How to Master Money Talks After 40: The Couple's Guide to Financial Clarity and Communication

Did you know that nearly 70% of couples argue about money, regardless of how much they have? These conversations are significant for those over 40,...

10 min read

Did you know couples who talk regularly about money are more likely to report financial satisfaction and stronger relationships? Yet after 40, these conversations often become more complex as retirement looms closer and financial priorities shift. The stakes are higher, with less time to recover from financial missteps.

Financial communication in midlife relationships isn't just about tracking expenses or planning for retirement. It's about navigating changing identities, evolving priorities, and addressing the emotional weight that money carries after decades together. As your financial landscape transforms, so too must the ways you communicate about the dollars and cents that shape your shared future.

Financial planning becomes even more essential as you move through your 40s and beyond. At this stage in life, you and your spouse may be juggling competing priorities—preparing for retirement, supporting family members, or simply wanting to enjoy more of what life offers. Creating a comprehensive financial plan together helps you align your financial goals and personal values, ensuring you're both working toward the same vision of financial security.

A well-crafted financial plan can help you reduce financial stress, make informed choices, and achieve the lifestyle you both desire in retirement and throughout your future together. Whether you're just starting to think seriously about your long-term finances or looking to refine your existing plan, a financial advisor or other financial professional can help you create a strategy tailored to your unique needs and circumstances. By prioritizing financial planning as a couple, you lay the groundwork for a strong foundation and a more confident financial journey ahead.

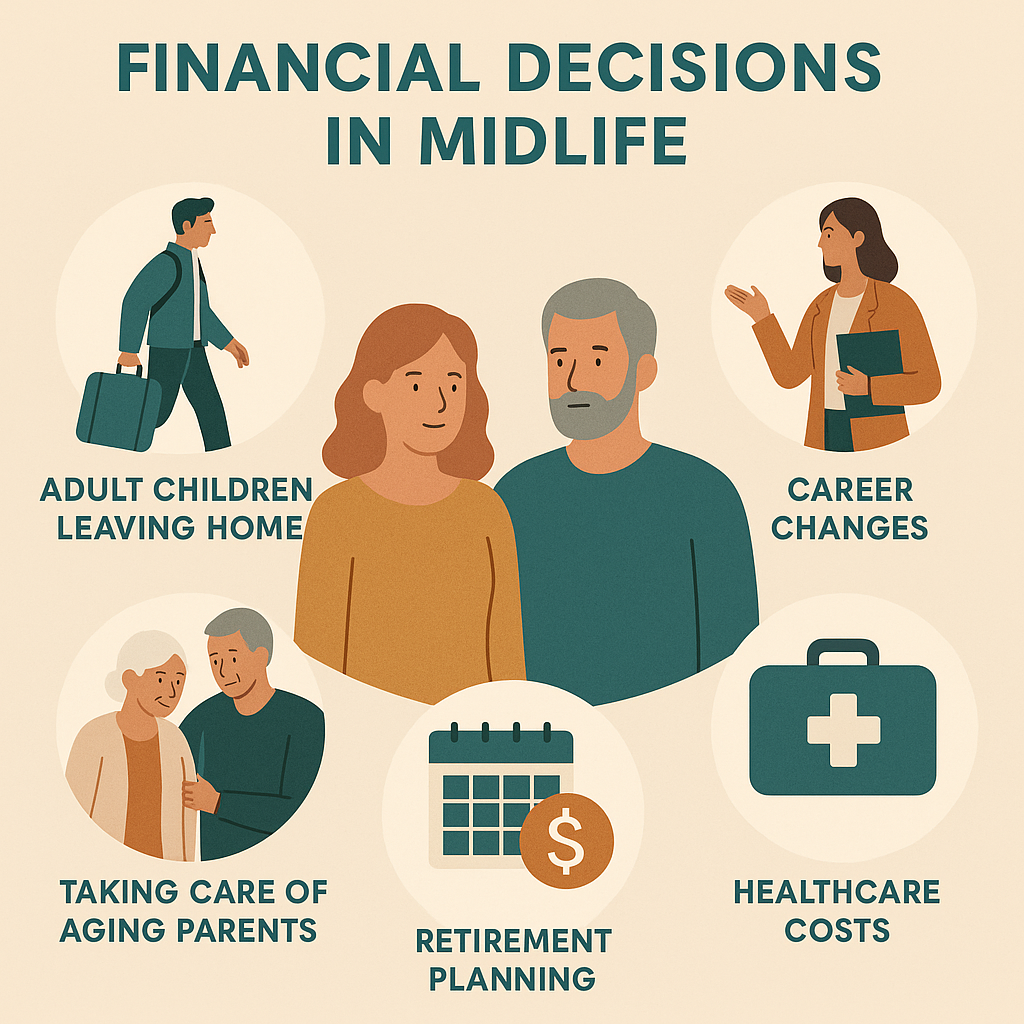

Financial conversations often become more complex after 40, as couples face new money challenges. The financial dialogue shifts from immediate concerns like home buying to longer-term needs like retirement planning and healthcare costs.

