Breanne Neely

Breanne Neely

Build an Emergency Fund Without Derailing Your Life

Life rarely goes exactly to plan. From sudden home repairs to urgent healthcare needs, staying prepared is essential. Unfortunately, the average US...

Did you know that 61% of Americans report living paycheck to paycheck, according to a 2023 LendingClub survey? Even more surprising, this includes 36% of those earning over $100,000 annually. The financial tightrope doesn't discriminate by income level.

Mid-year offers a perfect pause point to evaluate your financial journey before the holiday spending season arrives. Like checking your GPS halfway to your destination, this strategic pit stop allows you to recalibrate, address unexpected detours, and ensure you're still on track to reach your year-end financial goals.

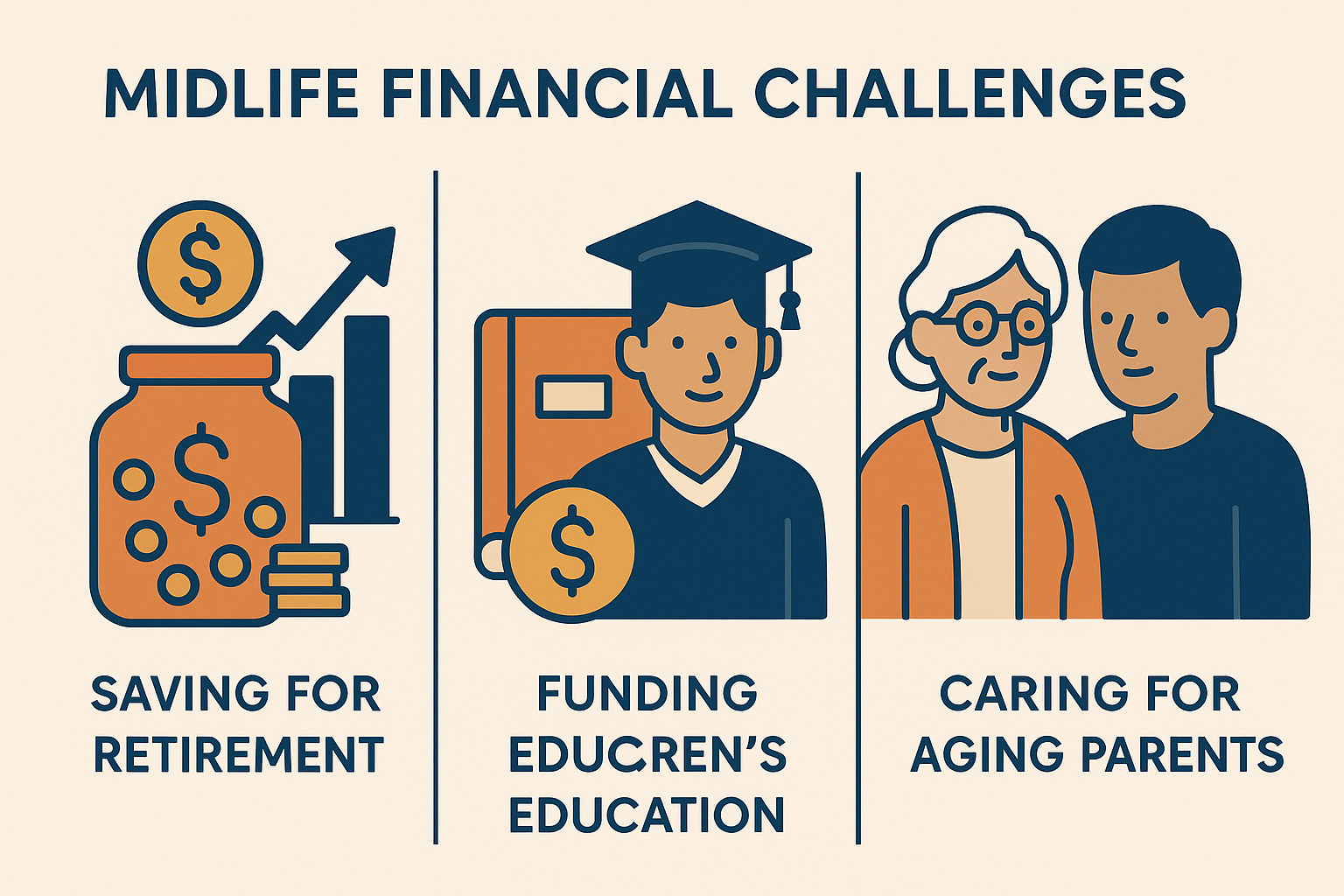

Balancing multiple financial responsibilities becomes particularly challenging during midlife. You might find yourself caught between saving for retirement, funding your children's education, and caring for aging parents—all at once. This juggling act can feel overwhelming, especially when unexpected events like medical emergencies or job changes throw your carefully laid financial plan off course.

