Emergency Fund vs. Savings Account: Why You Need Both for True Financial Security

Did you know that 56% of Americans couldn't cover an unexpected $1,000 expense from their savings? Many people mistakenly believe one financial...

5 min read

Did you know that 56% of Americans couldn't cover an unexpected $1,000 expense from their savings? Many people mistakenly believe one financial account can serve all their needs, leading to dangerous financial vulnerability.

Understanding the critical difference between emergency funds and savings accounts isn't just financial jargon—it's the foundation of true financial security. When these accounts are properly separated and maintained, you gain both protection against life's unexpected challenges and the freedom to pursue your planned financial goals without compromise.

A savings account is a secure deposit account at a bank or credit union that helps you store money while earning interest. Think of it as a dedicated place for setting aside funds for planned expenses you know are coming.

Most people use savings accounts for specific financial goals like:

What makes savings accounts helpful is their basic features:

Unlike emergency funds, savings accounts are designed for expenses you see coming, not for unexpected expenses.

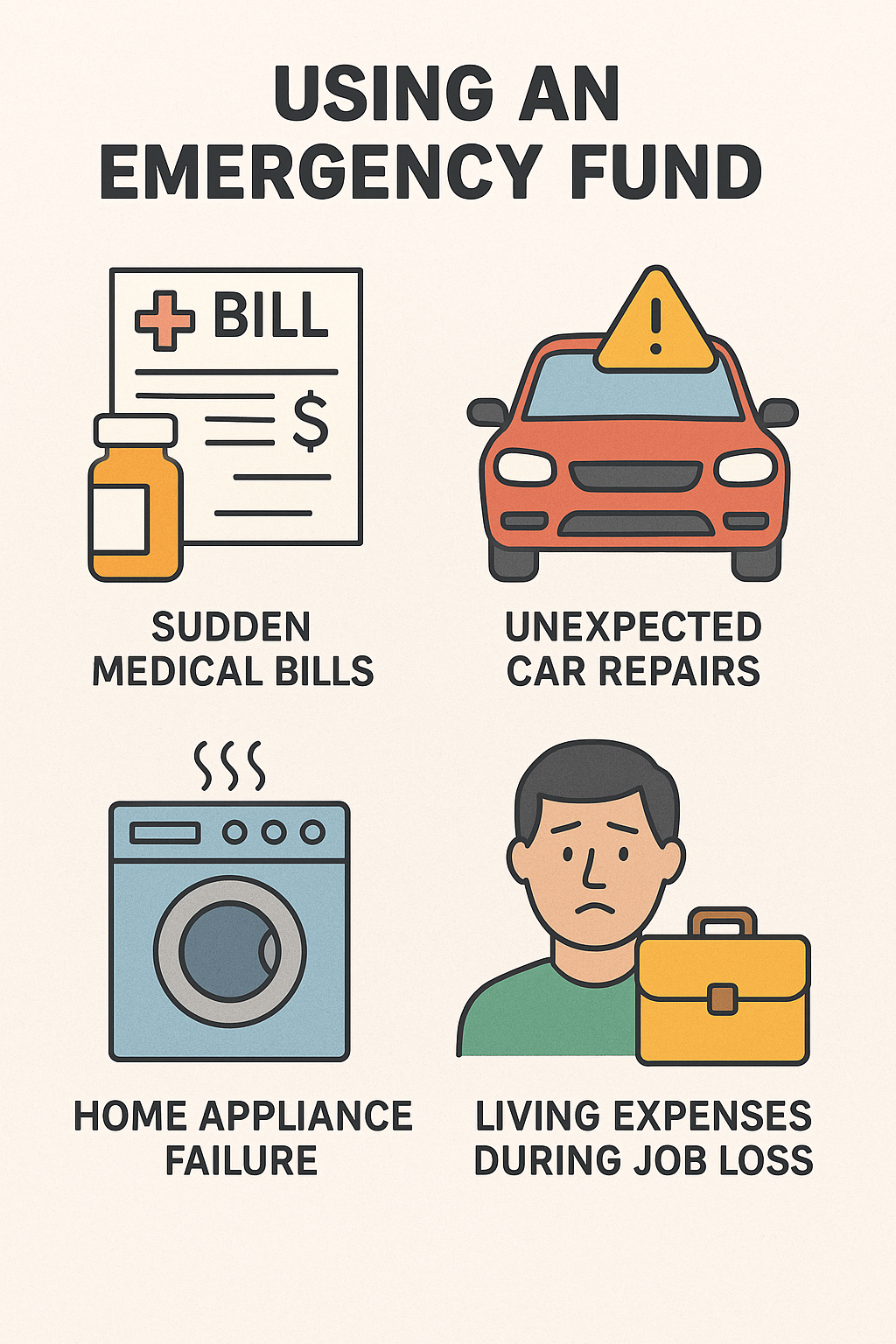

Unlike your savings account, an emergency fund is money set aside specifically for life's unexpected financial surprises. This financial safety net protects you when unplanned expenses arise that you couldn't possibly see coming.