Take time to reflect on how your financial choices and core beliefs have evolved over the years, and consider how these changes influence your current approach to money as a couple.

As life transitions occur—children leaving home, career changes, or caregiving responsibilities—couples need to revisit how they communicate about money. These changes require:

Regular review of your financial communication approach helps support your evolving partnership needs in midlife and beyond. Reflecting on your financial journey and re-evaluating your strategy as your partnership evolves can help ensure your financial decisions align with your true priorities.

Regular review of your financial communication approach helps support your evolving partnership needs in midlife and beyond. Reflecting on your financial journey and re-evaluating your strategy as your partnership evolves can help ensure your financial decisions align with your true priorities.

Our upbringing directly shapes our financial habits and attitudes. How your parents handled money likely influences your approach today, while your partner may carry completely different lessons from their family.

Taking time to discuss each person's financial values reduces future conflict. Understanding the "why" behind financial behaviors creates empathy rather than frustration.

Try asking each other:

Frame these conversations around curiosity and shared goals, avoiding judgment about different perspectives. This foundation helps build mutual respect for your ongoing money talks.

Before you can chart a course toward your financial goals, getting a clear picture of where you stand today is important. As a couple, take time to gather all your financial information—this includes your income, monthly expenses, outstanding debts, retirement savings, and other investments. Don’t forget to include all assets, such as savings accounts and property, as well as any liabilities.

Working together to assess your current financial situation helps you identify strengths and areas for improvement. Be open and honest about your financial habits and any concerns you may have. This transparency is key to building trust and ensuring your financial plan reflects both partners’ priorities. If you’re unsure where to start, a financial professional can help you organize your finances and set realistic long-term goals, such as boosting your retirement savings or updating your estate plan. By creating a shared understanding of your finances, you’ll be better equipped to make decisions that help you achieve your dreams for retirement and beyond.

Setting up safe spaces for financial discussions starts with removing blame and criticism. Many couples struggle with money talks due to embarrassment, fear of judgment, or resentment over different financial habits.

To build mutual respect during these conversations:

To build mutual respect during these conversations:

When tensions rise, take a short break rather than continuing unproductively. Remember that you are partners working toward shared financial security, not opponents in a financial debate.

For couples over 40, regular money check-ins prevent financial surprises and help address new issues before they become problems. Most financial advisors recommend setting aside specific times—monthly or quarterly—to review your financial picture together. During these meetings, it's important to regularly review your financial goals and habits to ensure they still align with your values and make adjustments as needed.

A productive financial meeting might include:

These structured conversations keep both partners informed and invested in decisions. They’re especially important during life transitions like children leaving home, career changes, or approaching retirement. Treating these meetings as a priority builds financial teamwork and reduces stress about money matters.

When both partners align on financial goals, it builds a stronger foundation for your future together. Start by individually listing your financial priorities—retirement timing, travel plans, helping adult children—then come together to discuss where you agree and where compromise is needed.

A practical approach:

As circumstances change—children leave home, careers shift, or health needs arise—regularly revisit these priorities. What seemed important at 40 might look different at 50 or 60. This ongoing conversation ensures both your visions remain respected as you move through midlife together.

Life is full of unexpected twists, and an emergency fund is vital to any solid financial plan. As a couple, aim to save at least three to six months’ worth of living expenses in a dedicated savings account. This emergency fund acts as a financial safety net, helping you cover sudden expenses like medical bills, car repairs, or even a temporary loss of income without relying on debt.

A financial advisor can help you determine the right emergency fund target for your unique situation, considering your lifestyle, job stability, and other factors. By prioritizing this savings goal, you can reduce financial stress and protect your long-term financial goals from unexpected setbacks. Knowing you have a cushion in place allows you to focus on building wealth and enjoying life, rather than worrying about what might go wrong.

Creating a budget together strengthens financial teamwork after 40. Start with these practical steps:

Transparency is essential—both partners should know where money is going. Regular check-ins help prevent misunderstandings and build financial compatibility.

Include personal spending allowances within your joint budget. This respects individual interests while maintaining shared financial goals. Couples can openly discuss how they want to spend money so that both individual and shared priorities are reflected. When each person has some financial freedom within agreed boundaries, resentment decreases, and banking on love grows stronger.

