How to Master Money Talks After 40: The Couple's Guide to Financial Clarity and Communication

Did you know that nearly 70% of couples argue about money, regardless of how much they have? These conversations are significant for those over 40,...

9 min read

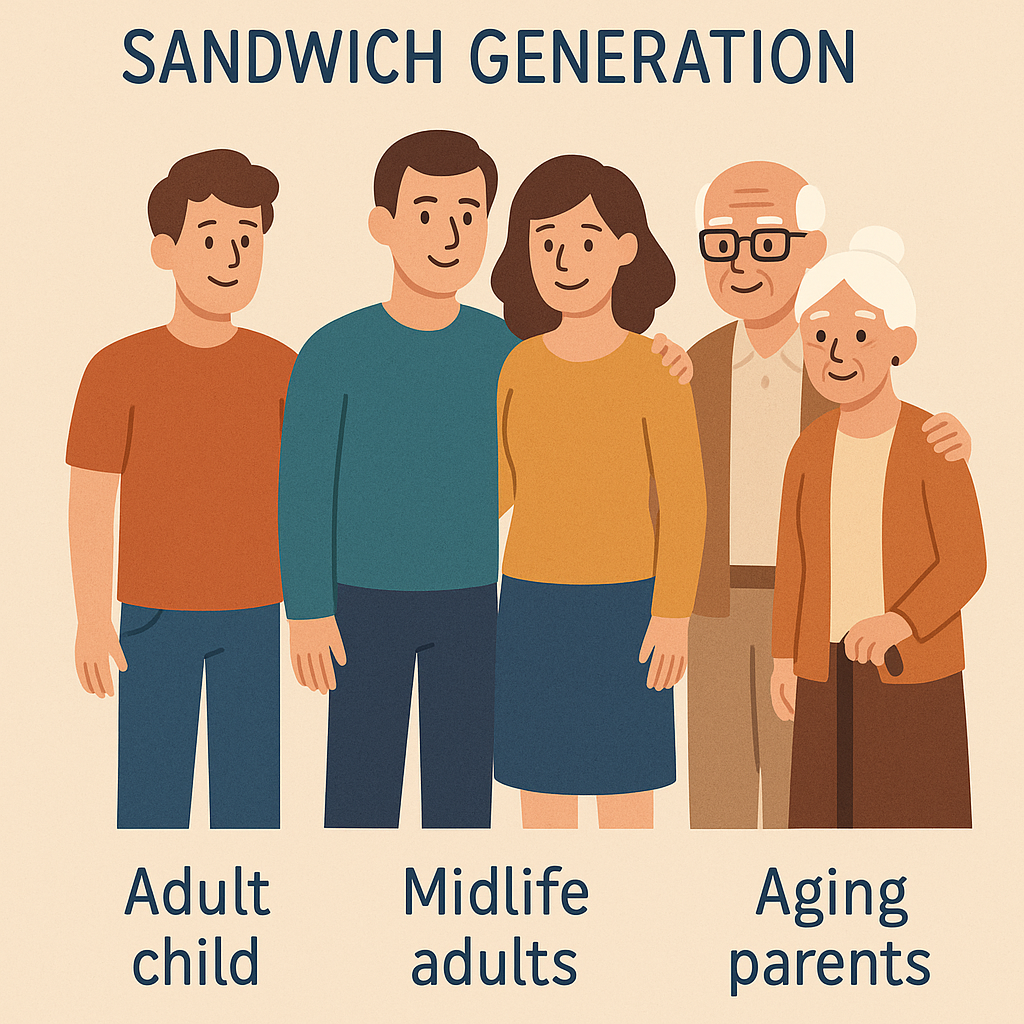

Did you know that 47% of adults in their 40s and 50s have a parent age 65 or older and either raise a young child or financially support a grown child? Welcome to the "sandwich generation," where your financial attention is constantly divided between aging parents, growing children, and your own future.

