How to Have Effective Financial Conversations with Aging Parents: A Compassionate Guide

Did you know that 68% of adult children find discussing finances with their aging parents more uncomfortable than talking about their own death? It's...

9 min read

Did you know that 68% of adult children find discussing finances with their aging parents more uncomfortable than talking about their own death? It's a staggering statistic that highlights just how deeply entrenched our money taboos are. Many families face this challenge, often postponing these important conversations until a crisis forces the issue.

Yet these conversations aren't just necessary—they're acts of love. When approached with empathy and preparation, and by planning ahead, financial discussions with aging parents can transform from awkward encounters into meaningful opportunities to honor their independence while ensuring their security. Understanding the overall financial landscape is also crucial when having these conversations.

Let's face it—talking about money with your parents can feel awkward. Most of us were raised with the idea that financial matters are private, making these conversations particularly challenging. When roles begin to reverse and you need to discuss your parents' financial planning, it can feel like you're acknowledging their mortality, which nobody wants to confront. Elderly parents are especially vulnerable when these important conversations are delayed.

This discomfort is especially pronounced if you're part of the sandwich generation, simultaneously caring for your children while supporting aging parents. The emotional and practical stress can be overwhelming.

Despite the uneasiness, these conversations are necessary. Without proper planning:

Remember that discussing money isn't about taking control—it's about creating security and embracing discomfort for everyone involved. Start talking about finances early to avoid confusion and stress later on.

Before sitting down to talk about money with your aging parents, a little preparation goes a long way:

Do your homework first. Get familiar with your parents' financial situation—their assets, savings, insurance policies, and income sources. Understanding their health status is equally important, as it affects future care needs.

Know your own limits. Be honest with yourself about what you can realistically offer—whether that's financial support, time, or living space. Setting clear boundaries now prevents resentment later and helps you maintain control over your own personal finances.

Gather important paperwork. Having relevant documents handy keeps the conversation focused:

When handling sensitive information, make sure you comply with privacy laws to protect your parents' rights and ensure legal and ethical management of their finances.

This groundwork makes a potentially uncomfortable conversation more productive and less awkward for everyone involved.

Timing matters when discussing money with your parents. Avoid bringing up financial topics during stressful family gatherings or holidays when everyone's attention is divided. Instead:

The physical environment significantly affects how open your parents might be. A casual setting, like having coffee at their kitchen table, often works better than formal arrangements that might feel intimidating. Consider your parents' physical health to ensure they are comfortable during the conversation. The goal is to create an atmosphere where they don't feel pressured or defensive about sharing personal financial information.

The physical environment significantly affects how open your parents might be. A casual setting, like having coffee at their kitchen table, often works better than formal arrangements that might feel intimidating. Consider your parents' physical health to ensure they are comfortable during the conversation. The goal is to create an atmosphere where they don't feel pressured or defensive about sharing personal financial information.

The way you phrase your questions makes all the difference. When discussing finances with aging parents, your tone and word choice can either open doors or put up walls. Recognizing when an aging parent may need support with financial matters is an important step in ensuring their well-being and peace of mind.

Start by acknowledging their independence: "I respect that you've managed your finances well for decades. I'm just wondering if we could talk about future planning together?"

Focus on collaboration rather than taking charge. Instead of "You need to tell me about your finances," try "How can we work together to make sure you're comfortable in the years ahead?"

Some gentle conversation starters include:

Remember, your parents may fear losing control. Reassuring them that your goal is supporting their wishes—not replacing their judgment—builds trust and keeps communication flowing.

When talking with parents about money matters, deciding who else should be part of the conversation requires careful thought. Should siblings join the first discussion, or should you start one-on-one?

Consider these approaches:

When siblings are involved, keep these guidelines in mind:

Regular family check-ins help prevent misunderstandings and ensure everyone stays informed about changes in your parents' situation. This coordinated approach makes it easier to share responsibilities as needs change.