Tackling debt and managing expenses together is a cornerstone of effective financial planning for couples. Start by listing all your debts—credit cards, loans, and other obligations—and create a plan to pay off high-interest balances first. Review your monthly expenses, including discretionary expenses, and look for opportunities to cut back or redirect spending toward your financial goals.

Consider setting up a budget that reflects your needs and wants, making sure to allocate resources for essentials while allowing flexibility. A financial professional can help you develop a debt management strategy and suggest ways to save more money each month. By working as a team to manage your money, pay down debts, and control expenses, you’ll free up more resources to invest in your future and achieve your shared financial dreams.

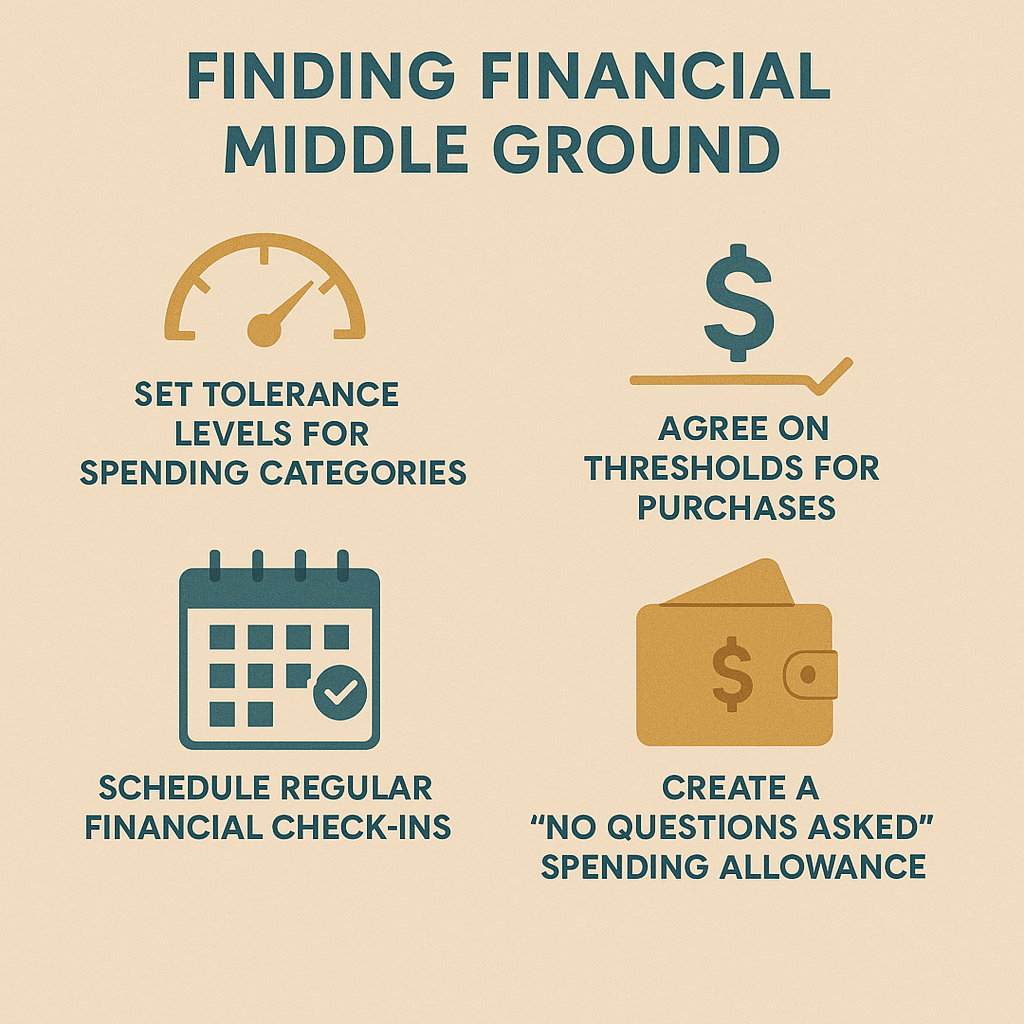

Money conflicts often stem from different spending habits and hidden expenses, sometimes called "financial infidelity." Tension can build quickly when one partner is a saver and the other a spender.

Try these practical techniques for finding middle ground:

The goal isn't for both partners to become identical in their money habits, but to validate each approach while establishing shared ground rules. This balance respects individual autonomy while protecting your joint financial health and communication.

