Key Factors That Determine the Cost of a Personal Loan: Your Complete Guide

Did you know Americans collectively hold over $156 billion in personal loan debt? Behind that staggering figure are millions of individuals...

6 min read

Did you know that 26 million Americans are "credit invisible," meaning they have no credit history at all? In today's financial landscape, having no credit can be just as challenging as having bad credit. But here's the silver lining: building credit from scratch actually gives you a clean slate to create a strong financial foundation.

Whether you're a recent graduate, new to the country, or simply haven't engaged with credit before, the path to building credit doesn't have to be overwhelming. With the right tools and strategies, you can start building your credit profile strategically and confidently, opening doors to better financial opportunities along the way.

Your credit history shapes many areas of your life - from getting approved for loans to landing an apartment. For Gen Z and Millennials starting their financial journey, building a solid credit foundation can feel like a challenge. Many young adults begin with no credit record, which can make it harder to reach money goals like buying a car or home.

The good news? Gen Z and Millennials are making progress. Over half of Gen Z has achieved "Very Good" or higher credit scores through smart habits like paying bills on time and watching their credit reports. While the average scores (690 for Millennials, 680 for Gen Z) still trail older generations, these numbers continue to improve as more young people focus on building their credit profiles.

A secured credit card works like a regular credit card but requires a cash deposit that acts as your credit limit. This deposit - typically $200 to $500 - protects the card issuer while giving you a chance to build your credit.

These cards send your payment activity to the major credit bureaus each month, helping you create a solid payment history. They're perfect for beginners since you can't spend more than your deposit, making it easier to stay within budget.

To start, compare cards looking at annual fees and features. Pick one with reasonable fees, put down your deposit, and use the card for small purchases you can pay off monthly. Setting up automatic payments helps you avoid missed due dates.

Getting added as an authorized user on someone else's credit card can help you build credit without taking on full account responsibility. When you're added to a card, the account's payment history shows up on your credit report, though the primary cardholder remains in charge of making payments.

Getting added as an authorized user on someone else's credit card can help you build credit without taking on full account responsibility. When you're added to a card, the account's payment history shows up on your credit report, though the primary cardholder remains in charge of making payments.

This method works well if you're starting from zero credit. To make it work, team up with someone who has a long-standing account with a strong payment record and low credit usage. Keep in mind that both your credit scores can be affected - good or bad - by how the account is managed. Talk openly about expectations and set up clear rules about card use before getting started.

A credit-builder loan is a specific financial product made for people starting their credit journey. Unlike traditional loans, the money you borrow stays in a bank account while you make monthly payments. Once you complete all payments, you receive the full loan amount.

A credit-builder loan is a specific financial product made for people starting their credit journey. Unlike traditional loans, the money you borrow stays in a bank account while you make monthly payments. Once you complete all payments, you receive the full loan amount.

These loans work well for newcomers to credit since they don't require existing credit history. Banks, credit unions, and online lenders offer them, with amounts typically ranging from $300 to $1,000. The credit bureaus receive reports of your payments, which helps build your credit score over time.

When looking for a credit-builder loan, check local credit unions first - they often have the best rates. Read the terms carefully, focusing on payment amounts, loan length, and any fees. Most loans run 6 to 24 months, making them a manageable way to start building credit.

Your monthly rent and utility payments can now help build your credit score. Services like RentTrack, Rental Kharma, and LevelCredit report these regular payments to major credit bureaus, giving you credit for bills you're already paying.

These reporting services work by tracking your payment history and sending updates to credit bureaus each month. When you pay on time, it adds positive information to your credit report, showing lenders you handle financial obligations well.

To get started, research available services and check which credit bureaus they work with. Look for ones that report to all three major bureaus for the biggest impact. Set up automatic payments through your bank or the service to make sure you never miss a due date. Most services charge a small monthly fee, but the credit-building benefits can make it worth the investment.

A cosigner adds their name to your credit application, sharing the legal duty to repay. This partnership can help you qualify for loans or credit cards when your credit file is thin. Many young adults use parents or close family members as cosigners to start building credit.

