Breanne Neely

Breanne Neely

Common Reasons to Use a Personal Loan (and When Not To)

Wondering exactly why get a personal loan? Whether you need to fund a major life event or manage a sudden financial hurdle, these financial tools...

Did you know that a personal loan could be your credit score's best friend or worst enemy? It all depends on how you manage it. While many borrowers focus solely on interest rates and monthly payments, the relationship between personal loans and your credit score deserves just as much attention.

When used strategically, personal loans can help diversify your credit mix, lower your credit utilization ratio, and establish a positive payment history. However, missteps like missed payments or taking on too much debt can have the opposite effect, potentially dragging your score down for years to come.

Personal loans are a type of installment loan where you borrow a specific amount of money and pay it back through fixed monthly payments over a set period. Unlike revolving credit (such as credit cards), which allows you to repeatedly borrow up to your limit, personal loans provide a one-time lump sum that you gradually repay.

Many people use personal loans for:

Personal loans come in two main varieties: secured and unsecured. Secured personal loans require collateral—something valuable like a car or savings account that the lender can claim if you don't repay. Unsecured personal loans don't require collateral but typically have stricter approval requirements.

Your credit history plays a big role in determining what terms you'll qualify for. Borrowers with higher credit scores generally receive better interest rates and more favorable loan conditions. Before applying for a personal loan, it's helpful to check your credit report and understand how your current credit score might affect your borrowing options.

Personal loans can actually help your credit score in several meaningful ways when managed responsibly. Here's how:

Improved credit mix: Adding a personal loan introduces an installment loan account to your credit profile. If you previously only had credit cards, this diversity in your credit mix can boost your score since credit scoring models favor having different types of credit.

Improved credit mix: Adding a personal loan introduces an installment loan account to your credit profile. If you previously only had credit cards, this diversity in your credit mix can boost your score since credit scoring models favor having different types of credit.

Stronger payment history: When you make your personal loan payments on time each month, you're building a positive payment history, which is one of the most important aspects of your credit score. Payment history typically accounts for about 35% of your score, making consistent on-time payments a powerful way to strengthen your credit score over time.

Lower credit utilization ratio: If you use a personal loan to eliminate revolving debt (like credit card debt), you could see a significant score increase. This happens because you're reducing your credit card utilization ratio—the percentage of available credit you're using on revolving credit accounts.

Real-world example: Let's say you have $8,000 in credit card debt spread across multiple credit cards with a total limit of $10,000 (80% utilization). By using personal loans for debt consolidation, your utilization drops to 0%, which can quickly raise your credit score, especially if you continue making timely payments on your new loan.