When you sit down for financial talks with your aging parents, tackle the most important matters first:

Start with immediate needs. Monthly bills, medical expenses, and health insurance should top your list. These affect day-to-day living and require regular attention. Paying bills and managing bill payments are key early topics, especially if your parents are starting to miss payments or need help organizing their finances.

Move to income sources. Discuss where money comes from—Social Security payments, retirement accounts, pensions, and investment income.

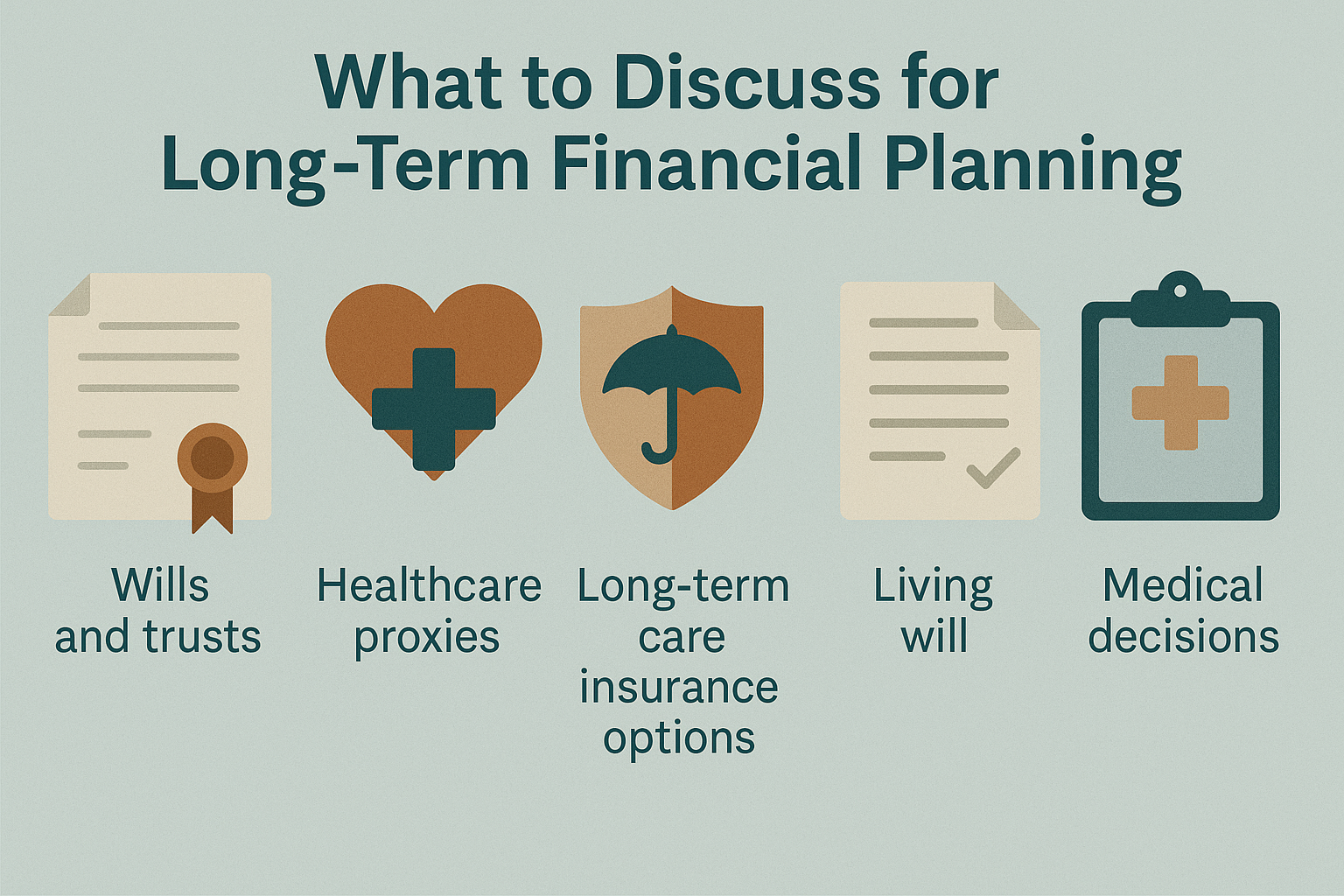

Address long-term planning next. This includes:

These are important legal documents for making financial and medical decisions if someone becomes mentally incapacitated. Early planning is crucial before cognitive impairment or a serious medical diagnosis occurs, to ensure your parents' wishes are respected and legal authority is established. If no planning is done, the court may need to appoint court appointed guardians to manage your elderly parents finances and make decisions on their behalf.

These are important legal documents for making financial and medical decisions if someone becomes mentally incapacitated. Early planning is crucial before cognitive impairment or a serious medical diagnosis occurs, to ensure your parents' wishes are respected and legal authority is established. If no planning is done, the court may need to appoint court appointed guardians to manage your elderly parents finances and make decisions on their behalf.

Don't forget about debts. Outstanding loans, credit card balances, and mortgages impact your parents' financial health.

Discuss housing preferences. Would they prefer to age in place? Move to assisted living? Understanding their wishes helps with future planning.

As your parents' needs change, you may need to take over their finances to protect their well-being. If you have joint accounts, be aware that when a parent dies, the account balance may automatically pass to the surviving owner, bypassing the will and probate process.

When storing important documents, consider safety deposit boxes as a secure option for wills, powers of attorney, and other legal documents.

By working through these topics systematically, you can make these difficult money conversations more manageable while ensuring nothing important gets overlooked.

One of the most important steps in managing your aging parents' financial affairs is organizing their financial and legal documents. This process goes beyond simply gathering paperwork—it's about creating a system that ensures nothing critical is overlooked when the time comes to take on financial responsibilities.

Start by working with your parents to collect all essential documents, such as wills, trusts, powers of attorney, insurance policies, and recent financial statements. Don't forget to include a list of account numbers, online banking passwords, and contact information for their financial advisors and institutions. Having a comprehensive inventory of these financial and legal documents will make it much easier to manage your parents' finances and pay bills on their behalf if needed.

Once gathered, store these documents in a secure location, like a fireproof safe or a safety deposit box, and make sure a trusted family member knows how to access them. Consider creating digital backups for added security. A financial advisor can help you develop a checklist and organizational system tailored to your parents' unique situation, ensuring that all financial affairs are in order and easily accessible when needed. This proactive approach not only streamlines future transitions but also provides peace of mind for both you and your parents.

Taking on the responsibility of managing an aging parent's finances means more than just handling their bills—it's about safeguarding their financial power and well-being. Begin by gaining a clear understanding of your parent's financial situation, including all income streams, regular expenses, and assets. Open communication is key: involve your parents in creating a budget and financial plan that reflects their wishes and priorities.

It's also important to include other family members in the decision-making process. Transparent discussions with siblings or other trusted relatives can help prevent misunderstandings and ensure everyone is on the same page regarding financial responsibilities. A financial planner can be invaluable in this process, helping to design a comprehensive plan that addresses your parents' current needs and long-term goals.

As you manage your parents' finances, be vigilant about potential risks such as elder fraud or cognitive decline. Establish safeguards, like dual signatures for large transactions or regular financial reviews, to protect your parents' assets and financial power. By working together as a family and seeking professional guidance when needed, you can help ensure your parents' financial situation is managed with care, respect, and in their best interests.

Protecting your aging parents from scams and identity theft is a crucial part of managing their finances. Older adults are often targeted by fraudsters, making it essential for adult children to take proactive steps to safeguard their parents' financial information.

