Breanne Neely

Breanne Neely

Build an Emergency Fund Without Derailing Your Life

Life rarely goes exactly to plan. From sudden home repairs to urgent healthcare needs, staying prepared is essential. Unfortunately, the average US...

Did you know that family caregivers provide nearly $873.5 billion worth of unpaid care annually in the United States? While the emotional commitment to caring for a loved one is immeasurable, the financial impact often surprises families.

Beyond the obvious expenses lie numerous hidden and unexpected costs that silently erode savings, career potential, and personal well-being. From out-of-pocket medical supplies to lost income opportunities, these unexpected costs and other financial burdens accumulate gradually, transforming what began as an act of love into a potentially destabilizing economic challenge.

Caregiving is a deeply rewarding yet often overwhelming journey that millions of family members undertake to support their loved ones. Nearly 2 in 5 Americans identify as family caregivers, stepping in to provide essential emotional, social, and financial support to care recipients. Most often, these caregivers are adult children caring for an elderly family member, though spouses and other relatives also play vital roles.

Taking on caregiving responsibilities can profoundly impact every aspect of a caregiver's life. While the well-being of the care recipient is always a top priority, the demands of caregiving can take a toll on the caregiver's own physical and mental health, disrupt social relationships, and threaten financial stability. Family caregivers often find themselves juggling multiple roles, striving to maintain balance while ensuring their loved one receives the best possible care.

Whether you're just beginning your caregiving journey or have been supporting a family member for years, understanding the full scope of caregiving responsibilities—and the support available—can help you protect your own well-being as you care for others.

The financial landscape for family caregivers is often more challenging than it first appears. According to a 2021 AARP report, family caregivers spend an average of $7,242 annually on out-of-pocket caregiving costs. These expenses can include everything from medical bills and prescription medications to transportation and home modifications, quickly adding up and straining the financial well-being of family members providing care.

For many, caregiving responsibilities require reducing work hours or leaving a job entirely to accommodate a loved one's needs. This can result in lost income, fewer retirement contributions, and lower Social Security benefits, directly impacting the caregiver's financial future. The cumulative effect of these financial challenges can be significant, making it harder to maintain financial stability and plan for long-term security.

Recognizing the true costs of caregiving is essential for family caregivers. By understanding how caregiving costs affect your financial landscape, you can take steps to protect your well-being and plan for a more secure future.