Balancing these competing priorities doesn't just strain your wallet; it tests your relationship. As couples navigate midlife's complex financial landscape together, the decisions you make now will echo for decades. The good news? With intentional planning and open communication, you can protect your financial future while supporting those who depend on you.

If you’re between 40 and 60 and support your children and aging parents while managing your own household, you’ve joined the “sandwich generation.” This position has unique challenges—from financial caregiver burnout to career disruptions and competing money priorities.

Your responsibilities might include paying for college tuition, covering parents’ medical expenses, and maintaining your family’s daily needs. These obligations often create not just financial strain but significant emotional stress.

Your responsibilities might include paying for college tuition, covering parents’ medical expenses, and maintaining your family’s daily needs. These obligations often create not just financial strain but significant emotional stress.

Some sandwich generation members may struggle to make ends meet, especially when daily expenses outpace income. Exploring solutions like life insurance, reverse mortgages, or income annuities can help improve cash flow and provide financial relief.

Many sandwich generation members constantly adjust household budgets. The key to surviving this stage is maintaining financial foresight and prioritizing one's own long-term financial health, especially retirement savings, even as one cares for others.

Strong financial partnerships begin with sharing your personal money stories. When you and your partner openly discuss your financial values, you build the trust to weather midlife’s complex challenges.

Try these practical approaches:

Many couples find that monthly “money dates” help them stay aligned on priorities and responsibilities. When financial tensions arise—perhaps over how much to help an adult child or aging parent—having established communication patterns makes finding solutions together much easier.

Financial professionals often recommend these routine conversations as the foundation for successfully managing competing priorities.

Establishing solid legal and financial foundations is the essential first step for couples navigating the complexities of midlife. With so many responsibilities—supporting aging parents, planning for children’s education expenses, and preparing for your retirement years—a comprehensive financial plan is your roadmap to financial success and peace of mind.

Working with a trusted financial advisor can provide clarity as you assess your personal assets, income, and spending habits. Together, you’ll create a plan that addresses every aspect of your finances, from managing credit card debt to optimizing investment management and building retirement accounts that support your long-term goals. Many couples find that this process helps them prioritize what matters most, ensuring that immediate needs and future dreams are accounted for.

It’s also crucial to consider the financial futures of your aging parents. Openly discussing advance care plans and legal documents—such as powers of attorney and healthcare directives—with family members can help avoid confusion and provide support when needed most. While sometimes difficult, these conversations are essential for protecting your parents’ assets and ensuring their wishes are honored.

Don’t overlook the impact of taxes on your financial goals. A knowledgeable advisor can help you explore tax strategies that reduce liabilities and maximize your savings, making your money work harder for you and your family. Reviewing insurance policies is another key step, ensuring that you, your spouse, and your children are protected against unexpected events.

As you lay these foundations, remember the importance of planning for education expenses, saving for retirement, and supporting family members in different ways as life evolves. By discussing and documenting your plans, you’ll be better prepared to handle money challenges and create a secure future for everyone you love.

Taking stock of your financial situation is essential when juggling multiple responsibilities. Review your current assets, debts, income, and cash flow patterns. Consider all aspects of your financial life, including investments, insurance, and estate planning, to ensure a comprehensive understanding of your position. This will give you a clear picture of where you stand today.

Next, identify major upcoming expenses that may impact your finances—college tuition, elder care costs, home repairs, or healthcare needs. Creating a list helps you align these immediate demands with your long-term goals without losing sight of either.

Several tools can simplify this process. Consider using:

These resources help you spot potential issues early and make adjustments before minor concerns become major problems. Keep in mind that certain financial decisions, such as risk tolerance and asset allocation, are subject to individual preferences and circumstances. A mid-year financial planning checklist can provide structure to your review process.

