Track Spending in 10 Minutes a Week: A Lightweight System That Sticks

Managing your money shouldn't require hours of complex spreadsheet work. If you need to manage personal finances with a busy schedule, adopting a...

3 min read

Life doesn’t always follow a straight path—but with the right support, every turn gets easier. From surprise expenses to big plans, we’re here with fast, flexible funding to keep you moving.

Managing your money shouldn't require hours of complex spreadsheet work. If you need to manage personal finances with a busy schedule, adopting a...

A budget reset involves reviewing your income sources, prioritizing essential expenses, and reducing variable costs to align with your current...

Have you ever felt wealthy checking your balance, only to remember a large insurance bill is due next week? According to financial experts, leaving...

1 min read

Ever applied for a loan and felt like you were just crossing your fingers, hoping for the best? There’s a key number that heavily influences loan...

1 min read

When it comes to choosing a loan, one of the most significant decisions you'll face is the length of the loan term. This choice directly influences...

1 min read

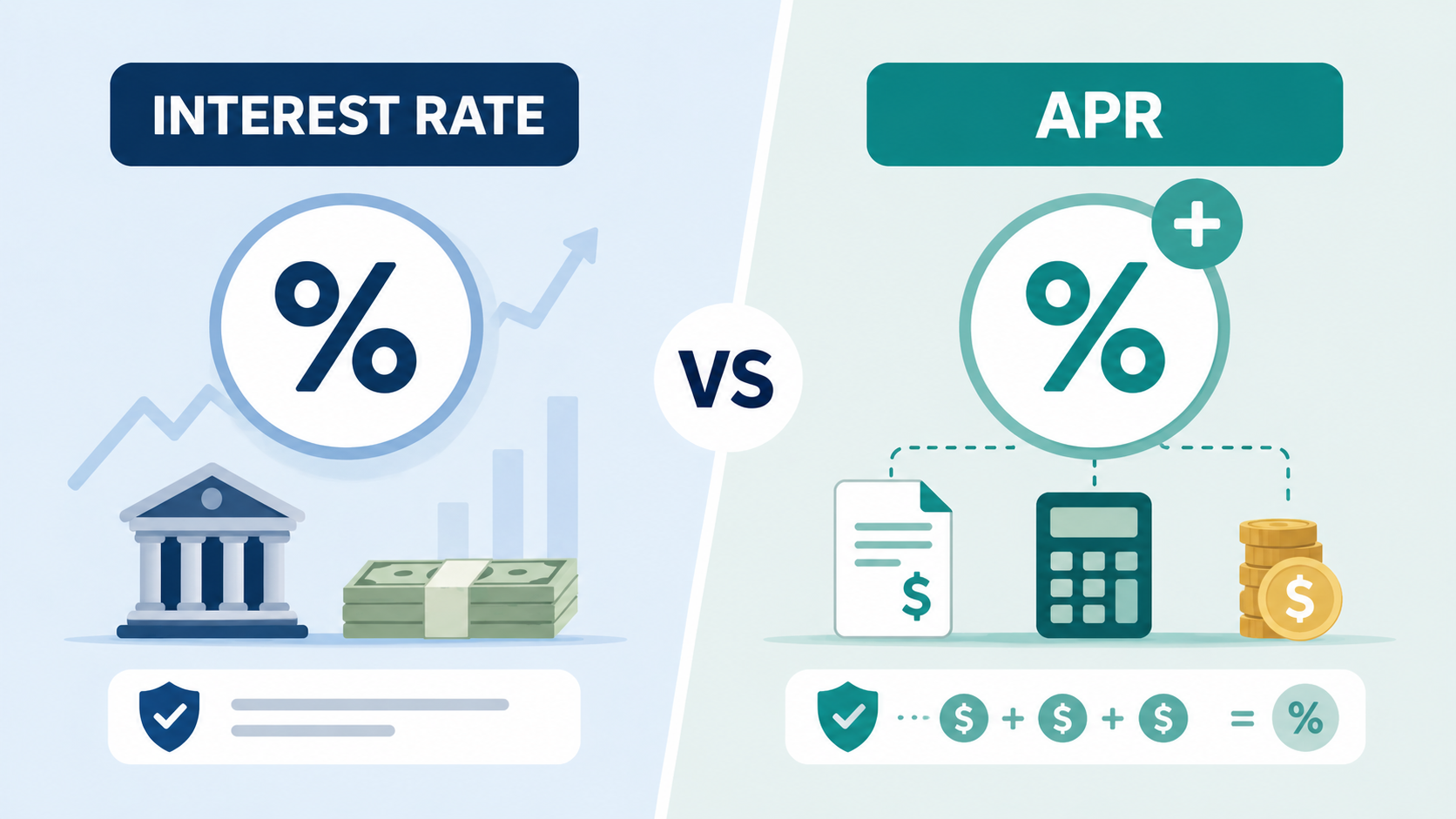

When shopping for a mortgage, auto loan, or credit card, you will inevitably encounter two crucial numbers. Understanding APR vs. Interest Rate:...