10 Hidden Costs of Caregiving That Can Devastate Your Finances

Did you know that family caregivers provide nearly $873.5 billion worth of unpaid care annually in the United States? While the emotional commitment...

8 min read

Ever wonder why financial plans that looked perfect in January seem to fall apart by summer? You're not alone. Mid-year financial drift affects most adults, but it hits particularly hard when balancing multiple priorities in your 40s and beyond.

The truth is that financial plans aren't meant to be set in stone. They're living documents that should evolve with your life circumstances. Taking time for a mid-year financial reset isn't admitting defeat—it's one of the smartest money moves you can make to stay on track toward your long-term goals.

If you’re in your 40s or beyond, you’re likely juggling multiple financial responsibilities that younger adults don’t face. Supporting children (sometimes adult ones), helping aging parents, and trying to save for your own retirement can create a perfect storm of financial pressure.

Many of us feel overwhelmed by these competing priorities, especially when unexpected life events throw carefully laid plans off course. A job change, health issue, or family milestone can quickly shift what matters most in your financial picture.

Mid-year is an ideal time to take stock of where you stand financially. If January’s optimistic budgets have fallen by the wayside or unexpected expenses have emerged, you’re not alone. This halfway point gives you the chance to:

Budget planning at this stage is essential—it’s a flexible process that helps you manage changing priorities, set clear categories, and adjust your spending habits to stay on track with your savings and expenses.

Taking this pause to recalibrate doesn’t mean you’ve failed—it’s smart financial management. Financial stress is common during midlife, but proactive planning and thoughtful adjustments can help alleviate it. By acknowledging changes in your circumstances and making thoughtful adjustments to your financial strategy, you can regain momentum and reduce the anxiety that often accompanies money concerns in midlife.

Remember that financial planning during these years isn’t just about numbers—it’s about creating security and options for yourself and those who depend on you. Making thoughtful adjustments now can help you regain control of your financial life and move forward with greater confidence.

