Breanne Neely

Breanne Neely

Emergency Fund vs. Seasonal Fund: What’s the Difference (and Do You Need Both?)

Mastering personal finance basics often begins with a solid savings strategy, but not all savings accounts serve the same purpose. If you have ever...

Did you know that your credit score can impact everything from your morning coffee runs to your dream home purchase? While most people think credit only matters for big loans, this three-digit number silently influences nearly every financial move you make - including whether you can rent that perfect apartment or even land your ideal job.

Understanding credit doesn't have to feel like decoding a secret language. Whether you're just starting your credit journey or looking to strengthen your financial foundation, mastering the basics of credit can open doors to better opportunities and save you thousands in interest over your lifetime.

Credit lets you borrow money or buy things now and pay later. Think of it as a financial tool showing lenders they can trust you to repay what you borrow. Building and maintaining credit for young adults opens doors to many opportunities - from renting your first apartment to getting utilities in your name. A good credit score can also help you qualify for a wider range of financial products, such as loans, credit cards, and other banking services.

When you use credit, you promise to repay the money, usually with interest added. Your credit profile tells the story of how well you keep these promises. Lenders make credit decisions based on your credit history and score. Starting early with good credit habits helps you get better interest rates and terms on future loans.

Building credit takes time, but it’s worth the effort. Whether you’re looking to finance a car, rent a home, or apply for a credit card, your credit standing can make these goals easier to achieve. Your credit score can also affect whether you need to pay a security deposit for utility services or housing.

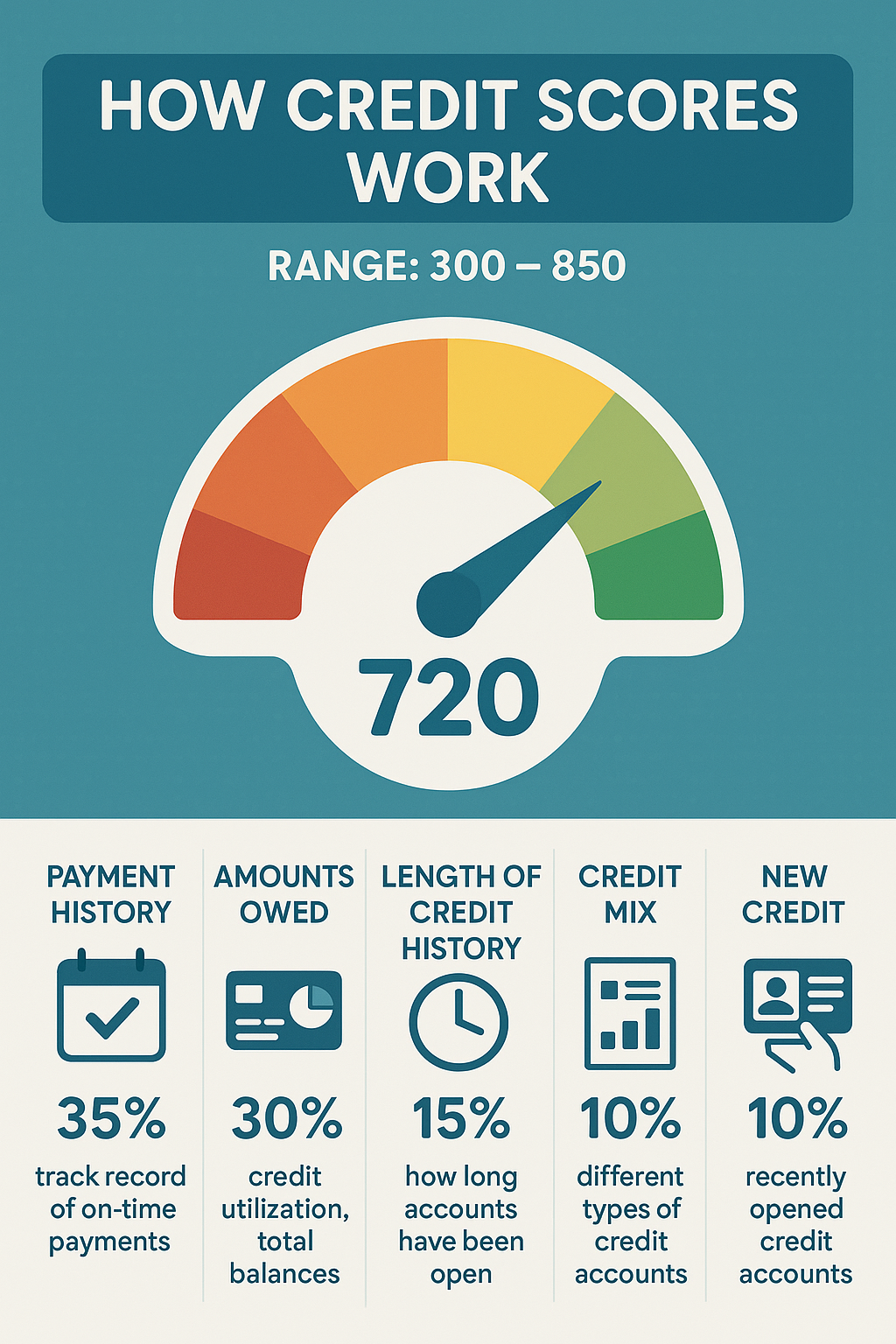

Credit scores tell lenders how likely you are to pay back money you borrow. The most common type of credit score is the FICO® score, which ranges from 300 to 850—higher numbers mean lower risk for lenders. Your score comes from information in your credit report, including how you handle bills and debt. The three main credit bureaus—Equifax, Experian, and TransUnion—each compile and provide credit data, such as account history and personal information, that is used to calculate your credit scores.