Your emergency savings steps in when you face situations like:

The key difference is in the purpose: emergency funds aren't for planned purchases or known expenses—they're solely for financial curveballs that might otherwise force you into debt.

What makes a proper emergency fund?

While both help secure your financial future, savings accounts and emergency funds serve distinctly different purposes:

When both accounts are properly maintained, you gain both financial security and the ability to pursue your planned financial goals without compromise, therefore protecting your financial well being.

Keeping your savings account and emergency fund separate creates clear financial boundaries that help you stay organized. When each account has a specific purpose, you're less likely to dip into your emergency money for non-emergencies or spend your vacation savings on unexpected car repairs.

This separation also provides genuine peace of mind. Knowing you have money specifically set aside for life's surprises reduces financial stress and anxiety. When you face an unexpected expense, you won't have to worry about derailing your other financial goals.

Maintaining separate accounts improves your budgeting effectiveness, too. It's easier to track your progress toward specific goals and stick to your savings strategy when funds aren't mixed together. This separation helps build financial discipline – you'll think twice before withdrawing money when accounts have clear, distinct purposes.

As one bank customer shared: "Having separate accounts helped me weather a job loss without touching the money I'd saved for my daughter's braces. Both needs were met without compromise."

When it comes to storing your emergency money, not all accounts are created equal. High-yield savings accounts stand out as the ideal choice for emergency funds because they combine immediate access with better interest rates than standard accounts.

The most important feature for your emergency fund account is liquidity – being able to access your money quickly when you need it most. This means:

Security matters too. Look for accounts that are FDIC-insured (or NCUA-insured for credit unions), protecting your money up to $250,000 per depositor. This insurance ensures your emergency safety net remains intact even if the financial institution fails.

Many online banks offer competitive high-yield savings accounts with no minimum balance requirements and easy transfer options to your primary checking account – perfect for when emergency expenses strike.

Most financial experts recommend keeping three to six months' worth of essential living expenses in your emergency fund. This amount typically covers essential expenses such as housing, utilities, food, transportation, and insurance—not discretionary spending like entertainment or dining out.

If saving several months of expenses feels overwhelming, start small. Begin with a modest goal of $500-$1,000 as your initial safety net, then build from there. Remember: having some emergency savings is significantly better than none at all.

