Breanne Neely

Breanne Neely

Common Reasons to Use a Personal Loan (and When Not To)

Wondering exactly why get a personal loan? Whether you need to fund a major life event or manage a sudden financial hurdle, these financial tools...

Ever wondered why personal loans have become a financial lifeline for those navigating the unpredictable waters of midlife? Unlike the structured financial journey of your 20s and 30s, your 40s and beyond often bring unexpected financial crossroads—from helping children with college expenses to weathering sudden medical bills.

Personal loans offer a unique solution during these transitional years, providing quick access to funds with the predictability that becomes increasingly valuable as retirement approaches. Personal loans are a way of borrowing money to cover specific needs or unexpected expenses. With fixed payment schedules and clear terms, personal loans create financial breathing room exactly when life seems determined to throw its most expensive surprises your way.

Midlife often brings unexpected financial pressures. If you’re in your 40s or beyond, you might be juggling career changes, helping children with college expenses, or facing sudden costs like medical bills or home repairs. Emergency medical expenses are a common reason people turn to personal loans, as these urgent costs often require quick access to funds.

Personal loans can provide a practical solution during these transitions. They offer quick access to funds with fixed monthly payments, making it easier to manage your cash flow when facing high or unexpected expenses.

The predictability of personal loans is particularly valuable during significant life changes. With set interest rates and payment schedules, you can budget more effectively and avoid the stress of fluctuating payments, which is especially helpful if you’re approaching retirement or adjusting to a new income situation.

What is a personal loan? A personal loan is money you borrow from a financial institution—like a bank, credit union, or online lender—that you pay back in regular monthly installments over a set period, usually with a fixed interest rate. A personal loan is a financial product designed to help individuals meet various financial needs.

Think of a personal loan as a car loan, but more flexible. You can use personal loans for almost anything—consolidating debt, fixing your home, covering medical bills, or funding major life events. Many personal loans are used for various purposes, from consolidating debt to covering emergency expenses.

Unlike mortgages or auto loans, most personal loans are unsecured, meaning they don’t require collateral like your house or car. Loan funds are typically disbursed as a lump sum directly into your bank account, making it easy to access and use the money for your intended purpose. This makes them more accessible and versatile for different needs.

Many people think personal loans are complicated, but they’re actually straightforward financial tools with clear repayment terms and few restrictions on how you use the funds.

Personal loans aren’t one-size-fits-all—several types are designed to meet different financial needs and situations. Understanding these options can help you choose the best fit for your goals and budget.