Having a cosigner boosts your chances of approval and may help you get better interest rates. However, both you and your cosigner put their credit on the line - any missed payments affect both credit scores. Choose someone with good credit who trusts you, and make sure both parties understand their responsibilities.

To make this arrangement work, pick a reliable cosigner, read all paperwork together, and set up payment reminders. Consider automatic payments to stay on track. Keep open communication about payment schedules and any financial changes that might affect the agreement.

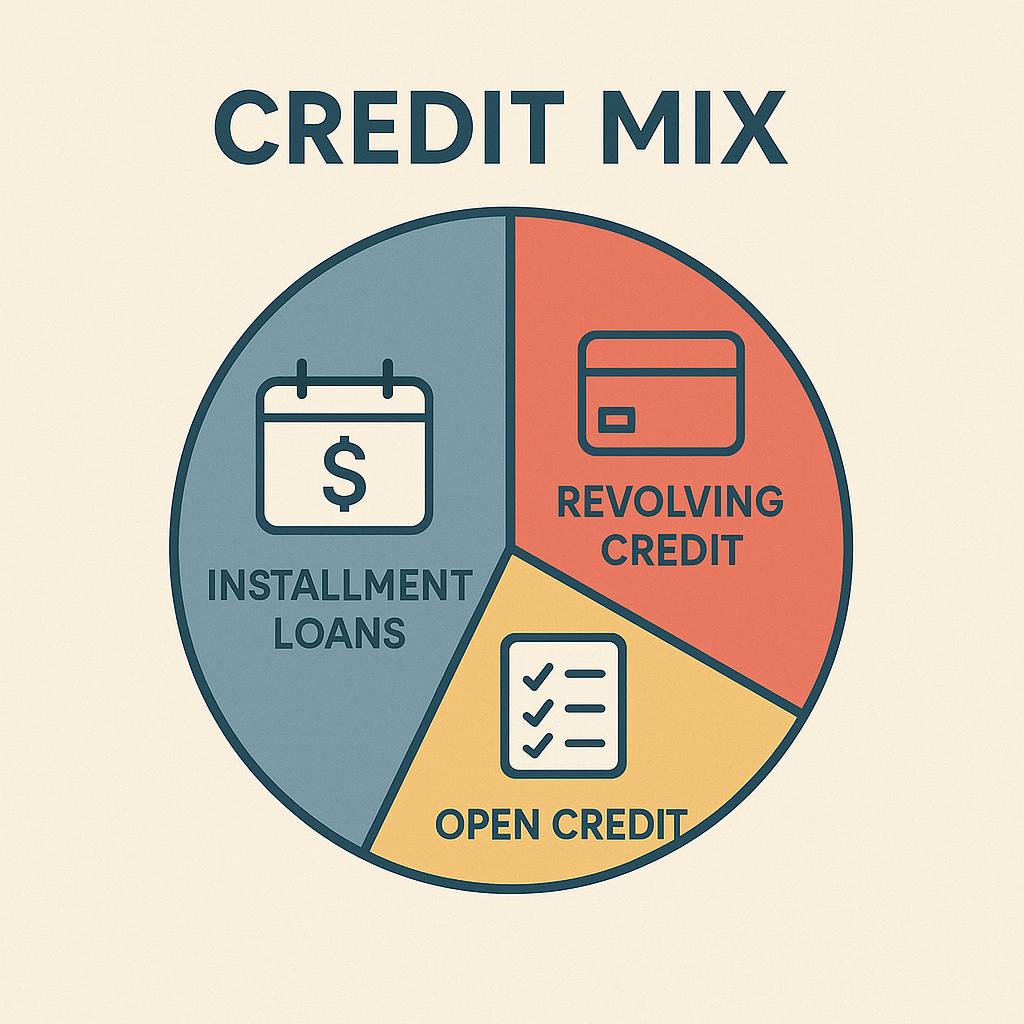

Credit scoring systems look at the different types of credit accounts you handle. A well-rounded credit file includes various account types: revolving accounts (like credit cards), installment loans (such as auto loans or student loans), and monthly payment accounts (like phone bills).