Start by regularly monitoring your parents' financial accounts and credit reports for any unusual activity. Set up alerts for large transactions or changes in account information, and encourage your parents to be cautious about sharing personal details over the phone or online. Educate them about common scams that target older adults, such as fraudulent calls claiming to be from the IRS or fake charities.

A financial planner can help you develop a strategy to prevent elder fraud, including best practices for protecting sensitive information and responding quickly to suspicious activity. Make sure your parents know how to report scams and have a plan in place for freezing accounts or credit if necessary. By staying vigilant and working together, you can help protect your parents' finances and ensure their financial future remains secure.

Supporting aging parents while managing your own financial responsibilities creates a delicate balancing act. Many adult children find themselves caught between helping their parents and protecting their own financial future.

The financial impact can be significant:

To maintain your financial health while helping parents:

Remember that maintaining your financial well-being isn't selfish—it's necessary for sustainable caregiving that won't leave you depleted.

Sometimes family conversations about money reach a point where outside expertise becomes valuable. You might consider bringing in professionals when:

Consulting a financial professional can provide valuable guidance in navigating these situations and ensuring sound financial decisions.

Financial advisors, financial planners, elder law attorneys, and accountants offer neutral perspectives that can reduce family tension while providing expert guidance. They can help:

When selecting professionals, look for those experienced with senior finances. Ask about their fee structure upfront and whether they're willing to meet with multiple family members present.

Remember that professional help isn't just for wealthy families—even modest estates benefit from proper planning. Their guidance often pays for itself by preventing costly mistakes while giving everyone peace of mind.

Financial planning isn't a one-time event—it's an ongoing process that changes with your parents' health and circumstances. Think of these talks as regular check-ins rather than a single high-stakes discussion.

Make it routine. Schedule quarterly conversations to review finances and address any changes. These regular talks feel less threatening than emergency meetings. As your elderly parents' needs evolve, monitor for signs that they may require more support managing their finances.

Keep reassuring your parents. Remind them that everyone shares the same goal: their comfort, security, and independence for as long as possible. Phrases like "We're figuring this out together" help maintain dignity.

When discussing funding options for care needs:

Be alert for red flags, such as an elderly parent entering multiple contests or sweepstakes, which could indicate vulnerability to scams or financial exploitation.

The most successful families maintain open communication channels where concerns can be expressed without judgment. By normalizing these conversations, you make it easier for everyone to adapt to changing needs.

Remember, the hardest part is simply beginning. The first conversation opens doors for many more, each one becoming progressively easier. By approaching financial discussions with aging parents as an ongoing journey rather than a destination, you create space for adaptation as circumstances change.

Your willingness to navigate this territory—despite the discomfort—is one of the most profound ways to show care. These conversations aren't just about money; they're about preserving dignity, honoring wishes, and ensuring that your parents' golden years shine as brightly as possible.

Disclaimer: The information provided in this blog post is for educational and informational purposes only and should not be considered as financial, legal, investment, or tax advice. Symple Lending is not responsible for any financial outcomes resulting from following the information or ideas shared in this blog. Every individual's financial situation is unique, and we strongly encourage readers to take their own circumstances into consideration and consult with a qualified financial, legal, tax, and investment advisor before making any financial decisions. Symple Lending does not provide financial, legal, tax, or investment advice.

Did you know that 68% of adult children find discussing finances with their aging parents more uncomfortable than talking about their own death? It's...

Did you know that 56% of Americans couldn't cover an unexpected $1,000 expense from their savings? Many people mistakenly believe one financial...

Did you know that 78% of Americans live paycheck to paycheck, making them vulnerable when emergencies strike? Living paycheck to paycheck means any...

Did you know that the true cost of a personal loan can be up to 10% higher than the advertised amount due to hidden fees? While many borrowers focus...

Did you know that 78% of Americans live paycheck to paycheck, regardless of their income level? Financial wellness isn't just about how much money...

What are your long-term financial goals? How important is it that you are financially well-off in life? Are you making the right financial choices...