Breanne Neely

Breanne Neely

Build an Emergency Fund Without Derailing Your Life

Life rarely goes exactly to plan. From sudden home repairs to urgent healthcare needs, staying prepared is essential. Unfortunately, the average US...

Life doesn’t always follow a straight path—but with the right support, every turn gets easier. From surprise expenses to big plans, we’re here with fast, flexible funding to keep you moving.

Life rarely goes exactly to plan. From sudden home repairs to urgent healthcare needs, staying prepared is essential. Unfortunately, the average US...

The second half of the year is a practical window to review your financial progress, reset your goals, and build habits that can create real results...

Managing money doesn't have to be a stressful daily chore. If you want to achieve your financial goals faster, understanding how automating bills,...

1 min read

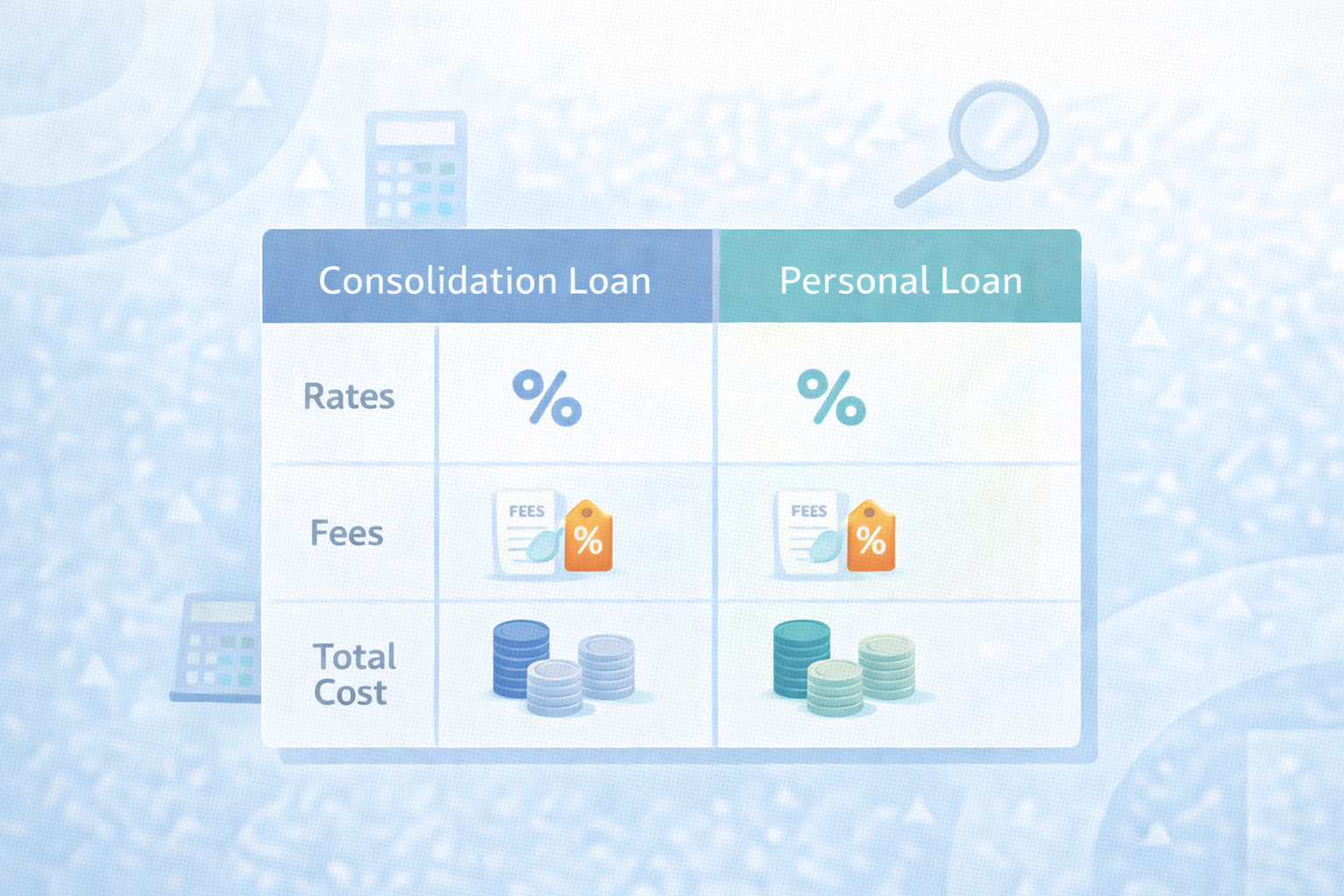

If paying bills feels like a game of Whac-A-Mole, you might ask: Consolidation Loan vs. Personal Loan: What’s the Difference? In reality, banks often...

1 min read

Staring at multiple bills makes it hard to tell if you’re saving money or just moving debt. In reality, consolidation loan vs personal loan rates...

1 min read

When an unexpected bill shows up—like a car repair or surprise medical cost—many people find themselves scrambling for a way to pay. In those...