Breanne Neely

Breanne Neely

Build an Emergency Fund Without Derailing Your Life

Life rarely goes exactly to plan. From sudden home repairs to urgent healthcare needs, staying prepared is essential. Unfortunately, the average US...

Have you ever wondered if that $1,000 sitting in your savings account is enough to handle life’s curveballs? While financial experts toss around the “three to six months of expenses” rule, the reality of emergency funds is far more personal than most advice suggests.

The truth is, your financial safety net isn’t one-size-fits-all. The right emergency fund depends on your individual financial situation, needs, and risk factors—there’s no universal answer. Whether you’re a freelancer with irregular income or a government employee with job security, your emergency fund needs are as unique as your financial fingerprint. Let’s explore building a cushion that fits your life—not someone else’s guidelines.

An emergency fund is a dedicated savings account set aside specifically for unexpected expenses. This is your money set aside as a reserve to cover emergencies, ensuring you have funds available when the unexpected happens. Unlike your regular savings account that might be earmarked for vacations or big purchases, this financial buffer exists solely for unplanned situations like sudden job loss, medical emergencies, or urgent home repairs.

Think of it as your financial safety net that:

Your emergency savings fund serves one clear purpose: to keep your financial life stable when life throws its inevitable curveballs. When your car suddenly needs a major repair or you face an unexpected medical bill, having this dedicated account means you can handle these situations without derailing your broader financial goals.

The most common recommendation from financial experts is to save between three and six months’ worth of essential living expenses in your emergency fund. This guideline gives you enough financial cushion to weather significant disruptions like job loss or major unexpected costs without using credit cards or loans.

This timeframe works because it typically provides:

While these benchmarks serve as helpful starting points, your situation might call for adjustments. Someone with irregular income or significant family responsibilities might aim for six months or more, while a person with multiple income sources might feel secure with three months of savings.

Remember, any emergency savings are better than none—even a modest fund of $500-$1,000 can handle many common unexpected expenses.

To build an effective emergency fund, you must know exactly how much you spend on essentials each month. Focus on these non-negotiable expenses:

How to calculate your monthly requirements:

For example, if your core expenses total $3,000 monthly, a three-month emergency fund would be $9,000, while a six-month fund would be $18,000.

Use budgeting apps or spreadsheets to track these expenses accurately and update your calculations periodically as your financial situation changes.

Looking at a target of three to six months’ worth of expenses can feel overwhelming when you’re just starting out. Instead of getting discouraged, begin with a smaller, more achievable goal—$500 or $1,000. Start saving as soon as possible, even if the amount is small, to begin building your emergency fund. This initial safety net can cover many common emergencies and give you momentum.

What matters most is establishing the habit of consistent saving. Developing a savings habit through regular contributions is crucial for long-term financial stability. Setting aside $25 or $50 per paycheck gradually builds your financial cushion. As your situation improves, you can increase your contributions. Setting clear savings goals can help motivate your progress and allow you to track your achievements.

Remember that:

The key is making a start—no matter how modest—and building from there. Your emergency savings will grow over time as you develop this essential financial habit.

Effectively managing your cash flow is the backbone of building a strong emergency fund. Cash flow simply means tracking the money coming in and going out of your accounts each month. By understanding where your income is going, you can identify opportunities to save more and set aside money for unexpected expenses.

Start by reviewing your monthly income and expenses, including essentials like rent or mortgage payments, utilities, groceries, and debt obligations. Look for areas where you can cut back—maybe dining out less often or canceling unused subscriptions. Even small adjustments can free up extra funds to boost your emergency savings.