Tax-advantaged 529 plans can be your ally when education expenses loom large, offering growth potential specifically for qualified education costs. Using tax-advantaged accounts to save early for education expenses can make a significant difference in managing future costs. Don’t overlook scholarships and grants—free money that reduces your out-of-pocket burden without affecting your other financial goals.

Finding balance is critical. Set realistic college budget boundaries and avoid tapping retirement accounts whenever possible. Parents can pay for education costs in several ways, such as using savings, taking out loans, or setting up structured payment plans. Remember, you can borrow for college but not for retirement.

Personal loans remain an option for covering educational gaps, but weigh their long-term impact carefully. Consider interest rates and repayment terms alongside federal and institutional aid packages. Many financial advisors recommend exhausting federal student loan options before turning to private financing, as they typically offer more flexible repayment terms and forgiveness possibilities.

Setting clear boundaries around financial support for grown children helps everyone. Instead of open-ended assistance, establish specific guidelines that encourage independence. Some adult children may be unable to cover their own expenses, which can lead parents to provide support. For example, you might help with emergency expenses but not regular bills.

Discuss your contribution limits early when major life events arise—like weddings or first home purchases. This prevents misunderstandings and allows everyone to plan accordingly. Before providing additional support, discussing with your children whether they have saved enough to meet their own financial needs is essential. Consider offering a fixed amount rather than an open checkbook.

To reduce relationship strain when supporting adult children:

Many couples find that putting these agreements in writing helps maintain consistency and prevents emotional decisions that could threaten their financial security.