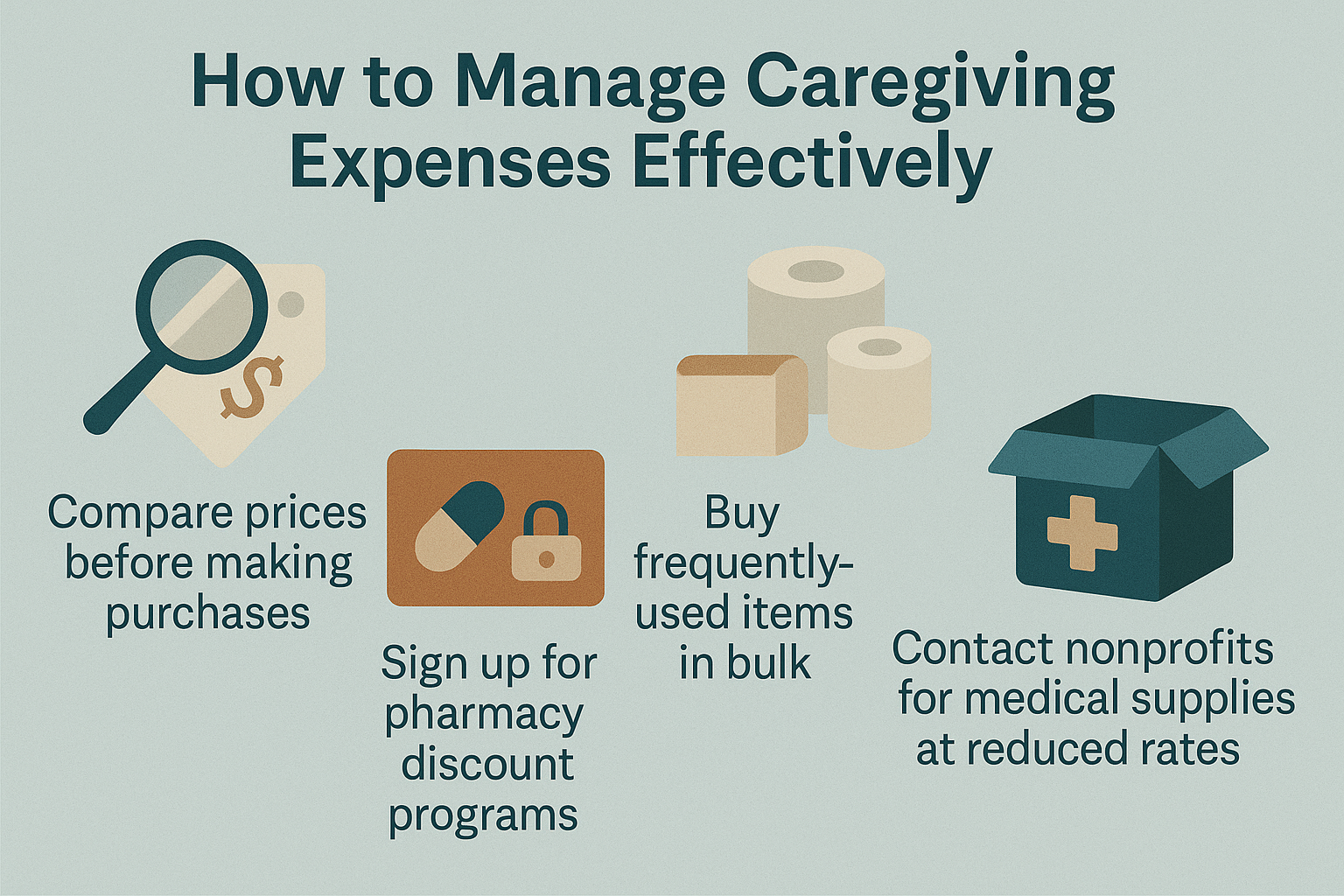

The ongoing costs of medical supplies can quickly add up for caregivers. From mobility aids and assistive devices to wound care products and adult diapers, these necessities often aren't fully covered by insurance.

Many caregivers are caught off guard by fluctuating prescription co-pays when medications change or insurance coverage shifts. Wound care supplies might suddenly become necessary, creating unexpected expenses that strain already tight budgets.

To manage these caregiving expenses more effectively:

Setting aside a small monthly amount specifically for these medical needs can help prevent financial stress when unexpected requirements arise.

Setting aside a small monthly amount specifically for these medical needs can help prevent financial stress when unexpected requirements arise.

Making a home safe for aging loved ones often requires physical changes to the living space. Common modifications include installing ramps, grab bars, stairlifts, widening doorways, and adding accessible bathrooms with shower seats and raised toilets. Improved lighting and non-slip flooring also help prevent falls.

Home modifications are often required to meet the evolving needs of care recipients, ensuring safety and accessibility as those needs change over time.

While these changes support independence and safety, they come with significant upfront costs. Many families report using savings or credit cards to finance these necessary renovations.

If you're facing home modification expenses, consider these funding options:

Planning ahead for these expenses can help you avoid financial strain while creating a safer environment.

Caregiving takes a heavy emotional toll, yet the cost of mental health support often falls outside insurance coverage. Individual counseling sessions and therapy appointments can add up quickly, becoming a financial burden many caregivers haven't planned for.

Emotional support is a crucial aspect of caregiving. It addresses the psychological and emotional needs of both caregivers and those they care for. Accessing this support can contribute to overall mental well-being, but it may also incur additional costs.

Support groups, mindfulness classes, and caregiver workshops can help manage stress and prevent burnout, but these resources rarely come free. While some employers or community centers offer limited access, most require out-of-pocket spending.

To protect your mental well-being without breaking the bank:

Taking care of your mental health isn't optional—it's an essential investment that prevents costlier health issues down the road.

The financial toll of caregiving extends far beyond direct expenses. Many caregivers must accommodate caregiving responsibilities by reducing work hours or leaving their jobs, which can impact career progression. These career changes lead to immediate income reductions and long-term financial consequences.

You're not just losing today's paycheck when you step back from your career to care for a loved one. You may miss out on promotions, forfeit healthcare benefits, and significantly reduce your retirement savings, with long-term caregivers facing up to 90% less in retirement funds compared to non-caregivers.

To protect your financial future while caregiving:

When focused on caring for someone else, your health often takes a backseat. This neglect can lead to serious conditions like anxiety, depression, hypertension, and even chronic illnesses that require ongoing medical care and costly treatment down the road.

Many caregivers skip doctor appointments and ignore symptoms, creating a perfect storm for health problems that could have been prevented. The physical demands of lifting, assisting with mobility, and losing sleep further increase the risk of injury and illness, impacting physical health with issues such as fatigue and sleep disturbances.

To protect both your health and wallet:

Investing in your health today prevents much larger medical expenses tomorrow.