Credit scoring systems look at the different types of credit accounts you handle. A well-rounded credit file includes various account types: revolving accounts (like credit cards), installment loans (such as auto loans or student loans), and monthly payment accounts (like phone bills).

Having different credit types shows lenders you can manage various financial commitments. However, when you're new to credit, start small. Add new accounts slowly - perhaps beginning with a secured credit card, then adding a credit builder loan after 6-12 months of consistent payments.

Remember: quality matters more than quantity. Focus on maintaining perfect payment records with your existing accounts before opening new ones. Keep credit card balances low, and only take on new credit when it makes sense for your financial situation.

The foundation of a strong credit score starts with consistent habits. Pay all your bills by the due date - even one late payment can stay on your credit report for seven years. Keep your credit card balances well under 30% of your credit limits. For example, if you have a $1,000 limit, try to keep your balance below $300.

Take advantage of free credit monitoring tools from your bank or credit card company. These tools let you track your score changes and spot potential issues early. Many services send alerts when something changes on your report, helping you catch mistakes or fraud quickly.

Good credit habits open doors to better loan rates and credit card rewards programs. When lenders see a history of responsible credit use, they're more likely to approve your applications and offer favorable terms.

Every time you apply for new credit, lenders run a "hard inquiry" on your credit report. Each inquiry can lower your score by a few points and stays on your report for two years. Multiple applications in a short time can signal financial stress to lenders.

To protect your score, wait 3-6 months between credit applications. When shopping for specific loans like mortgages or car loans, submit all applications within a 14-30 day window - credit scoring models typically count these as one inquiry.

Before applying, check your credit score and research lender requirements. Pick cards or loans that match your credit profile to increase approval odds. Some lenders offer pre-qualification tools that use "soft inquiries," letting you check your chances without affecting your score.

Your credit account age makes up about 15% of your credit score. The longer you keep accounts open, the more they help your score. When you close old accounts, you lose that history and might see your score drop.

Your credit account age makes up about 15% of your credit score. The longer you keep accounts open, the more they help your score. When you close old accounts, you lose that history and might see your score drop.

Closing accounts also affects your credit utilization ratio - the amount of credit you use compared to what's available. Less available credit means higher utilization, which can lower your score. For example, if you have $2,000 in balances across two cards with $10,000 total limit, closing one $5,000 limit card doubles your utilization from 20% to 40%.

For cards you rarely use but want to keep active, make small purchases every few months. Set up a recurring bill like a streaming service, then enable automatic payments. If you must close accounts, start with newer ones and keep your oldest card active to maintain length of credit history.

Building credit from scratch is like constructing a house – it requires careful planning, the right tools, and patience. By combining multiple credit-building strategies, from secured cards to credit-builder loans, you can create a robust credit profile that opens doors to better financial opportunities. Remember, everyone starts somewhere, and your credit journey is a marathon, not a sprint.

The key is to start small, stay consistent, and use these tools responsibly. Focus on making all payments on time, keeping credit utilization low, and regularly monitoring your progress. With dedication and smart credit management, you'll be well on your way to building a strong credit foundation that will serve you for years to come.

Disclaimer: The information provided in this blog post is for educational and informational purposes only and should not be considered as financial, legal, investment, or tax advice. Symple Lending is not responsible for any financial outcomes resulting from following the information or ideas shared in this blog. Every individual's financial situation is unique, and we strongly encourage readers to take their own circumstances into consideration and consult with a qualified financial, legal, tax, and investment advisor before making any financial decisions. Symple Lending does not provide financial, legal, tax, or investment advice.

Did you know Americans collectively hold over $156 billion in personal loan debt? Behind that staggering figure are millions of individuals...

Did you know that Americans hold over $177 billion in personal loan debt? While that number might seem staggering, it reveals an important truth:...

Ever wondered why personal loans have become a financial lifeline for those navigating the unpredictable waters of midlife? Unlike the structured...

Did you know that a personal loan could both hurt and help your credit score—sometimes simultaneously? While most borrowers worry about the negative...

Did you know that your credit score has more influence on your daily life than your college GPA? While grades might help you land your first job,...

Did you know that your credit score can impact everything from your morning coffee runs to your dream home purchase? While most people think credit...