Breanne Neely

Breanne Neely

Build an Emergency Fund Without Derailing Your Life

Life rarely goes exactly to plan. From sudden home repairs to urgent healthcare needs, staying prepared is essential. Unfortunately, the average US...

Life doesn’t always follow a straight path—but with the right support, every turn gets easier. From surprise expenses to big plans, we’re here with fast, flexible funding to keep you moving.

Life rarely goes exactly to plan. From sudden home repairs to urgent healthcare needs, staying prepared is essential. Unfortunately, the average US...

The second half of the year is a practical window to review your financial progress, reset your goals, and build habits that can create real results...

Managing money doesn't have to be a stressful daily chore. If you want to achieve your financial goals faster, understanding how automating bills,...

.png)

1 min read

When figuring out how to shop for a loan, financial jargon can quickly become overwhelming. Fortunately, understanding the total cost of borrowing...

1 min read

If a friend asked to borrow $1,000, you wouldn't just check their wallet. You’d verify they could repay tomorrow. In practice, this mirrors...

1 min read

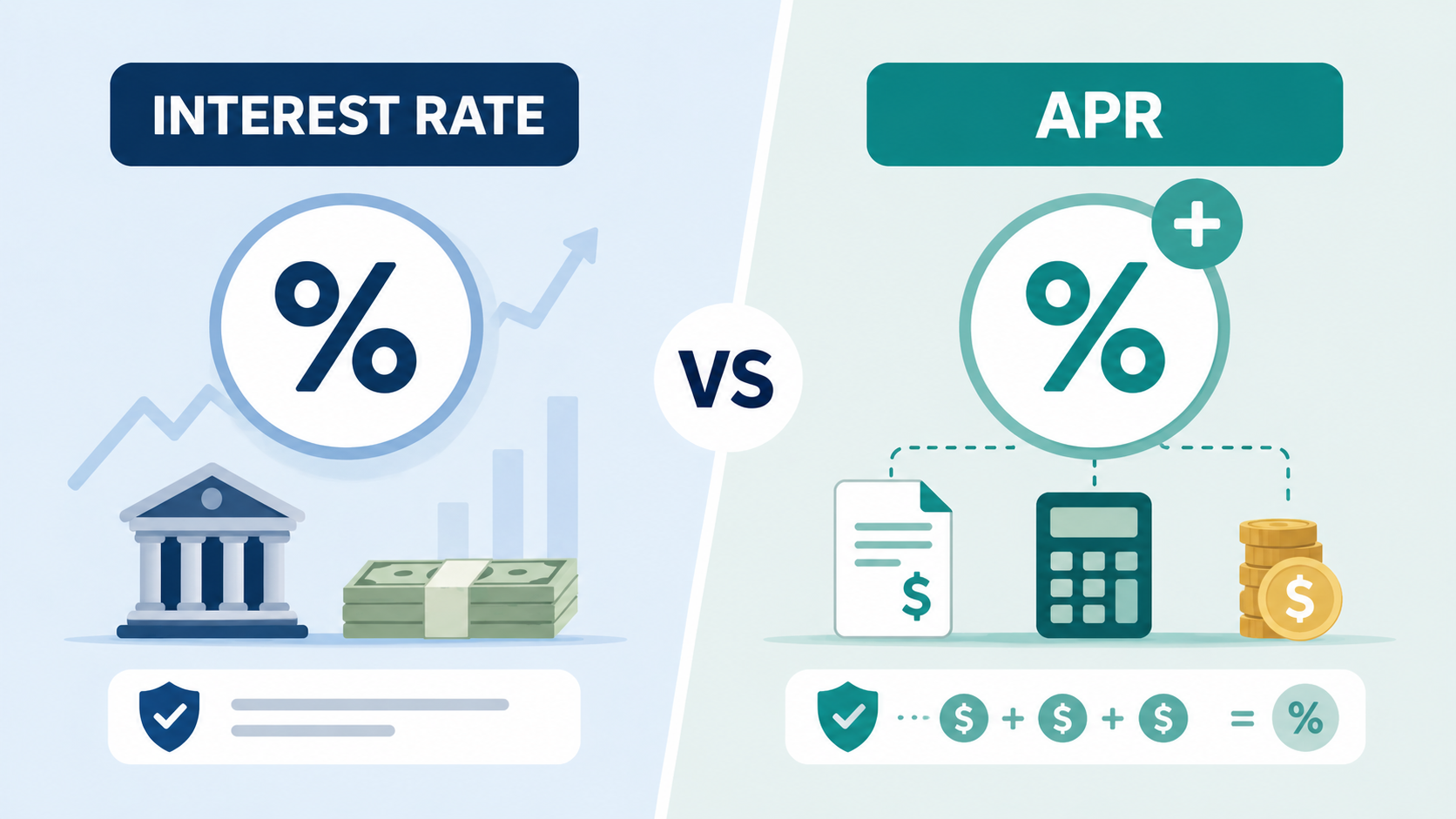

When shopping for a mortgage, auto loan, or credit card, you will inevitably encounter two crucial numbers. Understanding APR vs. Interest Rate:...