A mid-year financial check-in gives you the perfect opportunity to assess if your current strategies are working. Are you making progress toward your goals, or do you need to adjust your approach? Taking stock now allows you time to make meaningful changes before year-end, rather than waiting until December when finances may be limited.

Taking time mid-year to review your monthly expenses can reveal important patterns that might be hidden in day-to-day spending. Look carefully at where your money has gone over the past six months—have grocery costs climbed? Are streaming subscriptions piling up? This review helps identify spending that doesn't align with your priorities.

Once you spot areas of wasteful spending, you can redirect those funds toward more meaningful goals. For example, money saved from unused subscriptions could boost your emergency fund or add to your retirement account.

Set specific, measurable mid-year financial targets based on what you've learned. Use current data—like actual utility costs from this year—to create a realistic budget for the coming months. Avoiding financial pitfalls in midlife depends on regularly assessing and adjusting your financial plan.

Taking full advantage of your employer's retirement plan match should be a top priority in your mid-year financial assessment. This is especially important if you're 50 or older and eligible for "catch-up contributions," which allow you to save beyond standard annual limits. For example, in 2025, older workers can contribute extra funds to their 401(k) plans above what younger employees are permitted.

Making adjustments to your contribution rates now, rather than waiting until December, gives you time to spread additional savings across several paychecks. This approach is less financially stressful than trying to make large lump-sum contributions to your retirement accounts at year-end. Create a simple timeline that outlines exactly when and how you'll increase your contributions for the remainder of the year, ensuring you don't leave any potential retirement savings on the table.

Financial experts consistently recommend keeping an emergency fund that covers three to six months of living expenses. This financial buffer protects you when unexpected costs arise—like sudden car repairs or medical bills—without forcing you to tap into retirement savings or rack up credit card debt.