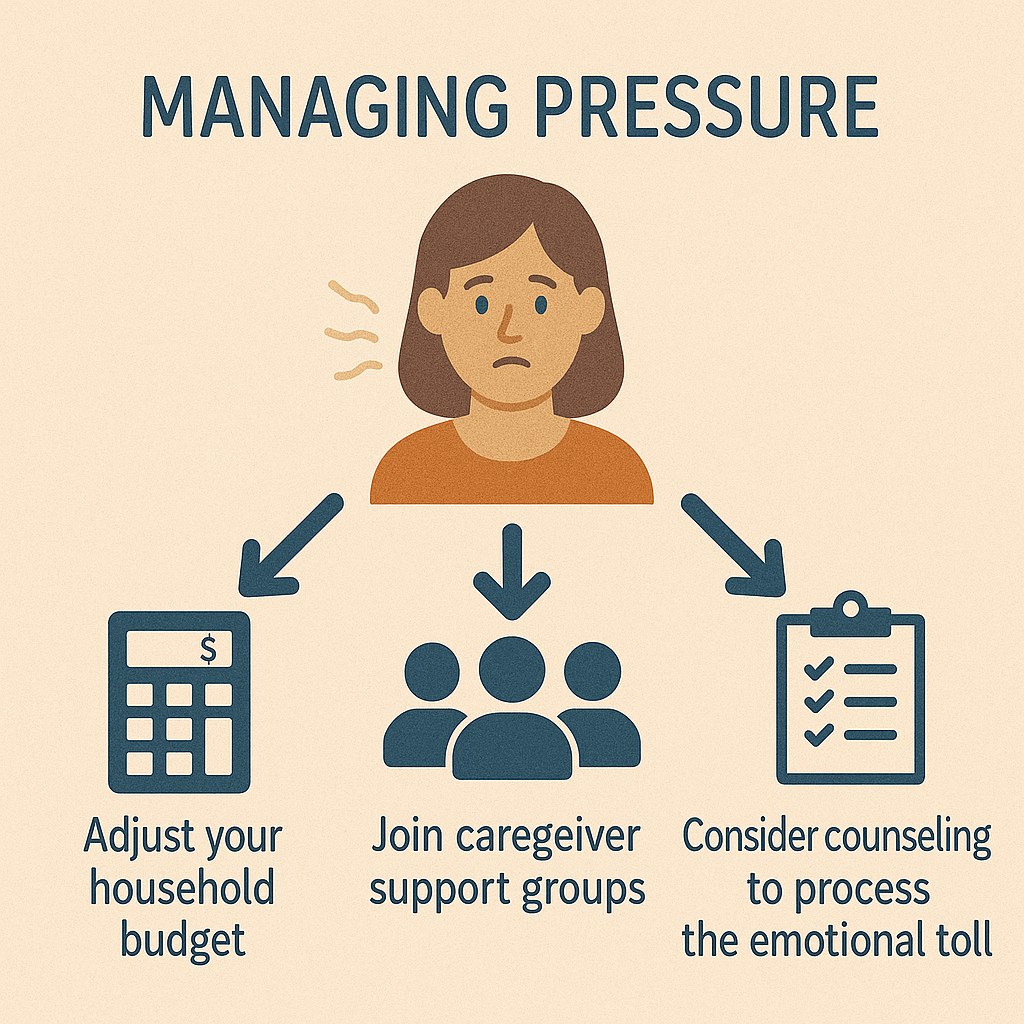

Ongoing financial support for aging parents often includes paying for healthcare, housing, and daily expenses—sometimes at the cost of your own savings or work opportunities. This responsibility can quickly strain your finances and emotional well-being.

Noticing your parents avoiding activities like managing their finances, driving to the bank, or handling daily tasks can signal that they need more support.

Planning ahead for increasing healthcare or long-term care costs is essential. Consider options like long-term care insurance and research available public benefits your parents might qualify for.

To manage this added pressure:

Many sandwich generation members report that creating specific budget categories for parent care helps them track and control these expenses without completely derailing their own financial plans.

While supporting multiple generations, keeping your retirement savings on track is non-negotiable. Many midlife couples make the mistake of pausing retirement contributions when family needs increase, which can severely impact your future security. Proactive planning and consistent saving are essential steps toward a comfortable retirement, even when balancing the financial demands of caring for children and aging parents.

Consider these practical approaches:

Revisiting your retirement goals helps maintain realistic expectations. If caregiving responsibilities have limited your earning potential or increased expenses, you might need to adjust your target retirement age or expected lifestyle.

Don’t underestimate the importance of maintaining a solid emergency fund during this period. Having 3-6 months of expenses readily available prevents dipping into retirement accounts when unexpected costs arise for children or parents.

Finding the right balance between joint and separate finances can strengthen your money management as a couple. Many midlife partners find that combining approaches works best, keeping separate accounts for personal spending while maintaining joint accounts for household expenses.

If you and your partner own a business together, coordinate your business finances with your household money management systems to support your business and personal financial goals.

Consider implementing a ‘separate buckets’ system where you allocate funds to different categories, such as housing, healthcare, and family support. This approach helps track where money goes and creates clarity around shared responsibilities.

Set specific spending thresholds—perhaps $200 or $500—above which you’ll consult each other before making purchases. This will preserve individual autonomy while ensuring big decisions are made together.

Streamline your system with:

This balanced approach helps minimize conflict and ensures both partners maintain financial independence while working as a team.

When juggling multiple financial responsibilities, setting clear priorities becomes essential. Start by working together to rank your goals—building college funds, supporting parents, or securing your retirement. Investing in diversified assets is crucial to reaching your financial goals, as it helps create a well-rounded financial strategy and manage risk.

Create a visual timeline for each goal with specific benchmarks. This helps you track progress and stay motivated when competing demands arise. Many couples find that assigning dollar amounts and deadlines makes abstract goals more concrete. When setting financial priorities, consider investment options that offer a lower rate of taxation, such as long-term capital gains, to enhance tax efficiency and maximize your wealth.

Regular check-ins are vital. Schedule quarterly reviews to assess progress and make adjustments as needed. When unexpected challenges arise—like a parent needing additional care—you’ll have a framework for deciding which goals might need temporary adjustments.

Remember that aligning financial priorities with your shared values strengthens your commitment. When both partners understand why certain goals matter, you’re more likely to weather setbacks together.