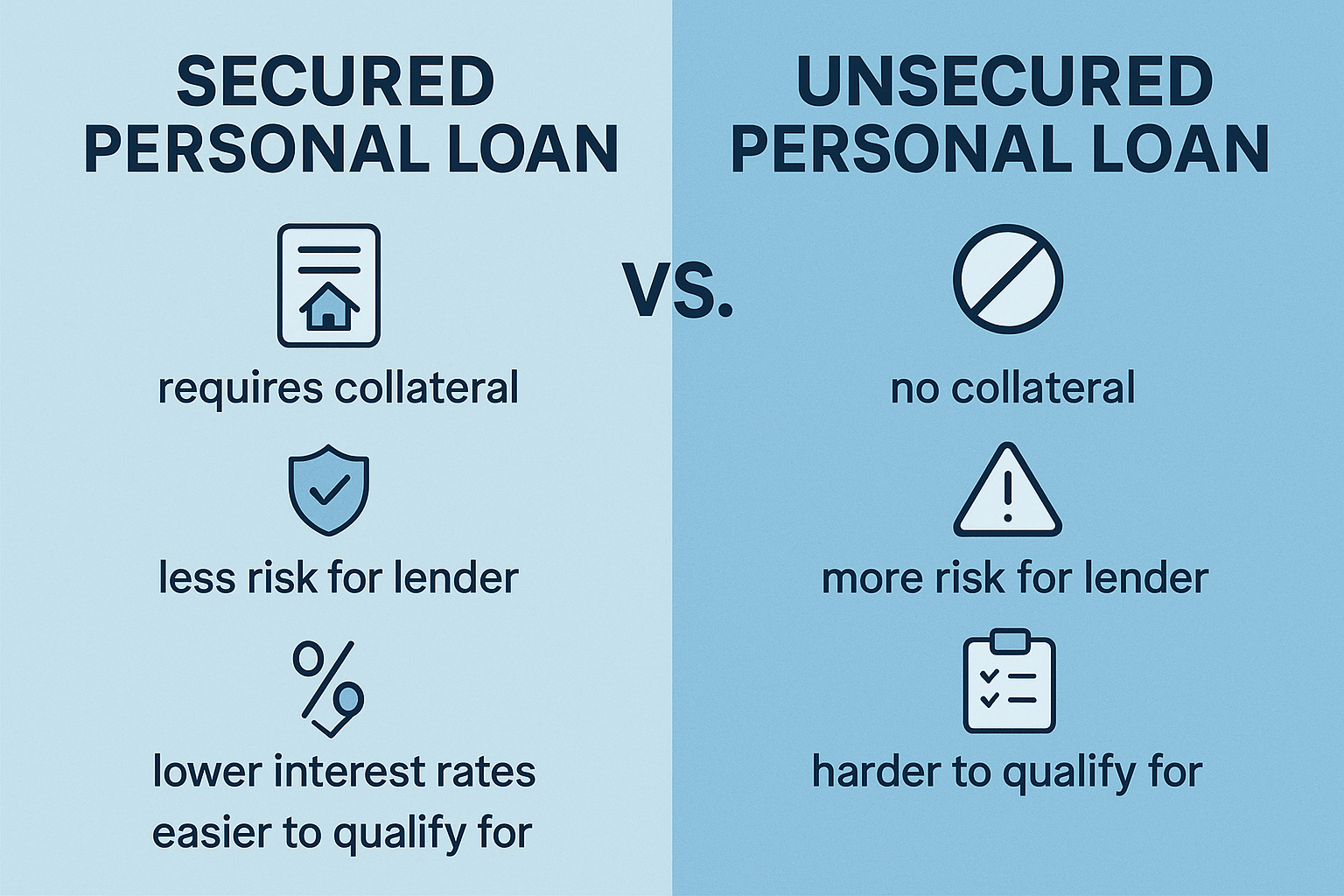

Unsecured personal loans are the most common type. These loans don’t require you to put up any collateral, such as a car or savings account, making them accessible and straightforward. Approval is typically based on your credit score, income, and debt-to-income ratio. Because there’s no asset backing the loan, interest rates may be higher than secured loans, but you won’t risk losing property if you can’t repay.

Secured personal loans require collateral—something of value like a savings account, certificate of deposit, or even a vehicle. Because the lender has an asset to claim if you default, secured loans often have lower interest rates. However, you should only consider this option if you’re confident in making every monthly payment.

Debt consolidation loans are designed to help you combine multiple debts—such as high-interest credit cards—into a single, manageable monthly payment. These loans can simplify your finances and may offer a lower interest rate, helping you save money and pay off debt faster.

Personal lines of credit work differently from traditional loans. Instead of a lump sum, you’re given a revolving credit limit you can draw from as needed. You only pay interest on the amount you use and can borrow and repay funds repeatedly during the draw period. This option offers flexibility for ongoing expenses or unpredictable costs.

By understanding the different types of personal loans, you can better match your borrowing strategy to your financial needs—whether consolidating debt, funding a home project, or covering emergency expenses.

When you’re approved for a personal loan, you receive a lump sum of money all at once. You then repay this amount plus interest through fixed monthly payments over the loan term, typically 1 to 5 years.

Most personal loans come with fixed interest rates, meaning your payment amount stays the same throughout the repayment period. Making regular loan payments on time is crucial for maintaining good credit and avoiding late fees. This makes budgeting simpler and more predictable. Some loans offer variable interest rates that may change over time, potentially affecting how much you pay each month.

You can get personal loans from three main sources: banks, credit unions, and online lenders. Traditional banks might take longer to process applications, while online personal loan lenders often provide faster approval and funding, sometimes within a day or two after you’re approved. Many lenders also offer the option to set up automatic payments, which can help ensure your loan payments are made on time and may even qualify you for a rate discount.