Investing wisely and safeguarding your assets are key steps in building long-term financial security. As a couple, discuss your retirement goals and consider contributing regularly to retirement accounts, such as 401(k)s or IRAs. Evaluate your investment choices together, taking into account your risk tolerance, time horizon, and overall financial plan. A financial advisor or financial professional can help you create an investment strategy that aligns with your values and helps you achieve your financial goals.

Don’t overlook the importance of protecting what you’ve built. Review your insurance policies—including life insurance, health insurance, and disability insurance—to ensure your family is covered in case of unexpected events. Estate planning is also crucial; work together to create or update your will, establish a trust if needed, and plan to distribute your assets to future generations. Regularly reviewing your financial plan with a professional can help you stay on track, make informed decisions, and adjust your strategy as your life and goals evolve. Investing for the future and protecting your assets creates a legacy of financial security for your family and peace of mind for yourselves.

Retirement planning ranks among the top financial stressors for couples over 40. Having open conversations about your readiness helps ensure both partners feel comfortable with future plans. Managing cash flow is especially important in retirement planning to maintain a stable income and cover ongoing expenses.

Estate planning and potential caregiving needs should be approached proactively rather than reactively. These discussions go more smoothly when framed as collective preparation rather than dwelling on worries.

Consider discussing:

When evaluating retirement income sources, consider other assets such as pensions or life insurance cash value to diversify your income and provide additional financial security. Married couples can also optimize Social Security and survivor benefits by coordinating claiming strategies to maximize household income.

Regular reviews of these plans become essential as your needs evolve. When both partners participate in these sometimes uncomfortable conversations, you build financial resilience together while reducing anxiety about the future.

Financial management roles often need to shift as couples move through midlife. Health changes, job transitions, or new caregiving duties may require reassigning who handles which money tasks.

When life circumstances change:

This flexibility prevents overload when one partner faces new demands. For example, if one spouse takes on parent care, the other might temporarily manage more bill payments or investment oversight.

Regular check-ins about how financial responsibilities are working help maintain balance as your partnership adapts to life’s changes.

Sometimes financial conversations benefit from outside expertise. A financial planner or counselor can provide structure, specialized knowledge, and neutral mediation for emotionally charged money topics.

When selecting a professional:

Remember that professional guidance should inform—not override—your shared decisions. The best advisors help clarify options while respecting your unique financial relationship.

Consider getting help for complex situations like blending finances later in life, preparing for retirement, or managing inheritance questions. These experts can often suggest options neither partner has considered.

