Breanne Neely

Breanne Neely

Emergency Fund vs. Seasonal Fund: What’s the Difference (and Do You Need Both?)

Mastering personal finance basics often begins with a solid savings strategy, but not all savings accounts serve the same purpose. If you have ever...

Life doesn’t always follow a straight path—but with the right support, every turn gets easier. From surprise expenses to big plans, we’re here with fast, flexible funding to keep you moving.

.jpeg)

Mastering personal finance basics often begins with a solid savings strategy, but not all savings accounts serve the same purpose. If you have ever...

Losing your job can quickly transform manageable credit card debt into a growing financial burden. Without a steady income, interest continues to...

High-expense periods—like the winter holidays, summer vacations, or property tax season—can easily derail your finances if you aren't prepared....

1 min read

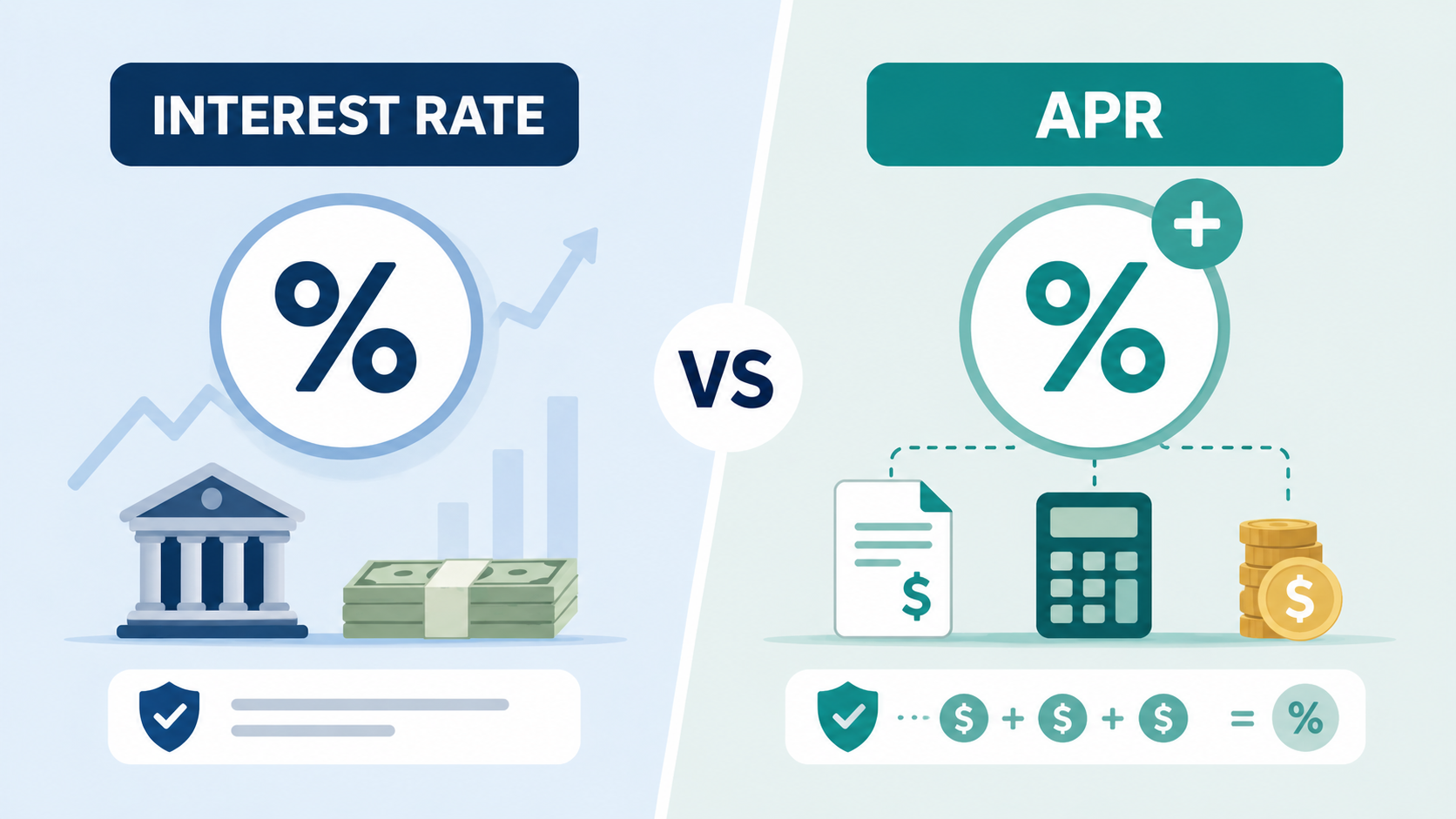

When shopping for a mortgage, auto loan, or credit card, you will inevitably encounter two crucial numbers. Understanding APR vs. Interest Rate:...