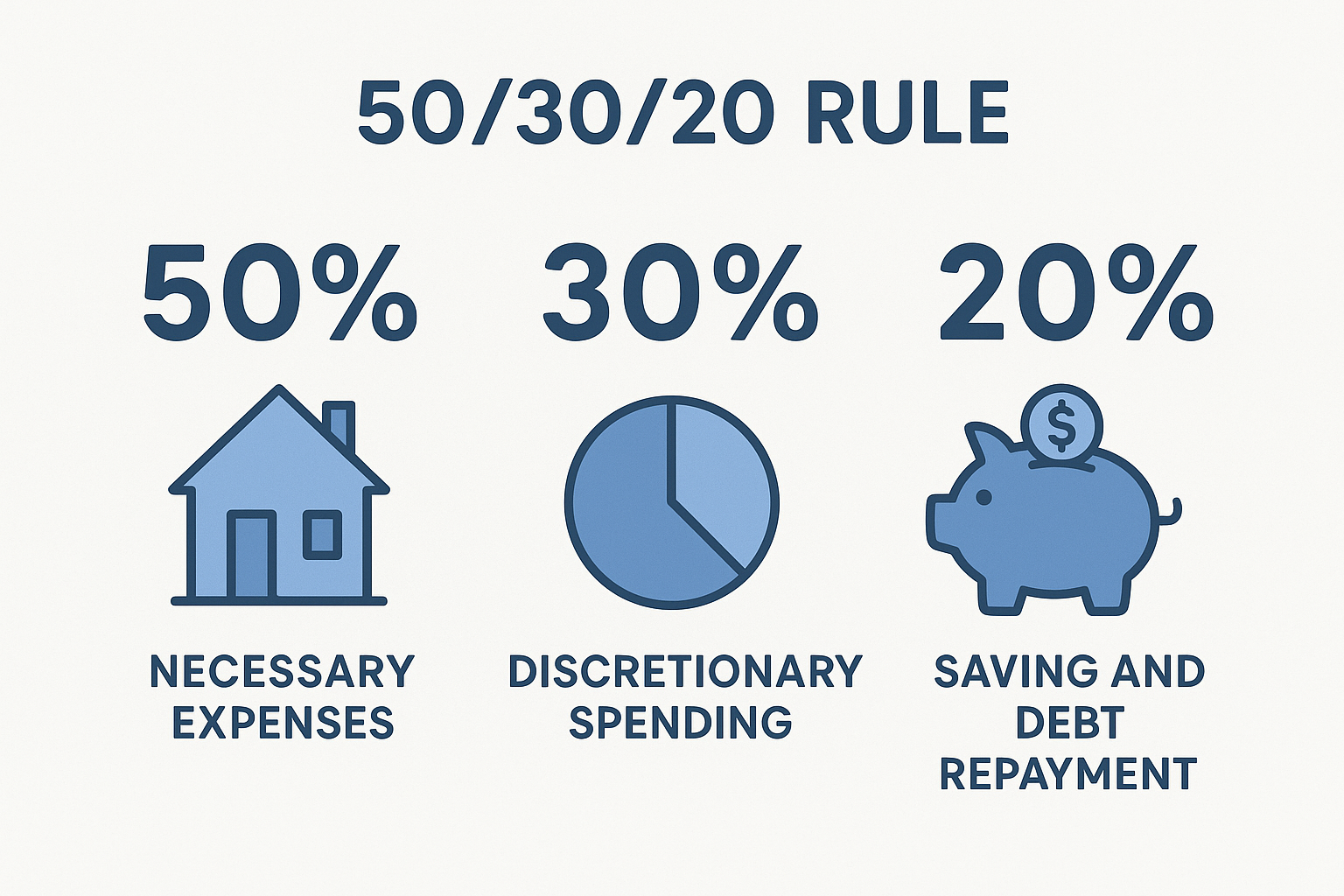

A popular approach is the 50/30/20 rule: Allocate 50% of your income to necessary expenses (like rent or mortgage payments), 30% to discretionary spending, and 20% to saving and debt repayment. This framework helps ensure you consistently set money aside for your financial safety net.

