Breanne Neely

Breanne Neely

7-Day Personal Loan Readiness Plan: A Step-by-Step Prep Guide to Improve Approval Odds

Applying for a personal loan shouldn't feel like a lottery. Lenders aren't guessing about your financial health, and neither should you. This 7-day...

Did you know Americans collectively hold over $156 billion in personal loan debt? Behind that staggering figure are millions of individuals navigating loan options, often without fully understanding what drives their borrowing costs.

What you don't know can cost you thousands when it comes to personal loans. Many people use personal loans for various purposes, but understanding the costs associated with borrowing money—such as interest rates and fees—is crucial. The difference between a well-researched loan decision and an impulsive one could mean paying double the interest over the life of your loan. Understanding the factors that influence personal loan costs isn’t just financial trivia—it’s essential knowledge that directly impacts your wallet.

A personal loan is money from a bank, credit union, or online lender that you pay back with interest over a set period. These loans typically range from $1,000 to $50,000 and are popular for:

The minimum loan amount is usually $1,000, a common eligibility threshold. When determining eligibility and interest rates, lenders consider your credit rating, a numeric representation of your creditworthiness.

Many people choose personal loans because they provide a lump sum quickly, usually don’t require collateral, and come with fixed interest rates. An unsecured personal loan does not require collateral and is based solely on the borrower's creditworthiness. It often has lower rates than credit cards, making it helpful for managing large expenses without resorting to high-interest credit card debt.

When comparing personal loan costs, understanding the difference between interest rate and APR is essential. The interest rate is simply the percentage you pay on the borrowed amount. However, the Annual Percentage Rate (APR) includes both the interest rate and additional fees like origination charges. Lenders charge various fees, such as origination fees, which are included in the APR calculation.

APR gives you a more complete picture of what you’ll actually pay. For example:

Despite having identical interest rates, the second loan costs significantly more. When shopping for personal loans, always compare APRs rather than just interest rates to understand the true borrowing expense. The lowest APR is typically available to borrowers with higher credit scores, larger loan amounts, and shorter loan terms.

There is a difference between a personal loan rate and personal loan interest rates: the personal loan rate refers to the specific rate offered to you. In contrast, personal loan interest rates describe the range of rates available in the market. Personal loan rates can vary based on your creditworthiness, income, loan amount, and term.

The time you take to repay your loan significantly affects your monthly payment and the total cost. The loan's term is a key factor in determining the interest rate and overall repayment terms. Repayment terms can also vary based on the lender, loan amount, and your credit profile. Shorter loan terms mean higher monthly payments but less interest paid overall, while longer terms reduce your monthly obligation but increase the total amount you’ll pay.

For example:

That’s an extra $1,133 in interest costs for the longer repayment period! This happens because interest continues to add up over time. While the lower monthly payment of a longer term might seem appealing for your budget and debt-to-income ratio, it’s important to consider how much more you’ll pay in the long run.

Your credit score has a significant impact on your personal loan costs. Lenders use this three-digit number to determine:

Lenders often consider your credit score range when determining your eligibility and the rates you are offered.

Higher scores translate to better rates because they suggest less risk to lenders. The difference can be substantial:

Your credit score considers your payment history, amounts owed, length of credit history, new credit applications, and types of credit used. Your credit report contains detailed information about your credit history, including bankruptcies and late payments, and reviewing it for errors can improve your chances of approval. To improve your score and qualify for better loan rates, focus on paying bills on time, reducing existing debts, and limiting new credit inquiries.

Other factors, such as your employment status and overall financial profile, influence your loan approval and interest rate.

When applying for a personal loan, lenders carefully examine your credit score and your income and debt-to-income ratio (DTI). Your DTI represents the percentage of your monthly gross income that goes toward paying debts, calculated as:

DTI = (Total Monthly Debt Payments ÷ Gross Monthly Income) × 100

Lenders typically prefer borrowers with a DTI below 36%. The lower your ratio, the more likely you’ll qualify for better rates and higher loan amounts. For example:

Lenders may also require recent tax returns as proof of income during the loan application process.

The first person would likely receive more favorable loan terms, even with identical credit scores. Steady income is important—lenders look for consistent earnings to ensure you can make loan payments reliably.

The size of your personal loan directly affects both its cost and approval chances. Larger loans typically come with:

For example, a smaller $5,000 loan might be approved at 10% APR, while a $30,000 loan could command 15% APR or require collateral to secure approval. Most personal loans range from $1,000 to $50,000, with amounts exceeding this upper limit often requiring exceptional credit or additional security.

When determining how much to borrow, consider what you need and how the loan amount will impact your total borrowing costs. Remember that applying for an unnecessarily large loan can result in higher fees and rates, affecting your debt-to-income ratio.

Since minimum loan amounts and terms can vary by provider, it is important to compare lenders to find the best rates and loan options for your needs.

When considering the total cost of a personal loan, don’t overlook the fees that can significantly increase what you pay. Common fees include:

These fees directly impact your bottom line. For example, on a $10,000 loan with a 5% origination fee, you’ll pay $500 in processing costs before receiving funds. If you pay off early but face a 2% prepayment penalty, that’s another $200.