Your credit score is a key factor in qualifying for a personal loan and securing favorable loan terms. Most lenders look for a minimum credit score—often between 600 and 700—before approving a personal loan application. The higher your credit score, the more likely you will receive a lower interest rate and access to higher loan amounts.

Applying for a personal loan follows a fairly simple path:

To qualify for a personal loan, lenders will assess your credit score, monthly income, and existing debt obligations.

Personal loan lenders review your application by looking at:

You’ll typically need to provide:

Many lenders use a soft credit check during prequalification, allowing you to compare offers without impacting your credit score.

The good news? Many lenders offer quick decisions—you might get approved within minutes online, with funding deposited to your account within 1-2 business days after approval.

When comparing personal loans, it’s essential to look beyond the interest rate and focus on the Annual Percentage Rate (APR). The APR represents the true cost of borrowing, as it includes both the interest rate and any additional fees, such as origination fees or upfront charges.

Personal loan APRs can vary widely, typically from 6% to 36%, depending on your credit score, the loan amount, and the lender’s policies. A lower APR means a lower monthly payment and less money paid over the life of the loan.

Some personal loans offer fixed interest rates, which keep your monthly payment consistent throughout the loan term. Others may have variable rates that can change, potentially increasing your costs over time. Always check whether the APR is fixed or variable before signing a loan agreement.

To find the most affordable personal loan, compare APRs from multiple lenders, not just the advertised interest rates. This will give you a clear picture of the total cost and help you make a smart decision.

Personal loans can be practical solutions for several common midlife financial challenges:

Debt consolidation allows you to combine multiple high-interest credit card balances into one loan with a lower rate, potentially saving money and simplifying your monthly payments. Using a personal loan to consolidate debt, especially to consolidate high-interest debt, can help lower your overall interest costs and make repayment more manageable.

Home improvement projects become more manageable when funded through a personal loan, especially if you lack sufficient home equity or prefer a faster, unsecured borrowing option.

Major life events like your child’s education expenses, wedding costs, or unexpected medical bills—including emergency medical expenses—can be handled with personal loans.

For example, you might use a personal loan to consolidate $15,000 in credit card debt, reducing monthly payments and total interest paid. Taking out a new personal loan to pay off high-interest debt can also help improve your credit utilization ratio, which may boost your credit score. Parents might also bridge a financial gap with a personal loan while waiting for their child’s college financial aid.

When shopping for a personal loan, certain features can make a big difference in your experience:

Fixed monthly payments and interest rates are worth prioritizing. Personal loans typically offer fixed interest rates and monthly payments, making them predictable and easy to budget. They help you plan your budget without surprises and protect you from payment increases over time.

Pay close attention to fees that affect the total cost of borrowing. These might include origination fees (typically 1-8% of the loan amount), late payment charges, and prepayment penalties if you want to pay off your loan early. Personal loan rates can vary widely depending on your credit score, the lender, and your relationship with the lender.

Most personal loans are unsecured loans, meaning you don’t need to offer collateral like your home or car. This makes them accessible to more borrowers. However, some lenders offer secured personal loan options that might come with lower interest rates but require an asset as collateral for the personal loan.

Repayment terms for personal loans can range from two to seven years. Choosing a longer loan term can result in lower monthly payments, but may increase the total interest paid over the life of the loan.

Repaying a personal loan is straightforward, but knowing what to expect is important before you commit. Most personal loans come with fixed monthly payments, meaning you’ll pay the same amount each month for the loan term. This predictability makes it easier to budget and plan for the future.

Your loan agreement will outline all the key details, including the loan amount, interest rate, monthly payment, and repayment term (typically two to seven years). Most lenders offer automatic payment options, which can help you avoid late fees and ensure your payments are always on time.

Making consistent, on-time payments keeps your loan in good standing, helps build your credit history, and improves your credit report. Before you sign, review the repayment terms carefully and make sure the monthly payment fits comfortably within your budget. If you ever have trouble making payments, contact your lender right away to discuss your options.