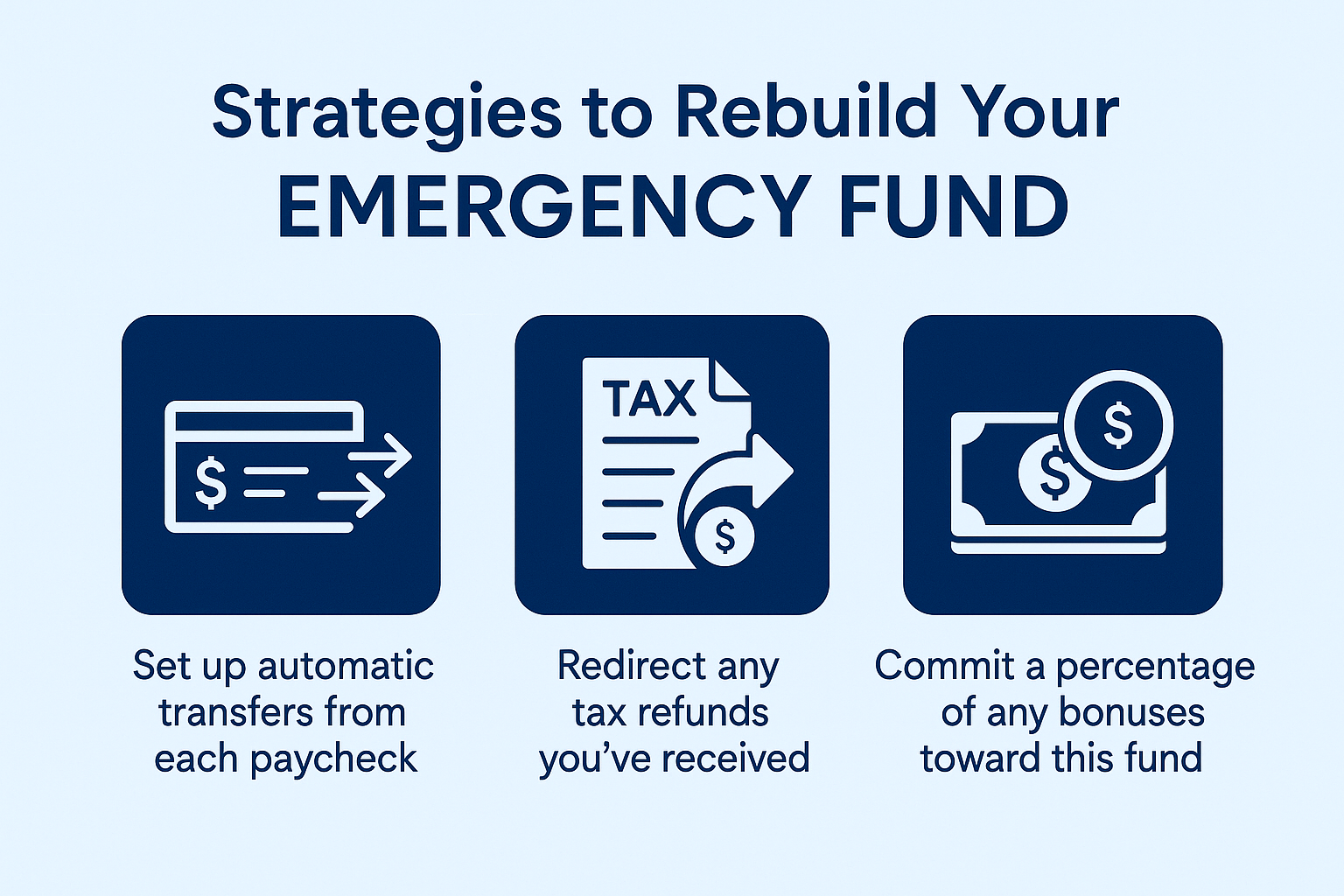

Mid-year is the perfect time to check if your emergency funds are adequate. If they've fallen short, implement simple strategies to rebuild: set up automatic transfers from each paycheck, redirect any tax refunds you've received, or commit a percentage of any bonuses toward this fund.

A well-stocked emergency fund does more than just prepare you for surprises—it creates peace of mind that carries into your year-end financial outlook. When you know you can handle unexpected financial challenges, you can focus more confidently on other financial goals without the constant worry of "what if" scenarios.

Taking a clear-eyed look at your current debts is one of the best financial moves right now. Start by creating a simple list of all your debts, noting interest rates, monthly payments, and remaining balances. Pay special attention to high-interest credit card balances, which can silently drain your financial resources month after month.

Consider these practical strategies to improve your situation:

These adjustments can free up monthly cash flow, allowing you to redirect money toward savings goals. Taking action on debt mid-year gives you time to see meaningful progress before December arrives.

Mid-year is the perfect time to review your savings plans, particularly tax-advantaged accounts like Health Savings Accounts (HSAs), IRAs, and 529 college savings plans. Take a close look at contribution levels and whether you're maximizing tax benefits available to you.

Make sure your savings strategies align with upcoming life changes. If your children are approaching college age, you might need to adjust your 529 plan contributions or begin thinking about how to access those funds efficiently.

Try these practical approaches to boost your year-end savings totals:

Small adjustments now can put you in a much stronger position by December, helping you avoid financial hardships as the year closes.

Market conditions often shift significantly within a year, making mid-year the perfect time to examine your investment allocations. Look at how your current portfolio balance compares to your original targets—have some investments grown to represent a larger percentage than you intended?

Consider any changes in your personal circumstances that might affect your investment strategy. Has your risk tolerance shifted? Are you closer to a major financial milestone like retirement or purchasing a home? These factors should guide your reallocation decisions.

Taking action now to adjust your mix of stocks, bonds, and cash helps you maintain an appropriate level of risk while positioning yourself for potential opportunities. Rather than reacting to market headlines, focus on your long-term goals and time horizon when making adjustments.

A thoughtful portfolio review during your mid-year financial check-in helps you stay on track with your investments while avoiding financial pitfalls as you approach year-end.

Mid-year is the perfect time to review all your insurance policies. Take a careful look at your health, home, life, and disability coverage to confirm they still match your needs. Has your family situation changed? Did you purchase valuable property? Did you switch jobs? Each of these events might require adjustments to your coverage.

Your estate planning documents need regular attention too. Check that your will, trusts, and beneficiary designations accurately reflect your current wishes. Many people forget to update beneficiaries after major life events like marriage, divorce, or having children.

Estate planning isn't just for the wealthy—it's a fundamental part of protecting your family's financial future. Without proper documentation, your assets might not transfer according to your wishes, potentially creating difficulties for those you care about most.