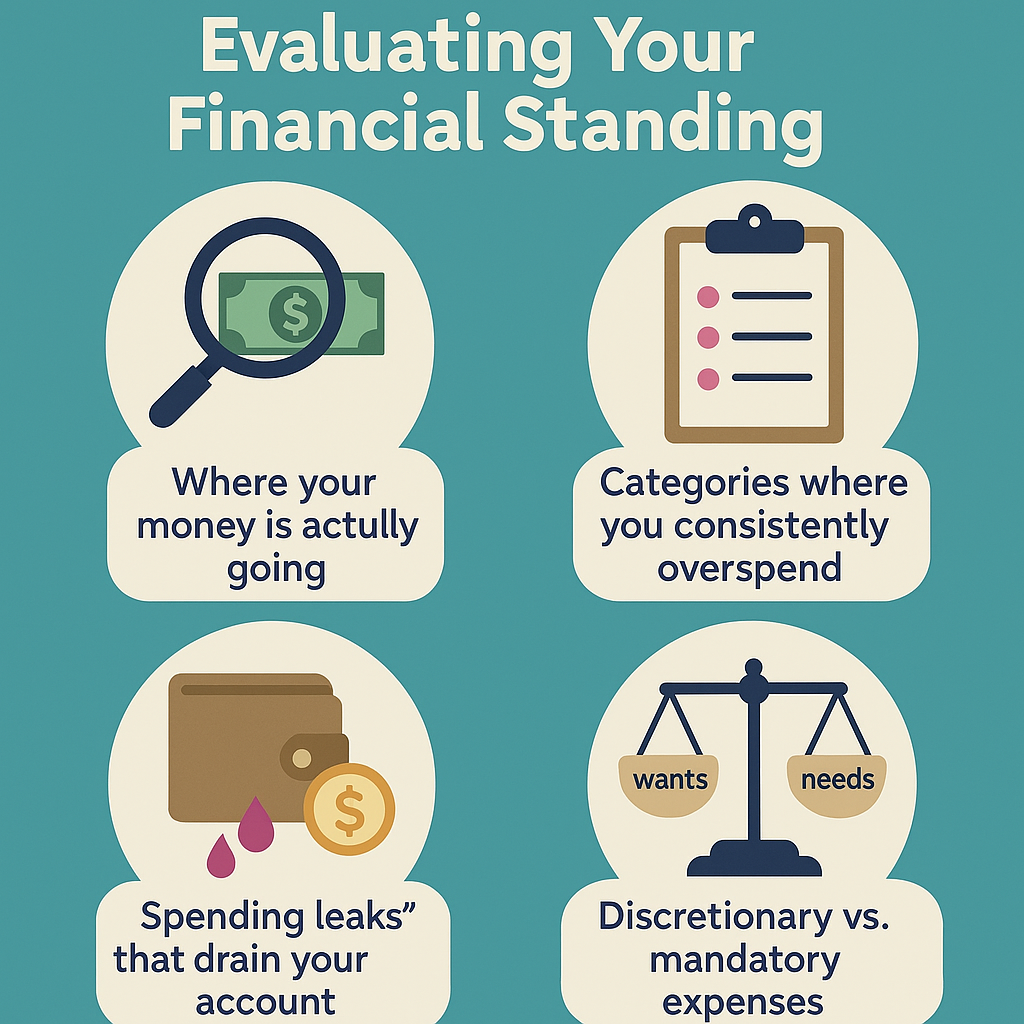

The first step toward financial clarity is knowing exactly where you stand. Start by calculating your net worth—add up all assets (cash, investments, home equity) and subtract all liabilities (mortgage, loans, credit cards). This single number gives you a snapshot of your overall financial health.

Next, take a close look at your cash flow. Review the last three months of income and expenses, and analyze your bank statements to identify spending habits and spot unnecessary expenses. Look for:

Your savings progress deserves special attention during mid-year reviews. Check your:

Don’t forget to examine your debt situation. High-interest debt can silently erode your financial progress, so list all outstanding balances along with their interest rates. While you’re at it, check your credit score—it affects everything from loan rates to insurance premiums.

As you review your finances, consider creating a realistic monthly budget to manage expenses, savings, and future goals. This self-assessment might feel uncomfortable, but it provides the honest foundation you need for effective planning. By understanding exactly where you stand mid-year, you can make targeted adjustments rather than general guesses about what needs to change. Remember to track financially so you can monitor your progress and make informed adjustments as needed.

A mid-year financial review is the perfect time to check your credit reports and ensure your credit health is on track. Your credit report is a detailed record of your credit history, including your accounts, payment history, and any recent credit inquiries. Reviewing your credit reports from all three major bureaus—Equifax, Experian, and TransUnion—can help you spot errors, catch signs of identity theft early, and understand the factors influencing your credit score.

A strong credit profile is essential for reaching your financial goals, as it can lead to better interest rates on personal loans, mortgages, and credit cards. Lower interest rates mean you’ll pay less over the life of your debt, freeing up more money for savings and investments. If you notice any inaccuracies or outdated information, dispute them promptly—this can help you correct them before they impact your loan approval or financial plans.

You’re entitled to a free credit report from each bureau once a year at AnnualCreditReport.com. Make it a habit to review your credit reports during your mid-year financial check-in. By staying proactive, you’ll be better equipped to manage your credit, reduce debt, and confidently move forward in the year's second half.

Once you’ve completed your financial assessment, it’s time to identify specific roadblocks that might be holding you back. Start by examining your debt - particularly those with interest rates above 10%. Credit cards and personal loans often fall into this category and can quietly drain thousands from your yearly budget. Actively paying off debt is a key step in financial management, helping you regain control and reduce financial stress. After identifying high-interest debt, consider debt consolidation as a strategy to simplify payments and potentially reduce your interest rates.

Next, look for those sneaky “spending leaks” in your budget. These aren’t the big purchases you remember but the small, repeated expenses that add up dramatically over time. Subscription services, frequent takeout meals, or impulse online shopping are common culprits. Similarly, watch for signs that your spending has gradually increased with your income without corresponding increases in savings.

When planning your debt repayment, making additional payments beyond the minimum can help you reduce your debt faster and save on interest in the long run.

Check your safety nets against recommended benchmarks:

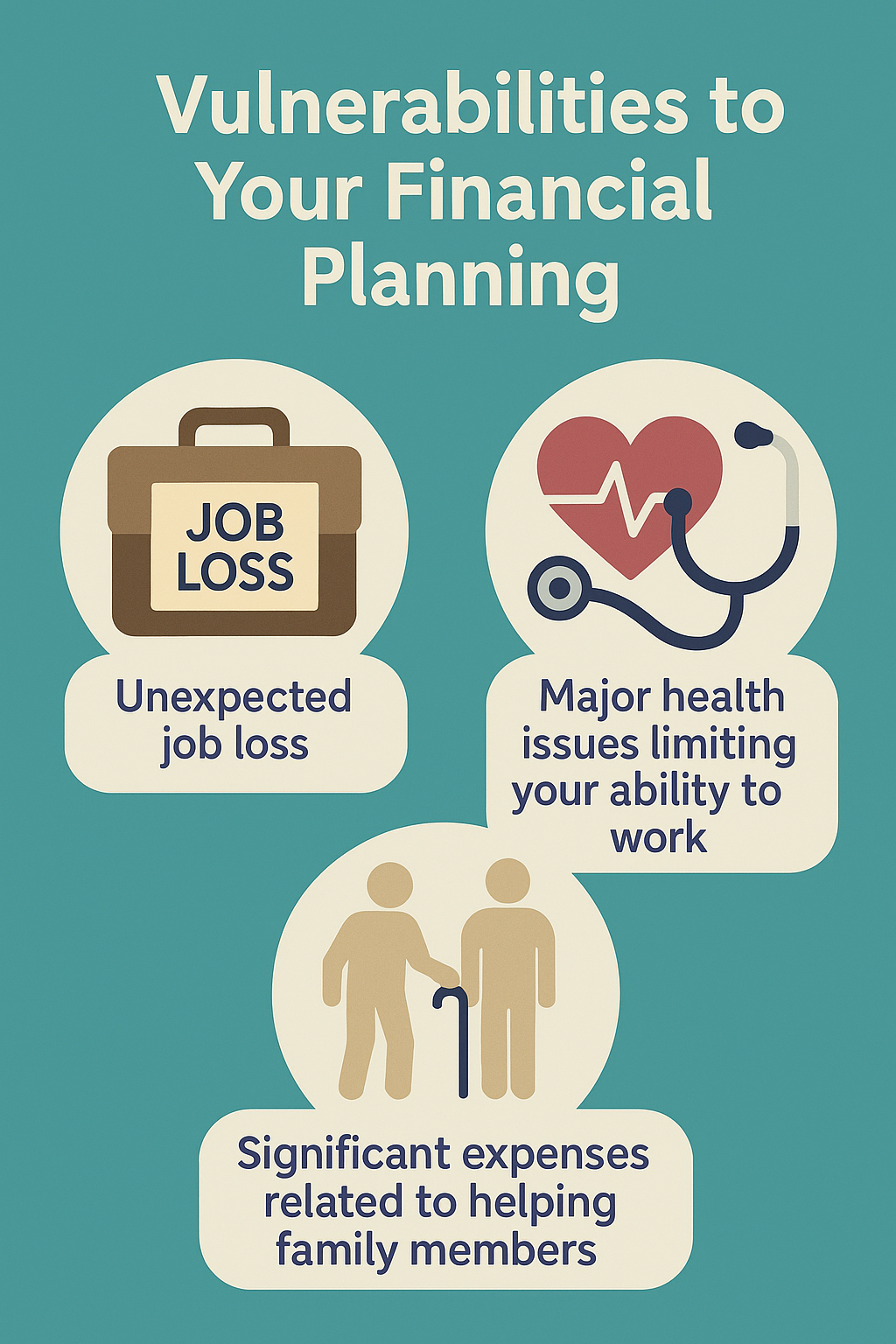

Don’t overlook potential vulnerabilities in your financial plan. Consider what would happen if you faced:

Don’t overlook potential vulnerabilities in your financial plan. Consider what would happen if you faced:

Identifying these obstacles isn’t about creating anxiety—it’s about spotting problems early while they’re manageable and developing targeted solutions, including building positive financial habits to support long-term success.

A robust emergency fund is the cornerstone of financial security, especially when life throws a curveball. If you haven’t already, use your mid-year review to assess your current savings and set a clear goal: aim to have enough in your emergency fund to cover at least 3 to 6 months of living expenses. This money should be kept in an interest-bearing savings account, where it’s easily accessible but still earning some interest.

Start by setting up automatic transfers from your checking account to your savings account—consistency is key, even if you can only save a small amount each month. Over time, these regular contributions will help your emergency fund grow without requiring constant attention. If you’re unsure how much you need or how to prioritize your savings, consider working with a financial advisor who can help you align your emergency fund with your broader financial goals.

Remember, an emergency fund isn’t just about peace of mind—it’s a practical tool that prevents you from relying on high-interest debt when unexpected expenses arise. By prioritizing your emergency fund in your budgeting and financial planning, you’ll be better prepared to handle whatever comes your way.

After identifying your financial challenges, it’s time to take action. Start by strengthening your emergency fund to cover 3-12 months of living expenses, depending on your job stability and family situation. Even small, consistent contributions can rebuild this safety net over time. If you receive a bonus or windfall, consider using that extra cash to boost your emergency fund or pay down debt.

Next, tackle high-interest debt using either the avalanche method (paying off the highest interest rates first) or the snowball method (eliminating the smallest balances first for psychological wins). Both strategies work—choose the one that matches your personality.

If you’re 50 or older, take advantage of catch-up contribution limits for retirement accounts. In 2025, you can contribute up to $23,000 to 401(k) plans and $8,000 to IRAs, including the extra catch-up amounts. Review your overall retirement plan and consider options like IRAs and CDs to help secure your long-term financial future.

For children’s education, consider tax-advantaged 529 plans, which allow your contributions to grow tax-free when used for qualified education expenses. Consider making charitable donations when reviewing your tax-advantaged accounts, as these can be valuable tax-deductible expenses.