Leverage budgeting apps or simple spreadsheets to track your cash flow and monitor your progress. By making saving automatic—such as setting up direct deposit into your emergency fund—you’ll build your financial safety net with less effort. Remember, every bit counts, and managing your cash flow wisely is key to covering unexpected events and building lasting financial security.

Your ideal emergency fund size should be tailored to your specific life situation. Several key factors will influence how much you should save:

Rather than following generic guidelines, assess your personal risk profile honestly. Developing a personalized savings strategy is essential to ensure your emergency fund matches your unique needs and expenses. A family with a stable government job might be comfortable with three months saved, while a self-employed contractor supporting dependents might need nine months or more for true financial security.

Let’s look at how emergency fund needs vary across different household situations:

Single person with stable job: Maria works as a nurse with a reliable income and minimal financial obligations. She feels comfortable with a three-month emergency fund of $9,000 (based on $3,000 monthly expenses).

Dual-income couple: James and Alicia both work full-time. They maintain a four-month fund of $16,000 with two income sources, knowing they’re unlikely to both lose income simultaneously.

Single parent: Robert supports two children on one income. Given his greater responsibility, he prioritized building a six-month fund of $24,000 to provide extra security.

Small business owner: Samantha experiences variable income in her consulting practice. She maintains an eight-month personal emergency fund plus a separate three-month business expense reserve.

Your emergency savings requirements will shift with major life changes. When Alex and Tina had their first child, they increased their fund from four months to six months to account for potential childcare costs and medical expenses. As their needs grew, they prioritized contributing more money to their emergency fund to ensure greater financial security.

Life rarely stays the same, and your emergency fund needs should change accordingly. Major life events often bring new financial responsibilities that require a larger safety net:

Make reviewing your emergency savings a routine part of your financial planning—at least annually or whenever your life circumstances change significantly. Ask yourself: "Would my current fund adequately protect me if an emergency happened today?"

The key is staying flexible. Your financial safety net should grow and adapt as your life evolves and your responsibilities change.

Starting your emergency fund doesn’t need to be complicated. Here’s how to begin:

For safe storage, choose:

Retirement accounts are unsuitable for emergency funds due to market risk, tax implications, and penalties for early withdrawal.

Remember to keep your emergency savings liquid and accessible—this isn’t money for investing. Emergency funds should not be used for daily spending and should be reserved for true emergencies. You need to withdraw them quickly without penalties when emergencies strike. With certificates of deposit (CDs), early withdrawal penalties may apply if you access funds before maturity, making them less ideal for emergency savings.

Accounts with FDIC insurance for protection are important, but not all investment and insurance products are insured by a federal government agency, so federal oversight is key for your security.

Choosing the right place to keep your emergency fund is just as important as building it. The goal is to keep your emergency savings in a low-risk, easily accessible account so you can cover unexpected expenses without delay.

High-yield savings accounts are a top choice for emergency funds. They offer competitive interest rates, helping your savings grow faster than in a standard savings account while providing easy access to your money. Look for accounts insured by the Federal Deposit Insurance Corporation (FDIC) or, if you prefer a credit union, by the National Credit Union Administration (NCUA). This insurance protects your funds up to the federal limit, giving you peace of mind.

Money market accounts and money market funds are also solid options. They typically offer higher interest rates than regular bank accounts and allow you to withdraw money quickly when needed. Just make sure to check for any minimum balance requirements or withdrawal limits.

It’s best to avoid investing your emergency fund in stocks or mutual funds, which carry market risk and may not be easily accessible in a pinch. The priority is safety and liquidity, not chasing high returns. By keeping your emergency fund in a high-yield savings account, money market account, or similar low-risk, FDIC-insured account, you’ll ensure your money is there when you need it most.

Knowing when to tap into your emergency fund is essential for maintaining financial security. Your emergency fund is designed to cover unexpected expenses critical to your health, safety, or financial well-being, such as medical bills, urgent car repairs, or an unexpected job loss.

