Breanne Neely

Breanne Neely

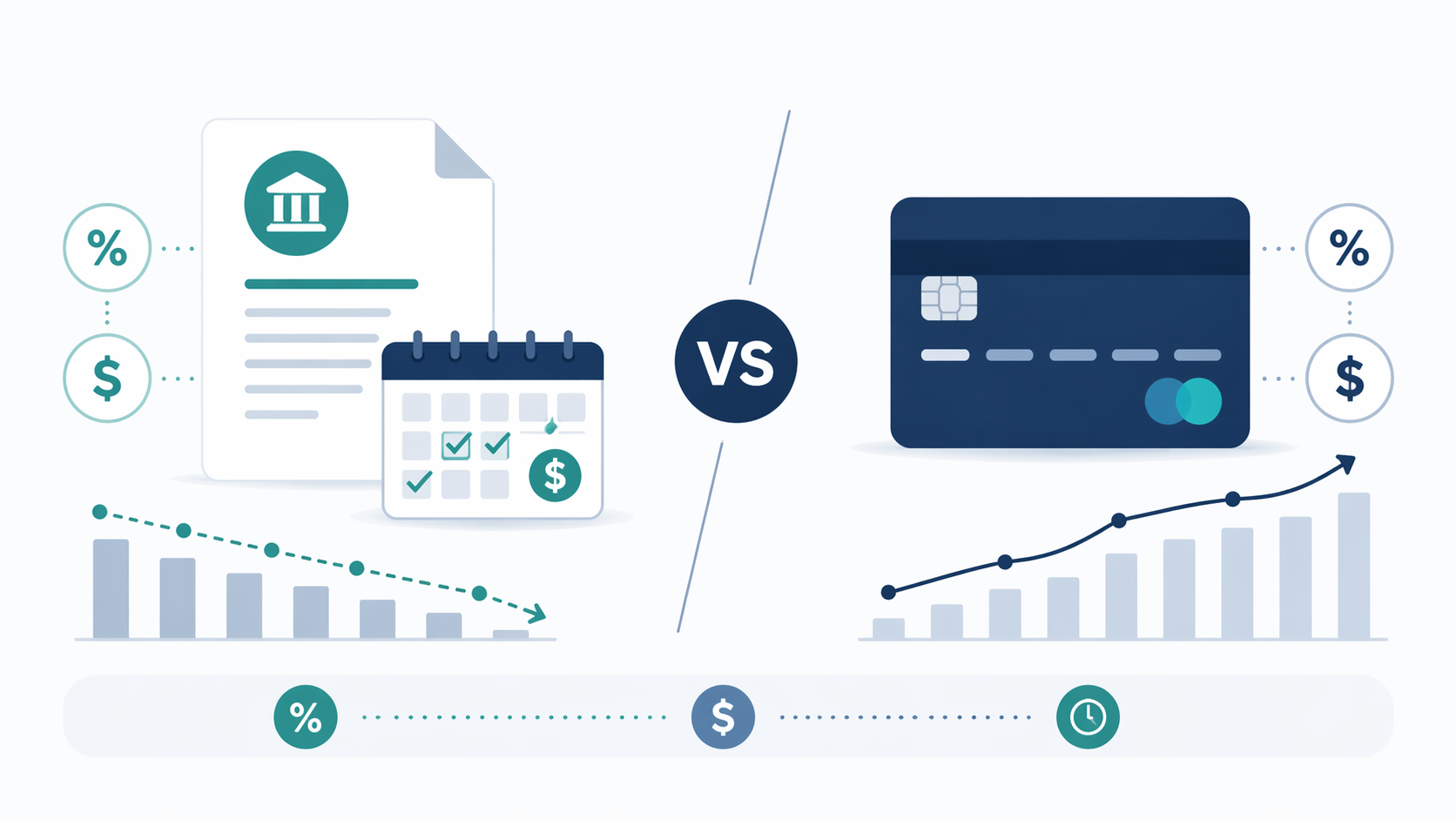

True Cost Comparison: APR, Fees, and Payoff Timelines for Loans vs. Cards

Have you ever paid your bill for a $3,000 car repair, frustrated that the balance barely moved? You've likely hit the "Minimum Payment Trap," paying...

Have you ever paid your bill for a $3,000 car repair, frustrated that the balance barely moved? You've likely hit the "Minimum Payment Trap," paying mostly interest—the "rent" charged to use someone's money. Comparing the true cost of personal loans versus credit cards based on APR, fees, and payoff timelines is vital. Using a total cost of borrowing calculator will finally show you exactly which option saves the most cash.

Buying a car with a low sticker price isn't a deal if the dealer adds huge checkout fees. Borrowing money works similarly. When weighing a personal loan versus a credit card, the interest rate is just the sticker price, while the Annual Percentage Rate (APR) is your true out-the-door cost. Calculating APR and interest by including upfront costs reveals why a slightly higher rate with zero fees is often cheaper overall.

Comparing loan fees versus credit card fees exposes invisible expenses. Always check your agreement for this hidden cost checklist:

Factoring these charges into your balance gives you the "Real APR" and prevents expensive surprises. Once you avoid these fee traps and secure the best upfront deal, your next step is escaping the minimum payment cycle with a fixed finish line.

Watching your credit card balance stall despite making payments exposes the danger of revolving credit versus installment debt. Cards keep you on a financial treadmill by charging interest on top of your interest. When comparing compound interest versus simple interest loans, the difference is striking: personal loans apply a fixed rate to a set balance, stopping your debt from constantly multiplying.

Running a $5,000 balance through a payoff timeline calculator reveals exactly how this compounding math works against you. If you only send the bank's requested minimum, you will spend years just covering the borrowing costs. Consumers often learn the hard way that minimum payments are a trap designed to barely touch the actual money borrowed.

Breaking free is exactly where fixed monthly payment benefits shine. A personal loan provides a steady payment plan with a guaranteed finish line, typically in three to five years. Rather than guessing your payoff date, you gain absolute certainty. With a clear exit strategy in sight, your next move is choosing your best path.

When asking whether a personal loan is cheaper than a credit card, evaluate the true cost using both APR and your timeline. Cards suit short-term needs, but escaping the credit card debt cycle requires structured, long-term loans. Before consolidating credit card debt, ask yourself:

Review your current rates today to start building a concrete debt-payoff strategy.

Disclaimer: The information provided in this blog post is for educational and informational purposes only and should not be considered as financial, legal, investment, or tax advice. Symple Lending is not responsible for any financial outcomes resulting from following the information or ideas shared in this blog. Every individual's financial situation is unique, and we strongly encourage readers to take their own circumstances into consideration and consult with a qualified financial, legal, tax, and investment advisor before making any financial decisions. Symple Lending does not provide financial, legal, tax, or investment advice.

Life doesn’t always follow a straight path—but with the right support, every turn gets easier. From surprise expenses to big plans, we’re here with fast, flexible funding to keep you moving.

Have you ever paid your bill for a $3,000 car repair, frustrated that the balance barely moved? You've likely hit the "Minimum Payment Trap," paying...

For many borrowers, the hesitation isn’t about the numbers.

Facing a $3,000 transmission repair? During a get money fast emergency, credit cards provide instant available credit. Conversely, comparing personal...