Mid-year is the perfect time to review your tax situation. Changes in income, job status, or family circumstances might mean your current withholding levels are no longer appropriate. Checking now helps you avoid unwelcome surprises like underpayment penalties or a large tax bill when you file.

Making adjustments at mid-year gives you plenty of time to spread any needed changes across remaining paychecks. For example, if you're currently underwithholding, increasing your withholding now over six months feels less painful than making dramatic changes in November or December.

Tax planning isn't separate from your other financial goals—it's an essential piece of your complete financial picture. Strategic tax management affects everything from retirement savings to investment decisions. Taking time now to fine-tune your tax approach provides peace of mind and potentially frees up resources for other priorities.

Technology can simplify your mid-year financial check-in process. Tools like YNAB (You Need A Budget) and Monarch help track your spending patterns, set alerts when you exceed budget categories, and visualize progress toward your goals.

These apps connect directly to your accounts, giving you real-time insights into your financial standing. Instead of manually tracking expenses in spreadsheets, let technology handle the heavy lifting.

The real benefit comes from accountability—seeing your actual spending habits displayed clearly makes it harder to ignore your financial blunders. Many apps also offer features to track your progress toward specific mid-year financial targets.

Consider setting up automatic bill payments and savings transfers. This "set it and forget it" approach reduces missed payments and helps you consistently build toward your financial goals without requiring constant attention.

Meeting regularly with a financial advisor throughout the year—not just during tax season—can make a significant difference in your financial health. These professionals offer perspective on your changing circumstances and can spot potential issues before they become problems.

When you schedule a mid-year review with your financial advisor, come prepared with updates about major life changes, questions about market conditions, and concerns about your progress toward goals. This preparation makes the meeting more productive and focused on actionable steps.

Advisors can help you interpret complex financial information, identify blind spots in your planning, and suggest adjustments to keep you on track. Their external perspective often reveals opportunities you might miss on your own, making these check-ins invaluable for your year-end financial positioning.

Setting realistic, measurable financial goals for the rest of the year helps focus your efforts where they matter most. Start by writing down specific targets with deadlines—"Save $2,000 for holiday expenses by November" is more effective than "save more money."

Break larger goals into smaller monthly milestones that feel manageable. For example, if you need to add $3,000 to your emergency fund by December, plan to save $500 monthly from July through December.

The benefits of acting now extend far beyond December 31st. Each financial goal you achieve builds confidence and creates momentum for your long-term financial security. Small wins today compound into significant progress over time.

Remember that financial planning isn't about perfection—it's about progress. Taking deliberate steps today, even modest ones, can significantly reshape your finances before year-end.

Taking action now, in the middle of your financial journey, gives you the runway needed to make meaningful changes before December's festivities and financial pressures arrive. Small adjustments in spending, saving, investing, and debt management during this mid-year checkpoint can create significant positive outcomes by year-end.

Remember that financial well-being isn't about perfection—it's about progress and awareness. By conducting a thoughtful mid-year money check, you're not just preparing for a stronger December balance sheet; you're building financial habits and mindfulness that will serve you well throughout your lifetime. The best time to course-correct is always now.

Disclaimer: The information provided in this blog post is for educational and informational purposes only and should not be considered as financial, legal, investment, or tax advice. Symple Lending is not responsible for any financial outcomes resulting from following the information or ideas shared in this blog. Every individual's financial situation is unique, and we strongly encourage readers to take their own circumstances into consideration and consult with a qualified financial, legal, tax, and investment advisor before making any financial decisions. Symple Lending does not provide financial, legal, tax, or investment advice.

Life doesn’t always follow a straight path—but with the right support, every turn gets easier. From surprise expenses to big plans, we’re here with fast, flexible funding to keep you moving.

Life rarely goes exactly to plan. From sudden home repairs to urgent healthcare needs, staying prepared is essential. Unfortunately, the average US...

The second half of the year is a practical window to review your financial progress, reset your goals, and build habits that can create real results...

Managing money doesn't have to be a stressful daily chore. If you want to achieve your financial goals faster, understanding how automating bills,...

1 min read

The second half of the year is a practical window to review your financial progress, reset your goals, and build habits that can create real results...

1 min read

A mid-year financial checkup helps you evaluate your savings, budget, and debt to ensure you remain on track for your annual goals. Taking time to...

1 min read

You can strengthen your finances for the rest of the year by updating your financial goals, tracking your spending, building emergency savings, and...