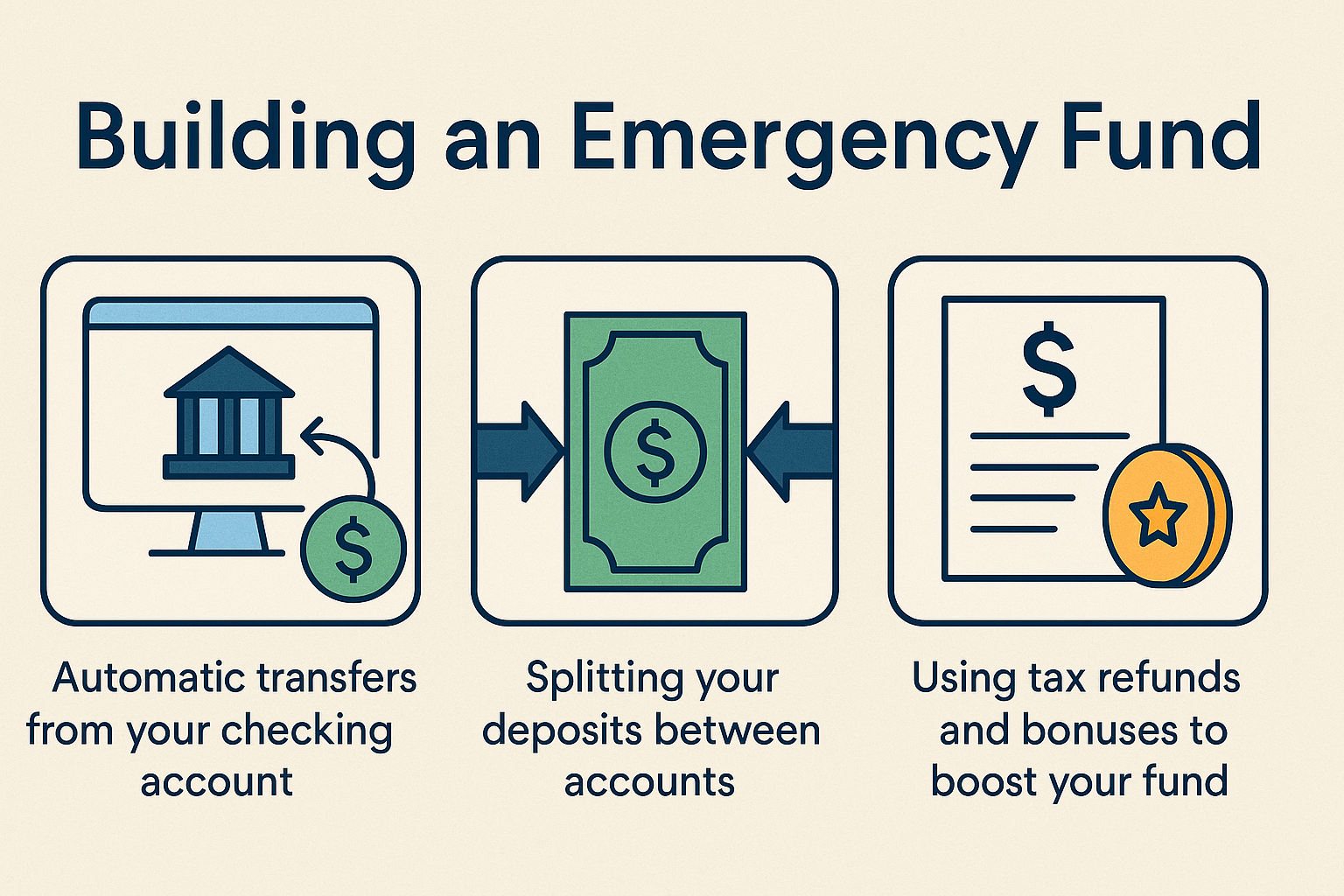

To build your fund consistently:

Review your emergency fund regularly, especially after life changes like having children, buying a home, or switching jobs. Your emergency needs may change as your life circumstances evolve.

Review your emergency fund regularly, especially after life changes like having children, buying a home, or switching jobs. Your emergency needs may change as your life circumstances evolve.

Once fully funded, you can redirect those contributions to other goals while maintaining your safety net.

Let's look at how these accounts work in real-life situations:

Sarah and Michael saved $15,000 in their dedicated savings account over two years for their kitchen renovation. When unexpected financial shocks arose during the project, they had the flexibility to adjust their timeline without stress because this was a planned expense with built-in flexibility.

When Jessica's transmission failed without warning, the $2,800 repair bill could have derailed her finances. Instead, she withdrew the amount from her emergency fund, paid for repairs immediately, and avoided credit card debt. Her vacation savings remained untouched.

Keeping these accounts separate protects you from having to make difficult choices. Without this distinction, you might face situations where:

Now that you understand the importance of opening separate accounts, it's time to put this knowledge into action. Start by taking inventory of your current financial accounts and clearly defining their purposes. Ask yourself: "Does my current setup protect my emergency needs while supporting my planned goals?"

Having specific targets for both accounts sets you up for financial success:

Consider opening dedicated accounts if you haven't already. Many banks offer the ability to create and name multiple savings accounts without additional fees – perfect for keeping your emergency fund distinct from other savings goals.

Make your strategy work through automation:

Remember that financial needs change. Review both accounts quarterly to ensure they still align with your current life situation and adjust contribution amounts as needed.

Financial peace of mind doesn't come from simply having enough money saved—it comes from having the right money in the right places. By maintaining separate accounts for emergencies and planned expenses, you create a financial framework that can withstand both expected costs and unexpected events.

Take action today by evaluating your current setup. Are your emergency and savings funds clearly separated? If not, consider opening dedicated accounts and automating contributions to each. This simple organizational step could make the difference between financial stress and financial confidence no matter what life throws your way.

Disclaimer: The information provided in this blog post is for educational and informational purposes only and should not be considered as financial, legal, investment, or tax advice. Symple Lending is not responsible for any financial outcomes resulting from following the information or ideas shared in this blog. Every individual's financial situation is unique, and we strongly encourage readers to take their own circumstances into consideration and consult with a qualified financial, legal, tax, and investment advisor before making any financial decisions. Symple Lending does not provide financial, legal, tax, or investment advice.

Did you know that 56% of Americans couldn't cover an unexpected $1,000 expense from their savings? Many people mistakenly believe one financial...

Did you know that 78% of Americans live paycheck to paycheck, making them vulnerable when emergencies strike? Living paycheck to paycheck means any...

Did you know that 56% of Americans couldn't cover an unexpected $1,000 expense without going into debt? The journey back to security can feel...

Have you ever wondered if that $1,000 sitting in your savings account is enough to handle life’s curveballs? While financial experts toss around the...

Did you know that 78% of Americans live paycheck to paycheck, making them vulnerable when emergencies strike? Living paycheck to paycheck means any...

Did you know that 56% of Americans couldn't cover an unexpected $1,000 expense without going into debt? The journey back to security can feel...