1 min read

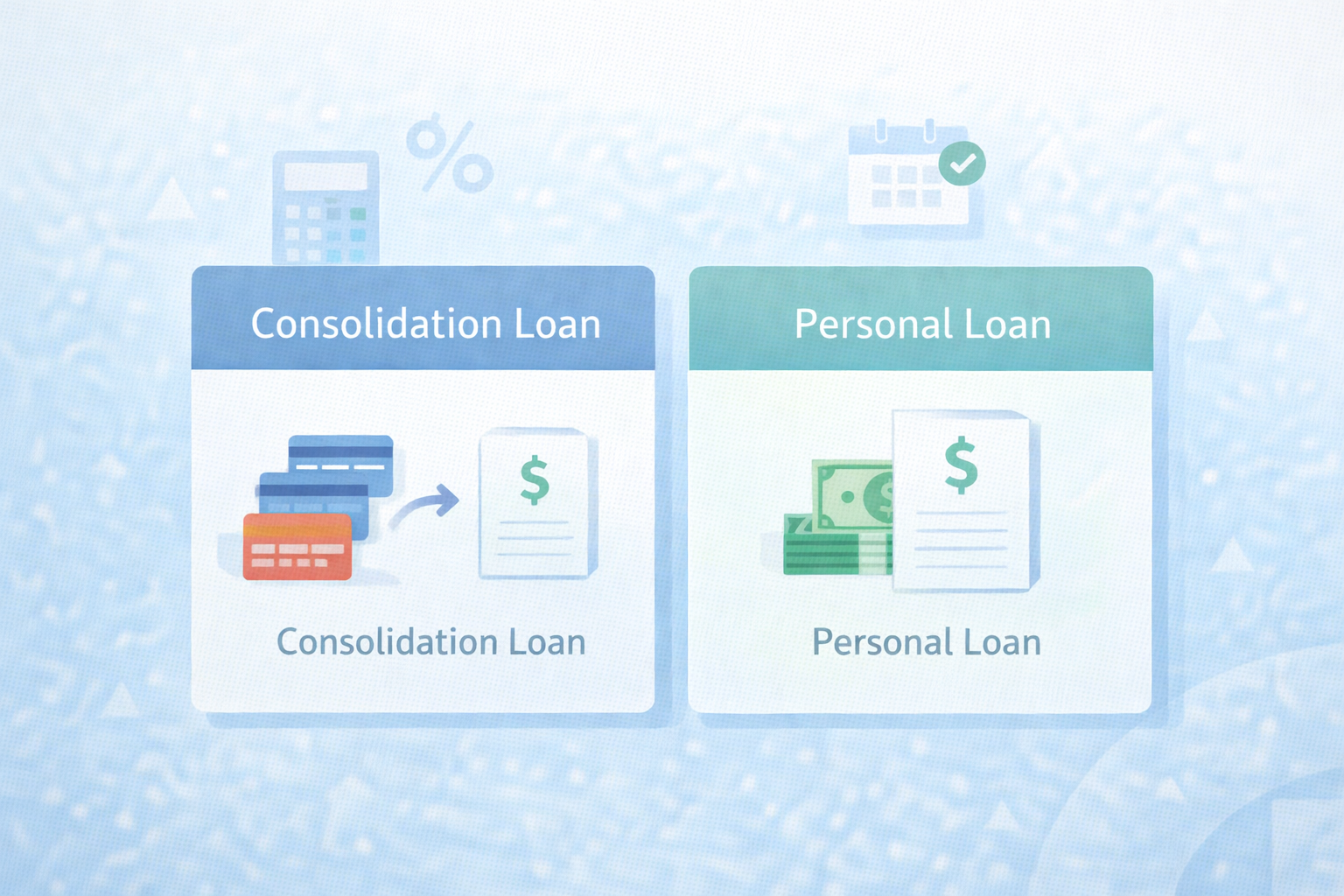

If paying bills feels like a game of Whac-A-Mole, you might ask: Consolidation Loan vs. Personal Loan: What’s the Difference? In reality, banks often...

1 min read

Getting approved for a debt consolidation loan is an exciting milestone on your journey to financial freedom. However, the real work begins...