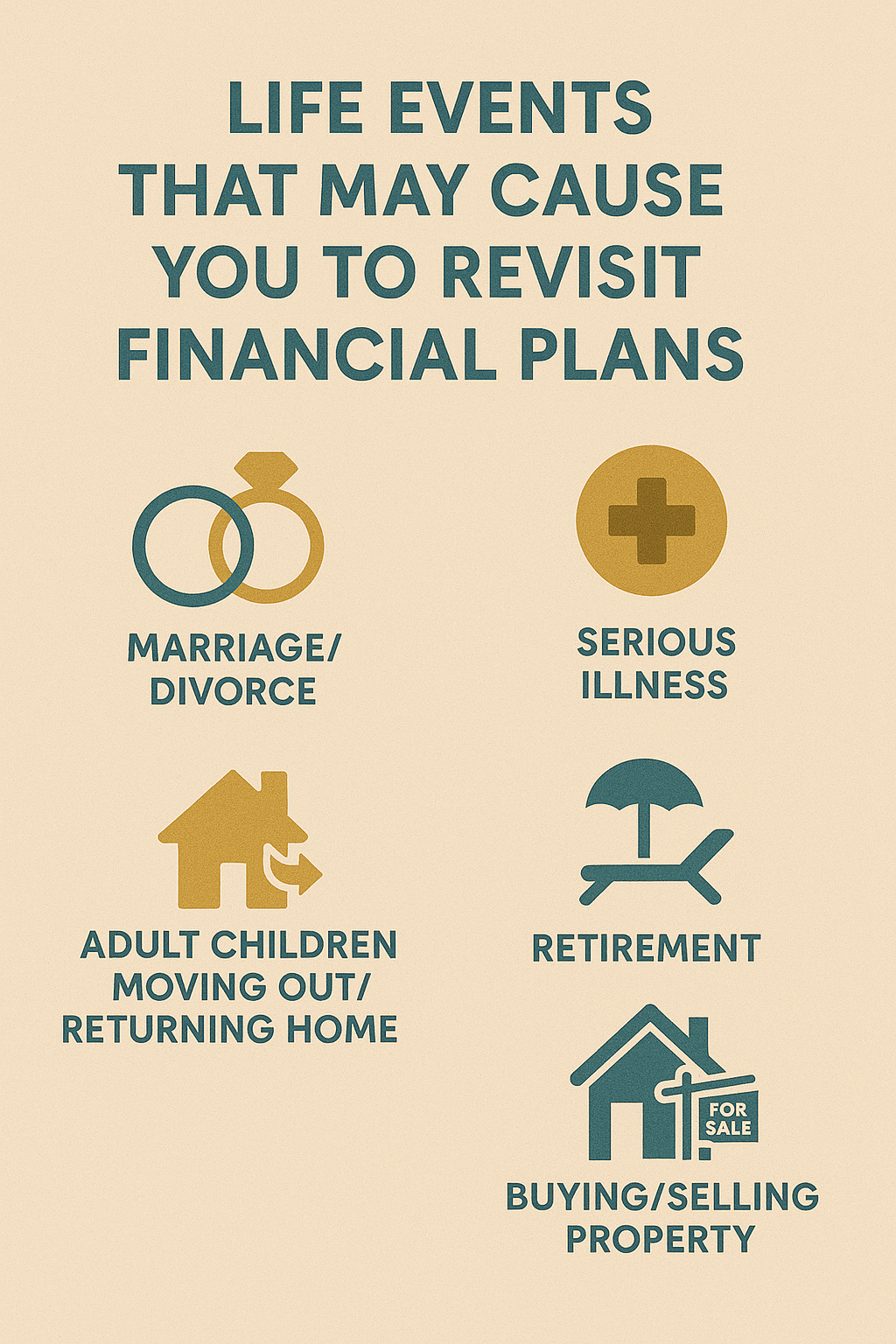

Life after 40 brings significant changes that impact your financial plans. Major events requiring updates include:

Think of your financial plan as a living document, not a static one. Review it at least annually and after every substantial life change. This helps you stay on track with your goals despite shifting circumstances.

Be willing to adapt your strategies to new realities. What worked in your 40s might need adjustment in your 50s and 60s as priorities evolve. As your financial goals and risk tolerance change with age, reviewing and adjusting your asset allocation is important to help manage risk and support your long-term objectives. This flexibility maintains your financial security while accommodating life’s inevitable changes.

Turning financial discussions into consistent action requires concrete accountability methods. Consider these practical approaches:

Define accountability for your partnership. Some couples prefer weekly quick checks, while others benefit from more detailed monthly reviews.

Remember to acknowledge your successes, both small and large. Celebrating financial wins reinforces your teamwork and makes money conversations more positive over time.

Starting money talks doesn’t have to be awkward. Try these conversation starters:

Keep discussions productive by:

Remember to celebrate your progress together. Acknowledge when you pay off debt, reach savings goals, or simply maintain a streak of regular money meetings. Take time to recognize how much you have saved so far—every milestone matters. These celebrations reinforce your partnership and make future financial conversations more appealing.

Financial communication after 40 isn’t just about money—it’s about continually building trust and partnership as your lives evolve. When you approach money conversations with openness, curiosity, and mutual respect, you create a foundation supporting your financial security and your relationship’s health. Aligning your financial plan with your personal values can also foster a sense of fulfillment and purpose in your relationship.

Remember that financial communication is a skill that improves with practice. Each conversation builds your capacity to navigate challenges together, whether planning for retirement, helping adult children, or adapting to unexpected life changes. By committing to honest dialogue about your resources, needs, and dreams, you’re investing in something far more valuable than any account balance—the strength and resilience of your partnership.

Disclaimer: The information provided in this blog post is for educational and informational purposes only and should not be considered as financial, legal, investment, or tax advice. Symple Lending is not responsible for any financial outcomes resulting from following the information or ideas shared in this blog. Every individual's financial situation is unique, and we strongly encourage readers to take their own circumstances into consideration and consult with a qualified financial, legal, tax, and investment advisor before making any financial decisions. Symple Lending does not provide financial, legal, tax, or investment advice.

Did you know that nearly 70% of couples argue about money, regardless of how much they have? These conversations are significant for those over 40,...

Did you know that 47% of adults in their 40s and 50s have a parent age 65 or older and either raise a young child or financially support a grown...

Did you know couples discussing finances at least once a month report significantly higher relationship satisfaction? Yet after 40, these...

What are your long-term financial goals? How important is it that you are financially well-off in life? Are you making the right financial choices...

Did you know that people who write down their financial goals are 42% more likely to achieve them? Yet, many of us still approach our money...

In today's world, where financial burdens have become a common aspect of many people's lives, it's essential to adopt proactive strategies to break...