Family discussions about money require care and planning. When approaching sensitive topics with adult children or aging parents, start by being transparent about your concerns and possible solutions. Use phrases like “I’m wondering if we could talk about…” rather than making demands. Be mindful of a parent's sense of authority or hierarchy, as acknowledging these feelings can help maintain respect and openness during financial conversations.

Keep these principles in mind:

When discussing inheritance plans or financial support limits, focus on fairness rather than equality. Each family member may need different types of assistance at various times.

Consider bringing in outside help for particularly complex situations—like determining long-term care options or mediating sibling disagreements about parent care. Financial counselors or family mediators provide neutral perspectives to help everyone feel heard while working toward practical solutions.

Finding the right balance between today’s needs and tomorrow’s goals often requires an honest assessment of one's current lifestyle choices. Ask yourself: “Are our spending patterns supporting or hindering our long-term financial health?”

Regular lifestyle reviews help identify areas where small adjustments yield significant long-term benefits. This doesn’t necessarily mean cutting all enjoyment—instead, it’s about making intentional choices that reflect what truly matters to you both. Planning for long-term care can significantly affect the lives of you and your loved ones, ensuring that everyone is better prepared for future healthcare needs.

Try these practical approaches:

Schedule annual “big picture” discussions about how well your lifestyle aligns with your financial goals. These conversations help you stay nimble as circumstances change—whether increasing parent care needs or shifting career opportunities.

Many couples find that revisiting their plans after significant life events prevents small disconnects from becoming major financial problems.

Building common financial ground doesn’t happen automatically—it requires intention and teamwork. A couple's ability to adapt to financial challenges together strengthens their partnership and prepares them for unexpected events. Consider activities that strengthen your connection: attend a financial workshop together, volunteer for causes you both support, or join a financial literacy group. These shared experiences naturally open conversations about what matters most to you both.

When you approach money management as a partnership project rather than a chore, it transforms your relationship. Many couples report working through financial challenges together—especially during the demanding sandwich generation years—deepens their connection.

Successful couples regularly:

Partners who consistently make financial decisions based on shared values typically report greater relationship satisfaction and better resilience when facing midlife’s inevitable challenges.

The journey through midlife’s financial challenges is rarely straightforward, but couples who approach it as true partners often emerge stronger. By establishing clear priorities, maintaining open communication, and making intentional lifestyle choices, you create a foundation that can withstand the competing demands on your resources.

Remember that financial partnership isn’t just about managing money—it’s about aligning your values and building a future that reflects what matters most to both of you. Be sure to keep your financial and legal documents organized and accessible for yourself and your loved ones, as this can help prevent complications in the future. When you navigate these complex waters together, you’re not just protecting your financial health; you’re strengthening the bond that will carry you through the next chapters of life.

Disclaimer: The information provided in this blog post is for educational and informational purposes only and should not be considered as financial, legal, investment, or tax advice. Symple Lending is not responsible for any financial outcomes resulting from following the information or ideas shared in this blog. Every individual's financial situation is unique, and we strongly encourage readers to take their own circumstances into consideration and consult with a qualified financial, legal, tax, and investment advisor before making any financial decisions. Symple Lending does not provide financial, legal, tax, or investment advice.

Did you know that nearly 70% of couples argue about money, regardless of how much they have? These conversations are significant for those over 40,...

Did you know that 47% of adults in their 40s and 50s have a parent age 65 or older and either raise a young child or financially support a grown...

Did you know couples discussing finances at least once a month report significantly higher relationship satisfaction? Yet after 40, these...

What are your long-term financial goals? How important is it that you are financially well-off in life? Are you making the right financial choices...

Did you know that 78% of Americans live paycheck to paycheck, regardless of their income level? Financial wellness isn't just about how much money...

In today's world, where financial burdens have become a common aspect of many people's lives, it's essential to adopt proactive strategies to break...