While personal loans offer many benefits, they come with important cautions to keep in mind:

Interest rates can be significantly higher for borrowers with lower credit scores—sometimes 20% or more, making the total cost of borrowing substantial over time. In contrast, higher credit scores tend to improve your chances of qualifying for unsecured loans, often resulting in better approval odds and lower interest rates due to increased creditworthiness.

Be cautious about fees that increase your costs. These include origination fees (often 1-8% of the loan amount), late payment penalties, and sometimes prepayment charges if you pay off your loan early.

Always read the terms and conditions carefully. Missing payments can damage your credit score and create financial stress. Personal loans aren’t ideal for non-essential purchases or when you’re uncertain about your ability to make consistent payments.

Remember that taking on new debt always carries risk. Make sure the personal loan serves a necessary purpose and fits comfortably within your budget. Taking out a personal loan is a good idea in situations such as emergencies, debt consolidation, or large purchases, especially when you can afford the payments and secure a low interest rate.

When reviewing personal loan options, always look for clear loan terms including the repayment schedule, interest rate (APR), and all possible fees. Transparency is essential for making informed decisions. Be sure to compare personal loans from multiple lenders to find the best rates and terms for your needs.

Don’t just compare personal loan interest rates—calculate the total cost of each loan by adding up all interest payments and fees over the entire loan term. This gives you the true price of borrowing.

Consider these practical steps:

Choose a personal loan that fits both your immediate financial goals and your realistic ability to repay. The best offer isn’t always the one with the lowest rate or largest amount—it’s the one with terms you fully understand and can comfortably manage.

While personal loans offer flexibility and predictable payments, they’re not the only way to borrow money. Depending on your needs and financial situation, you might consider these alternatives:

Before choosing an alternative to a personal loan, compare interest rates, loan amounts, and terms from multiple lenders. Consider the risks, such as putting your home on the line or paying higher interest on credit cards. By weighing all your options, you can find the borrowing solution that best fits your financial goals and helps you save money in the long run.

Personal loans work well when:

However, they’re not the right choice when:

Before borrowing, ask yourself: “Do I have a clear plan to repay this loan?” Only proceed if you understand the full cost and loan terms. Consider alternatives like emergency savings or payment plans for medical bills. Remember that taking on debt should solve a problem, not create a new one.

Personal loans can be powerful financial tools during life's middle chapters—but like any financial decision, they require thoughtful consideration. The best borrowing decisions align with both your immediate needs and long-term financial health, creating solutions rather than additional stress.

Before signing any loan agreement, compare multiple offers, understand the total cost of borrowing, and assess how the payments will fit into your monthly budget. Remember that the ideal personal loan isn't just about getting cash quickly—it's about finding loan terms that provide financial flexibility while supporting your journey toward long-term financial stability.

Disclaimer: The information provided in this blog post is for educational and informational purposes only and should not be considered as financial, legal, investment, or tax advice. Symple Lending is not responsible for any financial outcomes resulting from following the information or ideas shared in this blog. Every individual's financial situation is unique, and we strongly encourage readers to take their own circumstances into consideration and consult with a qualified financial, legal, tax, and investment advisor before making any financial decisions. Symple Lending does not provide financial, legal, tax, or investment advice.

Life doesn’t always follow a straight path—but with the right support, every turn gets easier. From surprise expenses to big plans, we’re here with fast, flexible funding to keep you moving.

.jpeg)

Wondering exactly why get a personal loan? Whether you need to fund a major life event or manage a sudden financial hurdle, these financial tools...

Have you ever wondered exactly what is a personal loan? Whether you need to cover unexpected expenses or finance a major life event, grasping...

Managing multiple credit card payments involves more than keeping track of due dates. The hidden costs — financial, organizational, and emotional —...

1 min read

Borrowing money is often seen as something to approach with caution, and for good reason. Taking on a loan is a financial commitment, and it’s...

1 min read

Borrowing money can feel like a big step. Whether you are considering a personal loan for the first time or have experience with credit, it is...

1 min read

A personal loan can support your goals when it serves a clear purpose, fits comfortably within your budget, and aligns with your broader financial...