Credit scores tell lenders how likely you are to pay back money you borrow. The most common type of credit score is the FICO® score, which ranges from 300 to 850—higher numbers mean lower risk for lenders. Your score comes from information in your credit report, including how you handle bills and debt. The three main credit bureaus—Equifax, Experian, and TransUnion—each compile and provide credit data, such as account history and personal information, that is used to calculate your credit scores.

Think of your credit score like a financial report card. It includes many factors: your payment history (35%), how much you owe (30%), how long you’ve had credit (15%), new credit accounts (10%), and the mix of credit types you use (10%). Credit scores are calculated based on the information in your credit report, and different scoring models may weigh these factors differently.

These numbers matter because they affect what you pay for loans, whether you can rent an apartment, and sometimes even job opportunities. Many companies check credit scores to make decisions about working with you.

Your credit score reflects five main elements that show lenders how you handle money. Payment history carries the most weight - making payments on time helps, while late payments hurt your score. The amount you owe, also known as your credit utilization, is the percentage of your available credit you’re using. Try to keep this under 30% of your limit.

The length of your credit history shows how long you’ve managed credit accounts. Older accounts help build trust with lenders. New hard credit inquiries can temporarily lower your score, so only apply when needed. Finally, having different types of credit—known as your credit mix accounts—shows you can handle various financial responsibilities. Revolving credit, such as credit cards, and installment loans, such as auto loans, car loans, and personal loans, are all part of your credit mix accounts.

For young adults starting out, focus on making all payments on time and keeping card balances low. Examples of installment credit include auto loans, car loans, and personal loans. Having a mix of these accounts, along with revolving credit, can positively impact your credit score by demonstrating responsible management of different types of credit. These habits form the foundation of good credit health.

Starting your credit journey takes planning and patience. Here are some practical first steps: Get a student credit card if you’re in college, or try a secured credit card that requires a cash deposit. It is a useful tool for those looking to establish or rebuild credit. Another option is to become an authorized user on a parent’s credit card—this can help you establish credit before you open your own accounts, as their strong credit profile can help build your credit record. The primary cardholder's responsible use of the account can also help you on your credit-building journey.

Consider credit-builder loans from local banks or credit unions. These loans put your payments into a savings account while reporting to credit bureaus. As you build credit, make small purchases and pay your statement in full each month. If you have trouble qualifying for credit on your own, you might consider applying with a co-signer, who agrees to take responsibility for the debt if you cannot repay.

Common roadblocks include limited income and no credit history. Start with basic credit products designed for beginners. Keep your spending low and set up payment reminders to stay on track. Remember: responsible credit use means spending only what you can afford to pay back.

Want to build strong credit? Start by making on time payments on all your accounts—this is the most important way to improve your credit and is the biggest factor in your credit score. Set up automatic payments or phone reminders to never miss a due date.

Keep your credit card account balances low. Using less than 30% of your available credit helps keep your accounts in good standing and is key to building a positive credit history. For example, if your limit is $1,000, try to keep your balance under $300.

Don’t close old credit accounts—they add valuable history to your credit report. Keeping your credit card account open and in good standing helps your credit profile. Instead, mix different types of credit over time. Having both credit cards and loans (like a student loan) shows you can responsibly manage your accounts.

Be selective about new credit applications. Each application typically causes a small, temporary drop in your score. Monitor your accounts regularly through free credit tracking tools to spot and fix issues quickly.

Many people slip up with credit by missing payments, making late payments, keeping high balances, or closing old credit cards without thinking it through. Missed payments and even a single late payment can quickly lead to a low credit score. Opening several new accounts in a short time can also hurt your credit score. Negative marks like late payments and accounts in collections can remain on your credit report for up to seven years.

Many people slip up with credit by missing payments, making late payments, keeping high balances, or closing old credit cards without thinking it through. Missed payments and even a single late payment can quickly lead to a low credit score. Opening several new accounts in a short time can also hurt your credit score. Negative marks like late payments and accounts in collections can remain on your credit report for up to seven years.

To stay on track, set up payment alerts on your phone or use automatic bill pay - this helps you never miss a due date. Only apply for new credit when you really need it. Keep an eye on your credit card spending and try to pay off balances each month.

If you carry balances, make a plan to pay them down steadily. Start with the highest-interest debt first. Keep older accounts open, even if you don’t use them much - they add value to your credit profile strength. Check your credit reports every few months to catch and fix any problems early.

