Breanne Neely

Breanne Neely

Common Reasons to Use a Personal Loan (and When Not To)

Wondering exactly why get a personal loan? Whether you need to fund a major life event or manage a sudden financial hurdle, these financial tools...

Think of a loan like a playground seesaw: as your monthly payment goes down, the total interest cost almost always goes up. This mechanical balance defines your loan term—simply the length of time you have to pay the money back.

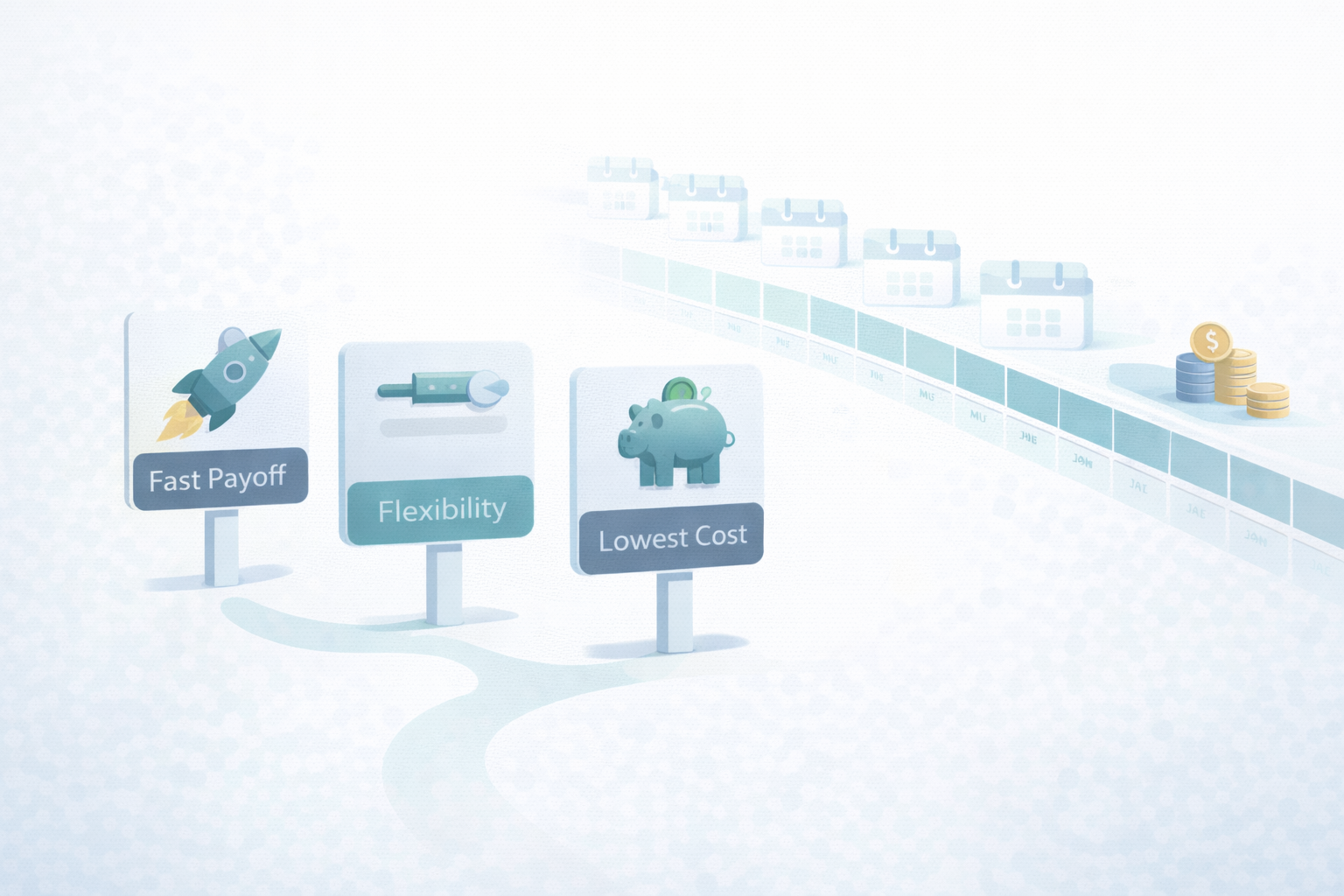

Selecting a timeline isn't just a math problem; in practice, it is a lifestyle decision. Whether you prioritize flexibility or speed, choosing the right loan term directly shapes your financial future.

Think of interest as a "convenience fee" for holding onto the bank's money. Stretching your payments out lowers your immediate monthly bill, but it increases the total price you pay for that flexibility. This is the central trade-off of any loan duration: you are constantly balancing today's cash flow against tomorrow's savings.

Consider a standard $10,000 personal loan. A 3-year plan is a financial sprint that might cost $322 monthly, getting you out of debt quickly with less interest paid. In contrast, a 5-year plan slows the pace to around $212 a month, but that extra time means the interest clock keeps ticking, significantly raising your total cost of borrowing.

Your choice depends on whether you need monthly breathing room or the lowest total price tag:

A simple decision framework helps pinpoint exactly which strategy fits your wallet.

Finding the right term requires looking beyond the calculation to see how much wiggle room you have in your budget right now. This loan term decision framework clarifies your priorities and helps you avoid over-committing to a bill you can't manage:

Your answers highlight whether you should focus on immediate safety or long-term speed. Even if you choose a longer term for safety today, you aren't necessarily stuck paying maximum interest forever. Fortunately, specific tactics allow you to manage these costs effectively.

When you compare loan offers, focus on the Annual Percentage Rate (APR) rather than the basic interest rate. The APR acts as the true "sticker price" because it captures fees and closing costs that the interest rate misses, ensuring you see the real total cost of borrowing money.

You can also control the timeline by making extra loan payments whenever your budget allows. Sending more than the minimum directly attacks your principal balance, which cuts your total interest costs and drastically shortens the term. This strategy offers the safety of a low required bill alongside the option to accelerate your financial freedom.

Ultimately, choosing the right loan term for your goals creates a balance between cash flow and savings that helps you sleep at night. Deepen your understanding of how loan term length affects your financial future to refine your debt payoff strategies. When you are ready to see real numbers, Check Your Rate.

Disclaimer: The information provided in this blog post is for educational and informational purposes only and should not be considered as financial, legal, investment, or tax advice. Symple Lending is not responsible for any financial outcomes resulting from following the information or ideas shared in this blog. Every individual's financial situation is unique, and we strongly encourage readers to take their own circumstances into consideration and consult with a qualified financial, legal, tax, and investment advisor before making any financial decisions. Symple Lending does not provide financial, legal, tax, or investment advice.

Life doesn’t always follow a straight path—but with the right support, every turn gets easier. From surprise expenses to big plans, we’re here with fast, flexible funding to keep you moving.

.jpeg)

Wondering exactly why get a personal loan? Whether you need to fund a major life event or manage a sudden financial hurdle, these financial tools...

Have you ever wondered exactly what is a personal loan? Whether you need to cover unexpected expenses or finance a major life event, grasping...

Managing multiple credit card payments involves more than keeping track of due dates. The hidden costs — financial, organizational, and emotional —...

1 min read

The term you signed on day one doesn't have to be the term you finish with. While extended contracts offer lower monthly payments, they often obscure...

1 min read

Summary: Loan term length is a key driver of your monthly cash flow, total interest paid, and long-term financial flexibility. Shorter terms mean...

1 min read

Ever been paralyzed by the sheer number of personal loan options available? You're not alone. Many borrowers feel overwhelmed when faced with terms...