While most fees are included in the loan amount calculation, some (like late fees) aren’t. Many lenders have unique fee structures, so reviewing each lender's fee schedule carefully is important. When comparing loan offers, always ask for a complete fee schedule to understand the true borrowing expense.

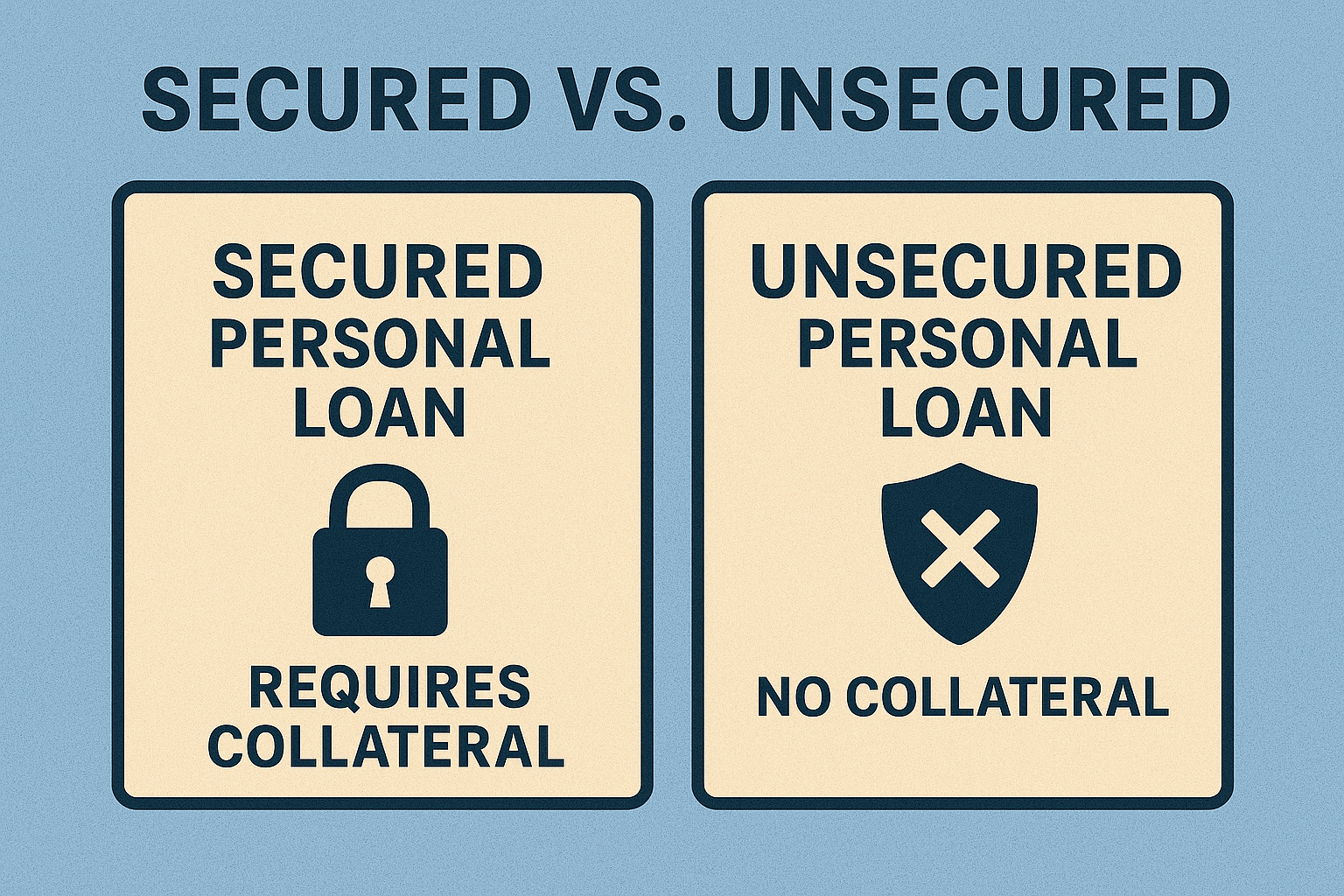

Personal loans come in two main types that affect your borrowing costs. Secured loans require collateral—an asset like your car, home, or even a savings account that the lender can take if you don’t repay. Unsecured loans don’t need collateral but rely on your creditworthiness.

The differences impact what you’ll pay:

For example, a $15,000 secured loan might have an 8% rate, while the same unsecured loan could charge 15%—potentially thousands more in interest over the loan term.

When choosing a personal loan, you'll typically select between fixed or variable interest rates, directly impacting your total loan cost.

Fixed rates stay the same throughout your entire loan term. Your monthly payments never change, making budgeting predictable and protecting you from market fluctuations.

Variable rates can change over time, usually tied to an economic benchmark. While they might start lower than fixed rates, they can increase, potentially raising your monthly payment significantly.

For example, if you borrow $10,000 with a variable rate that starts at 8% but rises to 10%, your $200 monthly payment could jump to $225, adding hundreds to your total loan cost. Meanwhile, fixed-rate borrowers would continue paying the same amount regardless of market changes.