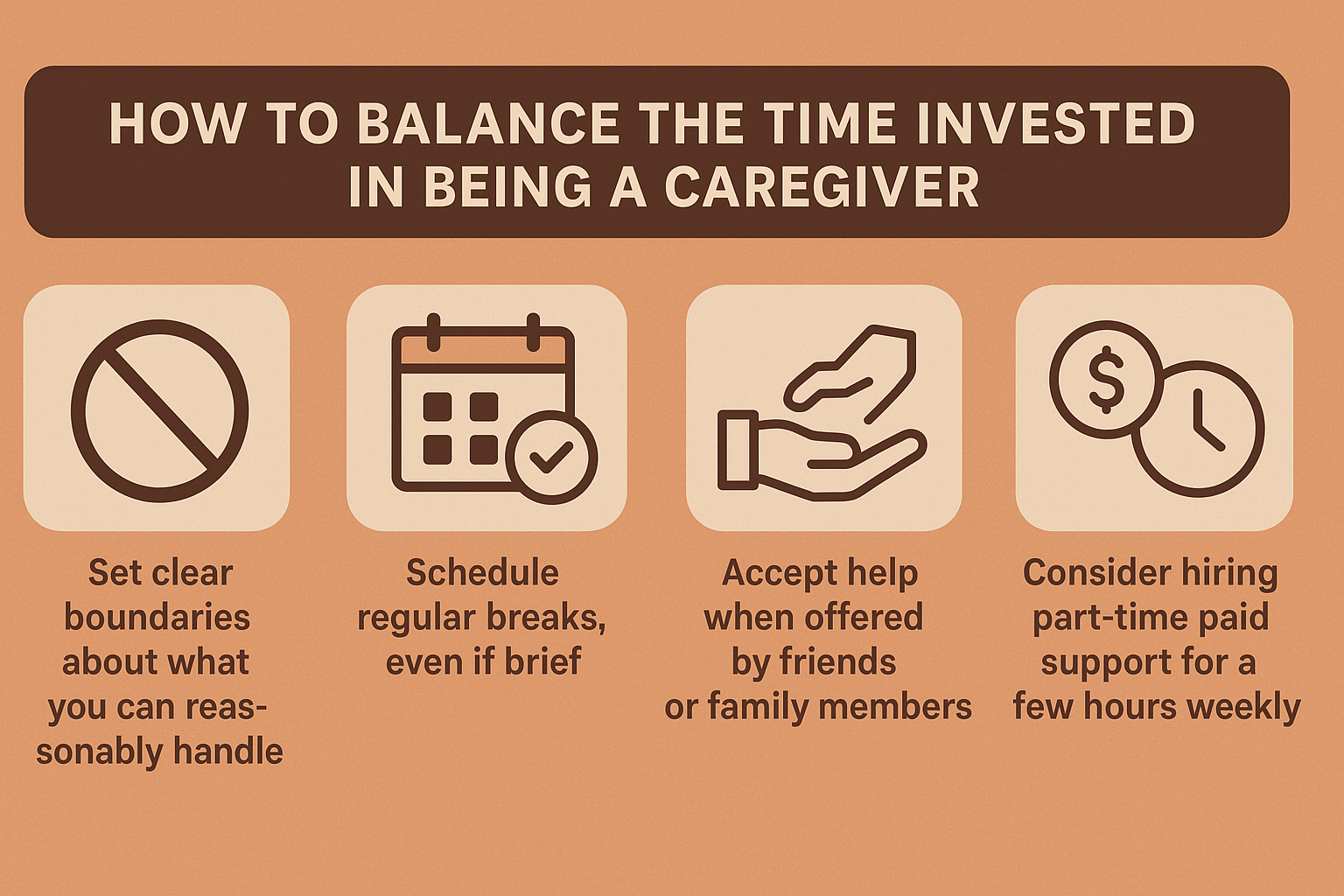

Family caregivers provide an estimated $873.5 billion worth of unpaid labor each year in the U.S. Informal caregivers—family members, friends, or neighbors who provide unpaid care—make a significant contribution to the overall value of caregiving. This staggering figure represents countless hours spent on feeding, bathing, transportation, and other essential tasks that would otherwise require paid professionals.

The time you spend caregiving often comes at the expense of your own leisure, work, and social activities. This represents about one-third of the total caregiving "expense" that's rarely calculated in financial terms.

To balance your time investment:

Remember that your time has real economic value, even when you're not being paid for it. Recognizing this helps justify investing in support that gives you back precious hours.

Remember that your time has real economic value, even when you're not being paid for it. Recognizing this helps justify investing in support that gives you back precious hours.

Getting your loved one to medical appointments, pharmacy visits, and errands creates ongoing expenses that many caregivers overlook. Gas, parking fees, vehicle wear and tear—these transportation costs add up quickly, especially for frequent medical visits.

Bringing in outside help like home aides, housekeeping services, or meal delivery can dramatically reduce your stress, but these services come with price tags that need careful budgeting. These costs should be factored into your overall caregiving budget.

To manage these expenses effectively:

When calculating the true cost of caregiving, don't forget to include these practical day-to-day expenses that keep your caregiving routine running smoothly.