Remember: good credit habits take time to build, but mistakes can quickly lower your score. Focus on steady, responsible credit use rather than quick fixes.

Stay on top of your credit by regularly checking your reports from all three major credit bureaus: Equifax, Experian, and TransUnion. Each of these three major credit bureaus provides a separate credit report, so it's important to review all of them. You can get free copies once a year at AnnualCreditReport.com. Your credit report includes personal details such as your name, address, and phone number. Look for mistakes like wrong account information or payments marked late when you paid on time.

Many banks and credit card companies offer free credit score tracking. These tools send alerts when your score changes or when a new account appears in your name. This helps you spot identity theft quickly.

Make it a habit to review your credit card statements monthly. If you see charges you didn’t make, report them right away. Keep copies of payment confirmations and dispute letters - they’re helpful if you need to fix errors on your credit report.

Set calendar reminders to check your credit reports every four months. By rotating between the major credit bureaus, you’ll have a clear picture of your credit status year-round. Your credit report may also include certain financial information, such as your account balances and payment history.

Your age matters in credit building because the length of your credit history makes up 15% of your credit score. Younger adults naturally start with shorter credit histories, which means patience is key as you build your financial track record. Starting your credit-building journey early gives you more time to develop a good credit history, which is essential for accessing favorable loan terms and building a successful financial future.

Starting good habits early gives you time to learn from small mistakes without major consequences. As you manage your first credit card or student loan, you’ll get better at budgeting, tracking due dates, and understanding interest rates.

Think of credit building like learning to cook - you start with basic recipes before trying complex dishes. Begin with a secured card or becoming an authorized user, then gradually add different types of credit as you show responsible credit behaviors. This hands-on experience teaches valuable money management skills that benefit you throughout life.

Remember: time is on your side when you start young. Focus on consistent, positive credit behaviors rather than quick results.

Made a credit mistake? Take action right away. If you miss a payment, contact your lender immediately to make it current. Many lenders will work with you if you reach out before the situation gets worse. Set up a payment plan if you’re having trouble keeping up.

Remember that small setbacks don’t define your credit future. Focus on the basics: paying all bills on time going forward, keeping credit card balances low, and avoiding opening new accounts while you rebuild. Good payment patterns over 6-12 months can help offset past mistakes. Building a positive credit history can also improve your chances of qualifying for a loan or credit card in the future.

Consider working with a non-profit credit counselor for personalized guidance. They can help create a budget and debt management plan. Some credit unions offer special credit-builder products designed to help after financial difficulties. The key is staying committed to your recovery plan - each on-time payment moves you closer to better credit health.

Looking to learn more about credit? Start with trusted websites like MyFICO.com, CreditKarma.com, and the Consumer Financial Protection Bureau (CFPB). These sites offer free tools, calculators, and easy-to-follow guides about credit basics.

For in-depth learning, pick up books like "Get Good with Money" by Tiffany Aliche or "The Total Money Makeover" by Dave Ramsey. These books break down credit concepts into simple steps you can follow.

Take advantage of free online classes through Khan Academy's personal finance section or Money Smart from the FDIC. Many banks and credit unions also offer free financial education programs for their members.

Download apps like Credit Sesame or Mint to track your credit score and learn as you go. Join online communities like r/personalfinance on Reddit to learn from others' experiences and ask questions about building credit.

Your credit journey is a marathon, not a sprint. While it may seem overwhelming at first, remember that every financial expert started exactly where you are - learning the basics and building habits one step at a time. The key is to stay consistent with your credit management practices and keep learning as you go.

Think of your credit score as your financial reputation - it's something that grows stronger with time and careful attention. By understanding the fundamentals covered in this guide and implementing smart credit practices, you're already on your way to building a solid financial foundation that will serve you well for years to come.

Disclaimer: The information provided in this blog post is for educational and informational purposes only and should not be considered as financial, legal, investment, or tax advice. Symple Lending is not responsible for any financial outcomes resulting from following the information or ideas shared in this blog. Every individual's financial situation is unique, and we strongly encourage readers to take their own circumstances into consideration and consult with a qualified financial, legal, tax, and investment advisor before making any financial decisions. Symple Lending does not provide financial, legal, tax, or investment advice.

Life doesn’t always follow a straight path—but with the right support, every turn gets easier. From surprise expenses to big plans, we’re here with fast, flexible funding to keep you moving.

.jpeg)

Mastering personal finance basics often begins with a solid savings strategy, but not all savings accounts serve the same purpose. If you have ever...

Losing your job can quickly transform manageable credit card debt into a growing financial burden. Without a steady income, interest continues to...

High-expense periods—like the winter holidays, summer vacations, or property tax season—can easily derail your finances if you aren't prepared....

1 min read

If your credit score isn’t where you want it to be, you’re not alone. Many people find themselves in a position where they want to improve their...

.jpeg)

1 min read

Improving your credit score doesn’t happen overnight, and that’s where a lot of people get discouraged. The truth is, a good credit score is built...

1 min read

Did you know that 34% of Americans have discovered errors on their credit reports that could be dragging down their scores? In the world of personal...