Understanding your estimated monthly payment is key before committing to a personal loan. This figure tells you exactly how much you’ll need to pay each month, helping you budget and avoid surprises. Your estimated monthly payment is determined by several factors: the loan amount, the interest rate or annual percentage rate (APR), and the loan term.

To calculate your estimated monthly payment, you can use an online loan calculator or apply a standard formula that considers the loan amount, annual percentage rate (APR), and the number of months in your loan term. For example, if you borrow $10,000 at an APR of 12% for 36 months, your estimated monthly payment would be about $332. This calculation helps you see how different interest rates or loan terms can affect your monthly payment and the total interest you’ll pay over the life of the loan.

It’s also important to remember that your credit score can influence the interest rate you’re offered, impacting your estimated monthly payment. Maintaining a good credit score by making timely payments and keeping your credit utilization low can help you qualify for lower rates and more manageable payments. Before you get a personal loan, always check your estimated monthly payment to ensure it fits comfortably within your budget.

When shopping for personal loans, look beyond the advertised rates. Compare APRs rather than just interest rates, as APR includes fees and gives you a more accurate picture of total borrowing costs. Request loan estimates from multiple lenders to evaluate:

The loan application process typically requires proof of income and employment, and loan approval is based on your creditworthiness and financial profile.

Read the fine print carefully. Some loans have hidden penalties or restrictions that significantly impact the final expense. Use online loan calculators to see how different terms affect your payments and total costs.

Consider your budget realistically before committing. A loan with the lowest rate isn’t necessarily best if its payment schedule strains your finances.

Representative example: If you borrow $10,000 at a 10% APR for 5 years, your monthly payment would be $212.47. Over the life of the loan, you would pay $2,748.20 in total interest.

Now that you understand what affects personal loan costs, research options matching your financial situation. Look for lenders who provide clear, upfront information about rates, fees, and terms without hiding important details in the fine print. Some reputable lenders offer personal loans with transparent terms. Additionally, some lenders specialize in debt consolidation loans and may offer features such as same-day funding for qualified applicants.

Before applying, calculate how loan payments will fit into your monthly budget and affect your overall financial health. Remember that the lowest advertised rate isn’t always the best deal when you factor in all costs.

At Symple Lending, we believe in transparent lending practices that help you make informed decisions. We offer personal loan solutions with competitive rates, straightforward terms, and no hidden fees. Contact us today to discuss how we can help you find a personal loan that meets your needs without unnecessary expense.

Once you’ve received your personal loan, managing your debt and finances effectively is crucial for maintaining good credit and financial stability. Start by making all monthly payments on time—late payments can negatively affect your credit score and may result in costly late fees. Setting up automatic payments from your bank account is a simple way to ensure you never miss a due date.

It’s also wise to review your loan agreement carefully to understand the loan term, interest rate, and any origination fee or other charges. Use a loan calculator to estimate your monthly payment and incorporate it into your budget. By planning ahead, you can avoid financial strain and keep your payments on track.

Maintaining good credit habits, such as paying more than the minimum when possible and avoiding additional debt, will help you manage your loan successfully. Staying organized and proactive with your payments protects your credit score and puts you on the path to greater financial freedom.

Armed with knowledge about interest rates, terms, credit scores, and fees, you're now better equipped to navigate the personal loan landscape. Remember that small differences in rates or terms can translate to thousands of dollars over the life of your loan—money that could otherwise go toward your financial goals.

Don't rush this important financial decision. If possible, take time to improve your credit, compare multiple offers, and calculate the total cost of each option. The right personal loan should not only meet your immediate needs but also align with your long-term financial well-being. When used wisely, personal loans can be powerful tools for achieving your goals without unnecessary financial strain.

Disclaimer: The information provided in this blog post is for educational and informational purposes only and should not be considered as financial, legal, investment, or tax advice. Symple Lending is not responsible for any financial outcomes resulting from following the information or ideas shared in this blog. Every individual's financial situation is unique, and we strongly encourage readers to take their own circumstances into consideration and consult with a qualified financial, legal, tax, and investment advisor before making any financial decisions. Symple Lending does not provide financial, legal, tax, or investment advice.

Life doesn’t always follow a straight path—but with the right support, every turn gets easier. From surprise expenses to big plans, we’re here with fast, flexible funding to keep you moving.

Applying for a personal loan shouldn't feel like a lottery. Lenders aren't guessing about your financial health, and neither should you. This 7-day...

Most people don’t delay debt relief because they’ve decided against it. They delay because they want to “think about it.” They want to wait for a...

Ever noticed how your financial plans seem to lose momentum when seasons change? That crisp fall air or summer sunshine often brings not just weather...

Did you know that a personal loan could both hurt and help your credit score—sometimes simultaneously? While most borrowers worry about the negative...

Ever wondered why juggling multiple debts feels more like a circus act than a financial strategy? It's not just about the money; it's about the...

Did you know the average American carries over $100,000 in total existing debt when mortgages, auto loans, credit cards, student loan debt, and other...