Before using your emergency fund, ask yourself: Is this expense truly unexpected and necessary? If it’s something like a sudden medical bill, a major home repair, or covering living expenses after a job loss, your emergency fund is there to help. However, avoid dipping into these savings for non-essential purchases, planned expenses, or luxuries—using your fund for these can leave you vulnerable when real emergencies strike.

If you need to use your emergency fund, prioritize replenishing it as soon as possible. This ensures you’re always prepared for the next unexpected expense and helps maintain your financial security over the long term.

Finding the right balance between building an emergency fund and paying off debt is key to achieving financial well-being. While saving for unexpected expenses is important, tackling high-interest debt—like credit card balances—should also be a priority.

A smart strategy is to split your available income between debt repayment and emergency savings. For example, you might dedicate a portion of each paycheck to paying down high-interest debt while still contributing regularly to your emergency fund. This approach helps you avoid accumulating more debt in the future and ensures you’re making progress toward both financial goals.

Consider options like debt consolidation or balance transfer credit cards to manage high-interest debt more efficiently. Remember, building an emergency fund and reducing debt go hand in hand regarding financial security. By striking a balance, you’ll protect yourself from financial emergencies and set yourself up for long-term financial success.

Creating multiple income streams is a powerful way to strengthen your financial safety net and accelerate your emergency fund growth. Relying on a single source of income can leave you vulnerable to job loss or unexpected expenses, but diversifying your income provides extra security.

Consider starting a side hustle, freelancing, or exploring gig economy opportunities to bring in additional money. Renting out a spare room, selling products online, or investing in dividend-paying assets are other ways to supplement your main income. The key is to direct this extra income toward your emergency fund and other financial goals, rather than increasing your day-to-day expenses.

You’ll be better equipped to handle financial shocks and unplanned expenses by building multiple income streams. This proactive approach helps you build your emergency fund faster and supports your overall financial well-being and long-term security.

If building your emergency fund feels overwhelming, you're not alone. Remember:

The goal isn't perfection—it's building financial resilience. A partial emergency fund will still help you handle unexpected costs better than having no savings at all.

Remember that your emergency fund is a journey, not a destination. As you watch that dedicated account grow from your first $100 to eventually reaching your target, each dollar represents a bit more peace of mind and financial resilience.

Don't let perfection be the enemy of good when it comes to your safety net. Even a small emergency fund can prevent a minor setback from becoming a financial disaster. Start where you are, save what you can, and adjust as your life evolves. Your future self will thank you when that inevitable rainy day arrives.

Disclaimer: The information provided in this blog post is for educational and informational purposes only and should not be considered as financial, legal, investment, or tax advice. Symple Lending is not responsible for any financial outcomes resulting from following the information or ideas shared in this blog. Every individual's financial situation is unique, and we strongly encourage readers to take their own circumstances into consideration and consult with a qualified financial, legal, tax, and investment advisor before making any financial decisions. Symple Lending does not provide financial, legal, tax, or investment advice.

Life doesn’t always follow a straight path—but with the right support, every turn gets easier. From surprise expenses to big plans, we’re here with fast, flexible funding to keep you moving.

Life rarely goes exactly to plan. From sudden home repairs to urgent healthcare needs, staying prepared is essential. Unfortunately, the average US...

The second half of the year is a practical window to review your financial progress, reset your goals, and build habits that can create real results...

Managing money doesn't have to be a stressful daily chore. If you want to achieve your financial goals faster, understanding how automating bills,...

1 min read

Your savings account can take years to build, but a few unplanned expenses can reduce that balance much faster than many people expect. Understanding...

1 min read

Nearly 4 in 10 Americans say they couldn't spare $400 to cover unexpected expenses without borrowing, and yet, surprise costs hit almost everyone at...

1 min read

If you are facing a sudden bill without money set aside, it is important to know that you are not alone and you still have options. This guide...