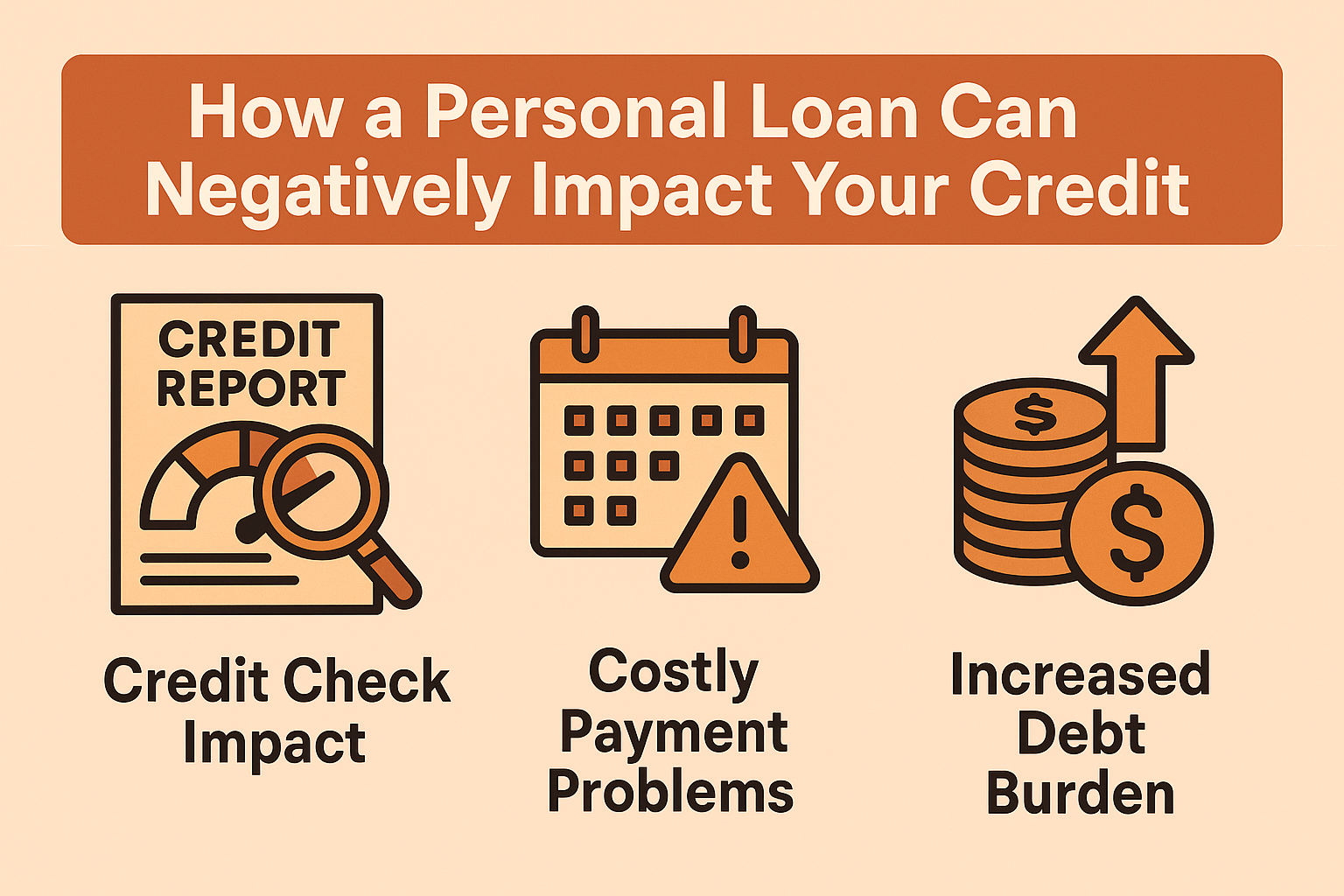

While personal loans can help your credit when managed properly, there are several ways personal loans hurt your credit score, including:

Credit check impact: When you apply for a personal loan, lenders perform a "hard credit inquiry" on your credit report. Each hard inquiry typically lowers your credit score slightly by a few points for a short time. Multiple hard credit inquiries in a brief period can add up, causing a more noticeable drop in your score.

Payment problems can be costly: Missing or making late payments on your personal loan can seriously damage your credit score since payment history weighs so heavily in credit scoring models. Even a single missed payment can remain on your credit report for up to 7 years, affecting future borrowing opportunities.

Increased debt burden: Taking on a new loan increases your overall debt load. If you already have substantial debt, adding more could make you appear financially overextended to lenders, potentially lowering your score.

What happens if you slip up: If you miss several payments or default on your personal loan, your credit score could drop significantly—potentially by 100 points or more for serious delinquencies. This makes getting approved for future credit much harder and more expensive, as lenders will see you as a risky borrower.

When it comes to protecting your credit score, how you handle your personal loan matters just as much as having one. Here are key practices to follow:

Check affordability first: Before signing for a personal loan, make sure the monthly payments fit comfortably within your budget. Calculate how the new payment will affect your financial situation alongside existing bills. If a payment would stretch you too thin, it might be better to look for a smaller loan or wait until your finances improve.

Set up automatic payments: One of the simplest ways to protect your credit score is by never missing a loan payment. Setting up autopay through your bank or lender ensures you are making timely payments, even when life gets busy. If autopay isn't an option, calendar reminders can help you avoid late payments and stay on track to repay your personal loan.

Borrow only what you need: Taking personal loans just because you qualify can lead to unnecessary debt. Only borrow for specific financial goals where the benefits outweigh the cost. This protects both your credit score and your overall financial health.

Understand reporting practices: Not all lenders report to all three major credit bureaus. Before choosing a lender, confirm they report to at least the major bureaus so your on-time payments will help build your credit history across all platforms.

Personal loans can be powerful tools for reaching your financial objectives when used thoughtfully. Many borrowers use these personal loans to pay off high-interest debt, handle unexpected expenses, or build their credit profiles by adding account diversity to their credit mix and establishing consistent payment patterns.

When considering a personal loan, always connect it to a specific financial goal. Ask yourself: "Will this loan help me save money in the long run?" For example, consolidating credit card debt at 18% interest into a personal loan at 10% creates clear savings, a lower monthly payment, and a defined payoff date.

Compare options carefully: Look beyond the advertised interest rate. Factor in other loan terms, including:

The right personal loan should match your financial situation. Some lenders offer specialized options based on your credit profile and goals. For instance, if you're primarily focused on improving your credit score, look for lenders who report to all three major credit bureaus and offer terms that fit your budget.

If you're considering using loans for specific financial goals or to improve your credit standing, comparing offerings from different providers can help you find the solution that best supports both your immediate needs and long-term credit health.

Remember that personal loans are financial tools—they're neither inherently good nor bad for your credit score. The impact ultimately depends on your borrowing habits and repayment discipline. Before taking out a new personal loan, carefully assess your financial situation, have a clear purpose for the funds, and create a solid repayment plan.

With responsible financial planning, most personal loans can be a stepping stone toward better credit and financial health. By understanding both the potential benefits and risks to your credit score, you can make informed decisions that align with your long-term financial goals, rather than just addressing immediate needs.

Disclaimer: The information provided in this blog post is for educational and informational purposes only and should not be considered as financial, legal, investment, or tax advice. Symple Lending is not responsible for any financial outcomes resulting from following the information or ideas shared in this blog. Every individual's financial situation is unique, and we strongly encourage readers to take their own circumstances into consideration and consult with a qualified financial, legal, tax, and investment advisor before making any financial decisions. Symple Lending does not provide financial, legal, tax, or investment advice.

Life doesn’t always follow a straight path—but with the right support, every turn gets easier. From surprise expenses to big plans, we’re here with fast, flexible funding to keep you moving.

.jpeg)

Wondering exactly why get a personal loan? Whether you need to fund a major life event or manage a sudden financial hurdle, these financial tools...

Have you ever wondered exactly what is a personal loan? Whether you need to cover unexpected expenses or finance a major life event, grasping...

Managing multiple credit card payments involves more than keeping track of due dates. The hidden costs — financial, organizational, and emotional —...

1 min read

Your transmission just died, bringing a sudden $3,200 repair bill. Swiping plastic might seem like the best option for emergency expenses, but that...

1 min read

Facing a $3,000 transmission repair? During a get money fast emergency, credit cards provide instant available credit. Conversely, comparing personal...

1 min read

Applying for funding shouldn't feel like a guessing game. According to industry data on critical loan approval factors, most rejections are...