Review your investment mix based on your time horizon. At midlife, you’ll likely need a balance between growth (equities) and stability (fixed-income investments). Avoid cutting equity exposure too dramatically—you still need growth potential. Plan for goals that may be a few years away by aligning your investment choices with your expected timeline.

Reassess your insurance coverage, particularly health, disability, and life insurance. These protections become increasingly important as you age. Track your tax-deductible expenses, such as medical bills and charitable donations, throughout the year to simplify your tax return and maximize your deductions.

Start budgeting for upcoming major expenses like holiday travel, back-to-school costs, or insurance renewals. Early planning can help you save money and reduce financial stress during busy seasons. Review your monthly expenses and consider cutting costs—canceling a streaming service you no longer use is a simple way to save money.

Finally, a realistic plan for supporting family members financially is created. While helping children and aging parents is important, remember that they can borrow for college or care, but you can’t borrow for retirement. Finding this balance is perhaps the most challenging aspect of smart financial planning for your future. Personal finance strategies, such as building an emergency fund and planning for the future, are essential for long-term stability.

If you receive a tax refund, consider putting it toward your savings goals to strengthen your financial position.

For online security, enable two-step verification on your financial accounts for added protection. Securing all financial accounts by using strong passwords and two-step verification is crucial to prevent unauthorized access and fraud.

Credit card debt can quickly derail your financial progress, especially if you’re not careful with spending or repayment. To avoid falling into the debt trap, start by adopting a solid budgeting strategy—such as the 50/30/20 rule—to ensure you’re living within your means and prioritizing your financial goals.

When using credit cards, always aim to pay your balance in full each month to avoid costly interest charges. Consider consolidating your debt with a personal loan at a lower interest rate if you carry a balance. This can simplify your monthly payment and help you pay off debt faster, especially if you qualify for a fixed rate and favorable loan terms.

Another effective approach is the debt snowball method: pay off your smallest credit card balances first, then roll those payments into your next largest debt. This strategy can help you stay on track and build momentum as you see your debts disappear individually.

By making mindful spending decisions, paying attention to your interest rates, and choosing the right repayment strategy, you can reduce your reliance on credit, avoid unnecessary interest, and move forward confidently toward your long-term financial goals.

Setting specific, measurable goals for the remainder of the year helps you stay on track with your financial reset. Instead of vague intentions like "save more," commit to exact targets: "Add $2,000 to my emergency fund by December" or "Reduce credit card debt by $5,000 before year-end."

Budget tracking tools make this process much simpler. Apps like Mint, YNAB, or your bank's built-in financial management features can automatically categorize spending and highlight progress toward savings goals. Many also allow you to set up automatic savings or debt payments transfers, removing the temptation to skip a month.

Schedule regular financial check-ins with yourself (or your partner). Monthly reviews work best for most people, allowing you to catch problems early without becoming obsessive about numbers. During these sessions:

Your credit score and net worth are valuable indicators of overall financial health. Track both quarterly to spot trends and address issues promptly.

Remember that life changes constantly, so your financial plan should too. When circumstances shift—whether it's an unexpected expense or a surprise bonus—take time to reconsider your goals and adjust your strategy accordingly. This flexibility isn't a sign of poor planning but rather smart financial management.

Financial success in midlife isn't about perfect planning but consistent course correction. By making mid-year financial assessments a regular habit, you transform potential problems into manageable adjustments before they derail your progress. This proactive approach reduces stress and builds confidence in your financial future.

Remember that every financial decision you make today shapes your options tomorrow. The halfway point in the year offers the perfect opportunity to reset, refocus, and recommit to your most important financial priorities. Your future self will thank you for taking this time to make thoughtful adjustments now.

Disclaimer: The information provided in this blog post is for educational and informational purposes only and should not be considered as financial, legal, investment, or tax advice. Symple Lending is not responsible for any financial outcomes resulting from following the information or ideas shared in this blog. Every individual's financial situation is unique, and we strongly encourage readers to take their own circumstances into consideration and consult with a qualified financial, legal, tax, and investment advisor before making any financial decisions. Symple Lending does not provide financial, legal, tax, or investment advice.

Did you know that family caregivers provide nearly $873.5 billion worth of unpaid care annually in the United States? While the emotional commitment...

Did you know that 68% of adult children find discussing finances with their aging parents more uncomfortable than talking about their own death? It's...

Did you know that 56% of Americans couldn't cover an unexpected $1,000 expense from their savings? Many people mistakenly believe one financial...

Did you know that 61% of Americans report living paycheck to paycheck, according to a 2023 LendingClub survey? Even more surprising, this includes...

What are your long-term financial goals? How important is it that you are financially well-off in life? Are you making the right financial choices...

While 85% of Americans feel anxious about their finances, most popular guidance focuses on quick fixes and trending financial hacks. However, true...