Caregiving often leads to social isolation as relationships and personal activities take a backseat. Many caregivers find their friendships fading and family dynamics becoming strained as their attention focuses on their loved one's needs. For many, this means being responsible for both an elderly person and young children, which significantly increases both financial and emotional strain.

For the "sandwich generation"—those caring for both aging parents and children—childcare expenses can consume up to 22% of household income. These dual responsibilities create both financial pressure and emotional strain.

To balance social connections and childcare while managing expenses:

Finding ways to preserve your social connections isn't a luxury—it's essential for sustainable caregiving.

Managing a loved one's care involves paperwork and planning that often comes with unexpected price tags. Legal documents like power of attorney, guardianship applications, and medical directives can cost several hundred to thousands of dollars in attorney fees. These legal and emergency expenses are direct costs—explicit, out-of-pocket payments that can be substantial for caregivers.

These administrative expenses typically hit all at once, creating financial strain when you're already dealing with emotional stress. Meanwhile, emergencies like sudden hospitalizations, equipment failures, or urgent medication needs can appear without warning. Caregivers often have to use their own money to cover these sudden expenses, and rising costs due to inflation and increasing prices can make emergencies even more financially challenging.

To prepare for these hidden expenses:

Planning ahead for these expenses helps prevent debt when caregiving emergencies arise.

Many caregivers discover they need specialized training to provide proper care, especially for complex conditions like dementia or when medical procedures like wound care or safe transfers are required. The primary caregiver is often responsible for obtaining specialized training to ensure quality care. These skills don't come automatically; formal instruction often comes with a price tag.

Learning materials such as books, online courses, and hands-on workshops add to the financial burden of caregiving. While this education is essential for providing quality care, it's rarely covered by insurance or support programs.

To gain necessary skills without breaking your budget:

Investing in proper training now can prevent costly mistakes and reduce stress later.

Navigating the financial realities of caregiving requires thoughtful financial planning and a proactive approach. Family caregivers should start by creating a comprehensive budget that includes all caregiving-related expenses, such as transportation costs, medical supplies, and potential assisted living facility fees. This clear overview can help you anticipate out-of-pocket costs and avoid unpleasant financial surprises.

It's also important to explore all available financial assistance options. Government benefits, nonprofit resources, and financial support from other family members can help ease the burden. Don't hesitate to reach out for help—many organizations offer guidance and resources specifically for family caregivers.

Consulting a financial advisor can be a wise step, especially if you're facing complex decisions about retirement accounts, Social Security benefits, or long-term care planning. A financial advisor can help you develop a personalized plan that addresses your unique needs and supports your long-term financial security.

By taking these proactive steps—budgeting, seeking financial assistance, and working with a financial advisor—family caregivers can reduce financial stress, maintain financial stability, and continue providing quality care to their loved ones without sacrificing their own financial future.

Acknowledging the hidden costs of caregiving is the first step toward managing them effectively. Planning for the hidden costs of caring for older adults is essential to protect your own retirement. By anticipating expenses, researching available resources, and creating dedicated funds for different aspects of care, you can reduce financial surprises that compound caregiving stress.

Remember that investing in support systems—whether professional help, assistive devices, or your own mental health—isn't an indulgence but a necessity for sustainable caregiving. Financial advisers can help caregivers navigate the complex financial and emotional challenges of caregiving, ensuring you maintain financial stability for both your loved one and your own retirement. Taking proactive financial steps today protects both your loved one's well-being and your own financial future during this challenging but meaningful journey.

Disclaimer: The information provided in this blog post is for educational and informational purposes only and should not be considered as financial, legal, investment, or tax advice. Symple Lending is not responsible for any financial outcomes resulting from following the information or ideas shared in this blog. Every individual's financial situation is unique, and we strongly encourage readers to take their own circumstances into consideration and consult with a qualified financial, legal, tax, and investment advisor before making any financial decisions. Symple Lending does not provide financial, legal, tax, or investment advice.

Life doesn’t always follow a straight path—but with the right support, every turn gets easier. From surprise expenses to big plans, we’re here with fast, flexible funding to keep you moving.

Life rarely goes exactly to plan. From sudden home repairs to urgent healthcare needs, staying prepared is essential. Unfortunately, the average US...

The second half of the year is a practical window to review your financial progress, reset your goals, and build habits that can create real results...

Managing money doesn't have to be a stressful daily chore. If you want to achieve your financial goals faster, understanding how automating bills,...

1 min read

Imagine juggling your career and family responsibilities and suddenly becoming the primary caregiver for an aging parent—or another family member—all...

1 min read

A $2,500 HVAC repair makes anyone wonder the best way to pay for an emergency. Research shows unexpected expenses usually push us toward the fastest...

.jpeg)

1 min read

Your credit score can change because of decisions you make every single day, and some of the biggest hits come from situations you'd never think to...